All Exams >

Commerce >

Economics Class 11 >

All Questions

All questions of The Theory of the Firm under Perfect Competition for Commerce Exam

A firm can sell as much as it wants at the market price. The situation is related to?- a)Monopoly

- b)Monopolistic competition

- c)Perfect competition

- d)Oligopoly

Correct answer is option 'C'. Can you explain this answer?

A firm can sell as much as it wants at the market price. The situation is related to?

a)

Monopoly

b)

Monopolistic competition

c)

Perfect competition

d)

Oligopoly

|

Sushil Kumar answered |

Pure or perfect competition is a theoretical market structure in which the following criteria are met:

- All firms sell an identical product (the product is a "commodity" or "homogeneous").

- All firms are price takers (they cannot influence the market price of their product). Market share has no influence on prices.

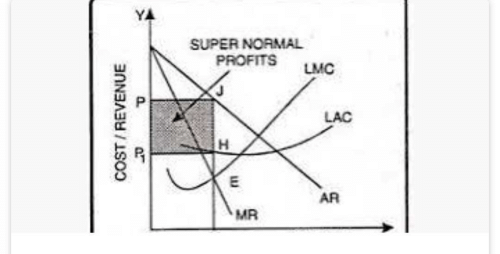

When AR=Rs. 10 and AC=Rs. 8, the firm makes?- a)Gross profit

- b)Supernormal profit

- c)Normal profit

- d)Net profit

Correct answer is option 'B'. Can you explain this answer?

When AR=Rs. 10 and AC=Rs. 8, the firm makes?

a)

Gross profit

b)

Supernormal profit

c)

Normal profit

d)

Net profit

|

|

Ishan Choudhury answered |

Supernormal profit is defined as extra profit above that level of normal profit.

Here the firm earns profit of Rs. 2 over the cost occurred.

Here the firm earns profit of Rs. 2 over the cost occurred.

____________ is an ideal market?- a)Monopolistic competition

- b)Oligopoly

- c)Perfect competition

- d)Monopoly

Correct answer is option 'C'. Can you explain this answer?

____________ is an ideal market?

a)

Monopolistic competition

b)

Oligopoly

c)

Perfect competition

d)

Monopoly

|

|

Vikas Kapoor answered |

Pure or perfect competition is a theoretical market structure in which the following criteria are met: All firms sell an identical product (the product is a "commodity" or "homogeneous"). All firms are price takers (they cannot influence the market price of their product). Market share has no influence on prices.

This a MCQ (Multiple Choice Question) based practice test of Chapter 4 - Theory of Firm Under Perfect Competition of Economics of Class XII (12) for the quick revision/preparation of School Board examinationsQ Condition for producer equilibrium is:- a)TC=TSC

- b)MC=MR

- c)TR=TVC

- d)None of above

Correct answer is 'B'. Can you explain this answer?

This a MCQ (Multiple Choice Question) based practice test of Chapter 4 - Theory of Firm Under Perfect Competition of Economics of Class XII (12) for the quick revision/preparation of School Board examinations

Q Condition for producer equilibrium is:

a)

TC=TSC

b)

MC=MR

c)

TR=TVC

d)

None of above

|

Puja Nambiar answered |

Condition for Producer Equilibrium

The producer equilibrium is a situation where a firm is maximizing its profits by producing a level of output where marginal cost (MC) is equal to marginal revenue (MR). In other words, the producer equilibrium is reached when a firm is producing at the point where it is making the highest possible economic profit.

The condition for producer equilibrium is as follows:

MC = MR

Explanation

Marginal cost (MC) is the additional cost of producing one more unit of output. Marginal revenue (MR) is the additional revenue earned by selling one more unit of output. In perfect competition, a firm is a price taker, meaning it cannot influence the market price of the product it sells. Therefore, the price of the product remains constant for the firm.

In perfect competition, the firm's marginal revenue (MR) is equal to the price of the product. Therefore, the condition for producer equilibrium can be rephrased as:

MC = P

where P is the price of the product.

If a firm produces at a level where MC is less than MR, it means that the firm can increase its profits by producing more units of output. Similarly, if a firm produces at a level where MC is greater than MR, it means that the firm can increase its profits by producing fewer units of output. So, the producer equilibrium is reached only when MC is equal to MR, where the firm is producing the level of output that maximizes its profits.

Conclusion

The condition for producer equilibrium is MC = MR, where a firm is producing the level of output that maximizes its profits. In perfect competition, where a firm is a price taker, the condition can be rephrased as MC = P.

The producer equilibrium is a situation where a firm is maximizing its profits by producing a level of output where marginal cost (MC) is equal to marginal revenue (MR). In other words, the producer equilibrium is reached when a firm is producing at the point where it is making the highest possible economic profit.

The condition for producer equilibrium is as follows:

MC = MR

Explanation

Marginal cost (MC) is the additional cost of producing one more unit of output. Marginal revenue (MR) is the additional revenue earned by selling one more unit of output. In perfect competition, a firm is a price taker, meaning it cannot influence the market price of the product it sells. Therefore, the price of the product remains constant for the firm.

In perfect competition, the firm's marginal revenue (MR) is equal to the price of the product. Therefore, the condition for producer equilibrium can be rephrased as:

MC = P

where P is the price of the product.

If a firm produces at a level where MC is less than MR, it means that the firm can increase its profits by producing more units of output. Similarly, if a firm produces at a level where MC is greater than MR, it means that the firm can increase its profits by producing fewer units of output. So, the producer equilibrium is reached only when MC is equal to MR, where the firm is producing the level of output that maximizes its profits.

Conclusion

The condition for producer equilibrium is MC = MR, where a firm is producing the level of output that maximizes its profits. In perfect competition, where a firm is a price taker, the condition can be rephrased as MC = P.

Under which market condition firms make only Normal Profit in the long run?- a)Oligopoly

- b)Monopoly

- c)Monopolistic competition

- d)Duopoly

Correct answer is option 'C'. Can you explain this answer?

Under which market condition firms make only Normal Profit in the long run?

a)

Oligopoly

b)

Monopoly

c)

Monopolistic competition

d)

Duopoly

|

|

Nandini Iyer answered |

In the long-run, the demand curve of a firm in a monopolistic competitive

Other name by which average revenue curve known:- a)Indifference curve

- b)Profit curve

- c)Average cost curve

- d)Demand curve

Correct answer is option 'D'. Can you explain this answer?

Other name by which average revenue curve known:

a)

Indifference curve

b)

Profit curve

c)

Average cost curve

d)

Demand curve

|

|

Aryan Khanna answered |

Average revenue curve is often called the demand curve due to its representation of the product's demand in the market. Each point on the curve represents the price of the product in the market. Price determines the demand for a product, hence Average revenue curve is also demand curve.

Assuming it is a perfect competitive market.

Assuming it is a perfect competitive market.

In perfect competition, since the firm is a price taker, the ________ curve is straight line- a)Total cost

- b)Marginal cost

- c)Total revenue

- d)Marginal revenue

Correct answer is option 'D'. Can you explain this answer?

In perfect competition, since the firm is a price taker, the ________ curve is straight line

a)

Total cost

b)

Marginal cost

c)

Total revenue

d)

Marginal revenue

|

|

Aryan Khanna answered |

Marginal revenue is the extra revenue generated when a perfectly competitive firm sells one more unit of output. The marginal revenue received by a firm is the change in total revenue divided by the change in quantity.

Perfect competition is a market structure with a large number of small firms, each selling identical goods. Perfectly competitive firms have perfect knowledge and perfect mobility into and out of the market. These conditions mean perfectly competitive firms are price takers, they have no market control and receive the going market price for all output sold.

Since they are the price takers and have no control over price but just the production, so even if they increase their quantity of production, still the price will remain constant and so does the marginal revenue.

In the long run the market price of a commodity is equal to its minimum average cost of production under the___________?- a)Monopolist competition

- b)Perfect competition

- c)Oligopoly

- d)Monopoly

Correct answer is option 'B'. Can you explain this answer?

In the long run the market price of a commodity is equal to its minimum average cost of production under the___________?

a)

Monopolist competition

b)

Perfect competition

c)

Oligopoly

d)

Monopoly

|

|

Kiran Mehta answered |

Perfect competition is an industry structure in which there are many firms producing homogeneous products.

None of the firms are large enough to influence the industry. In the long-run, companies that are engaged in a perfectly competitive market earn zero economic profits.

The long-run equilibrium point for a perfectly competitive market occurs where the demand curve (price) intersects the marginal cost (MC) curve and the minimum point of the average cost (AC) curve.

Since they are the price takers and the price remains constant so does the AC of production.

When ___________, the firms are earning just normal profit:- a)AC=AR

- b)MC=AC

- c)AR=MR

- d)MC=MR

Correct answer is option 'A'. Can you explain this answer?

When ___________, the firms are earning just normal profit:

a)

AC=AR

b)

MC=AC

c)

AR=MR

d)

MC=MR

|

|

Vikas Kapoor answered |

AC = AR means the firm’s cost and revenue are equal which means the firm does not earn any profit or no loss, which means the firm is earning normal profit.

Which of the following is the condition for equilibrium of a firm?- a)MC curve must cut MR curve from above

- b)MR = MC

- c)None of above

- d)Both of these

Correct answer is option 'B'. Can you explain this answer?

Which of the following is the condition for equilibrium of a firm?

a)

MC curve must cut MR curve from above

b)

MR = MC

c)

None of above

d)

Both of these

|

Rahul Chaudhary answered |

Equilibrium of a Firm:

Equilibrium of a firm refers to a situation where the firm is earning maximum profits or where there is no incentive to change the level of output. In other words, the firm is producing the level of output where its marginal cost equals its marginal revenue.

Condition for Equilibrium:

The condition for equilibrium of a firm is that its marginal revenue (MR) should be equal to its marginal cost (MC). This condition can be explained as follows:

- Marginal Revenue (MR): Marginal revenue is the additional revenue earned by the firm by selling one additional unit of output. It is also the slope of the total revenue curve.

- Marginal Cost (MC): Marginal cost is the additional cost incurred by the firm by producing one additional unit of output. It is also the slope of the total cost curve.

When the firm produces one additional unit of output, it incurs an additional cost (MC) and earns an additional revenue (MR). If MR is greater than MC, the firm should produce more output as it will earn more revenue than the cost incurred. On the other hand, if MC is greater than MR, the firm should produce less output as it will incur more cost than the revenue earned. Therefore, the firm should produce the level of output where MR equals MC, as at this level of output, the firm is earning maximum profits.

Conclusion:

Hence, the condition for equilibrium of a firm is that MR should be equal to MC. If the firm produces any other level of output, it will not be in equilibrium, as it will either earn less profit or incur losses.

Equilibrium of a firm refers to a situation where the firm is earning maximum profits or where there is no incentive to change the level of output. In other words, the firm is producing the level of output where its marginal cost equals its marginal revenue.

Condition for Equilibrium:

The condition for equilibrium of a firm is that its marginal revenue (MR) should be equal to its marginal cost (MC). This condition can be explained as follows:

- Marginal Revenue (MR): Marginal revenue is the additional revenue earned by the firm by selling one additional unit of output. It is also the slope of the total revenue curve.

- Marginal Cost (MC): Marginal cost is the additional cost incurred by the firm by producing one additional unit of output. It is also the slope of the total cost curve.

When the firm produces one additional unit of output, it incurs an additional cost (MC) and earns an additional revenue (MR). If MR is greater than MC, the firm should produce more output as it will earn more revenue than the cost incurred. On the other hand, if MC is greater than MR, the firm should produce less output as it will incur more cost than the revenue earned. Therefore, the firm should produce the level of output where MR equals MC, as at this level of output, the firm is earning maximum profits.

Conclusion:

Hence, the condition for equilibrium of a firm is that MR should be equal to MC. If the firm produces any other level of output, it will not be in equilibrium, as it will either earn less profit or incur losses.

What are the conditions for the long run equilibrium of the competitive firm?- a)SMC=SAC=LMC

- b)P=MR

- c)LMC=LAC=P

- d)All of the above

Correct answer is option 'C'. Can you explain this answer?

What are the conditions for the long run equilibrium of the competitive firm?

a)

SMC=SAC=LMC

b)

P=MR

c)

LMC=LAC=P

d)

All of the above

|

Anjana Desai answered |

Conditions for Long Run Equilibrium of Competitive Firm

In a perfectly competitive market, there are certain conditions that must be met for a firm to achieve long-run equilibrium. These conditions are as follows:

LMC = LAC = P

In the long run, a firm in a perfectly competitive market will produce at the point where its long-run marginal cost (LMC) is equal to its long-run average cost (LAC). At this point, the firm is producing at the minimum efficient scale, which means that it is producing at the lowest possible cost.

At the same time, the price of the good or service that the firm is selling (P) must be equal to its long-run marginal cost (LMC) and its long-run average cost (LAC). This condition ensures that the firm is earning zero economic profit in the long run.

Implications of these Conditions

When a firm is in long-run equilibrium, it is operating at maximum efficiency. It is producing at the lowest possible cost and selling its output at a price that is just enough to cover its costs. As a result, there is no incentive for new firms to enter the market, and existing firms have no reason to leave.

In this state of equilibrium, the market is perfectly competitive, with many firms producing the same good or service. Consumers benefit from the low prices that result from the firms' efficient production, and the firms themselves are able to earn a reasonable rate of return on their investments.

Conclusion

In conclusion, the conditions for long-run equilibrium of a competitive firm are that its long-run marginal cost (LMC) must be equal to its long-run average cost (LAC), and both these costs must be equal to the price (P) of the good or service. When these conditions are met, the firm is operating at maximum efficiency and the market is perfectly competitive.

In a perfectly competitive market, there are certain conditions that must be met for a firm to achieve long-run equilibrium. These conditions are as follows:

LMC = LAC = P

In the long run, a firm in a perfectly competitive market will produce at the point where its long-run marginal cost (LMC) is equal to its long-run average cost (LAC). At this point, the firm is producing at the minimum efficient scale, which means that it is producing at the lowest possible cost.

At the same time, the price of the good or service that the firm is selling (P) must be equal to its long-run marginal cost (LMC) and its long-run average cost (LAC). This condition ensures that the firm is earning zero economic profit in the long run.

Implications of these Conditions

When a firm is in long-run equilibrium, it is operating at maximum efficiency. It is producing at the lowest possible cost and selling its output at a price that is just enough to cover its costs. As a result, there is no incentive for new firms to enter the market, and existing firms have no reason to leave.

In this state of equilibrium, the market is perfectly competitive, with many firms producing the same good or service. Consumers benefit from the low prices that result from the firms' efficient production, and the firms themselves are able to earn a reasonable rate of return on their investments.

Conclusion

In conclusion, the conditions for long-run equilibrium of a competitive firm are that its long-run marginal cost (LMC) must be equal to its long-run average cost (LAC), and both these costs must be equal to the price (P) of the good or service. When these conditions are met, the firm is operating at maximum efficiency and the market is perfectly competitive.

Before producer’s equilibrium when MR>MC, the firm earns only- a)Normal Profit

- b)Normal loss

- c)Abnormal loss

- d)Abnormal profit

Correct answer is option 'D'. Can you explain this answer?

Before producer’s equilibrium when MR>MC, the firm earns only

a)

Normal Profit

b)

Normal loss

c)

Abnormal loss

d)

Abnormal profit

|

|

Vikas Kapoor answered |

If a firm makes more than normal profit it is called super-normal profit. Supernormal profit is also called economic profit, and abnormal profit, and is earned when total revenue is greater than the total costs.

Total profits = total revenue (TR) – total costs (TC)

Abnormal Profit = MR > MC

Total profits = total revenue (TR) – total costs (TC)

Abnormal Profit = MR > MC

For maximum profit, the condition is:- a)MC=AC

- b)MR=MC

- c)AR=AC

- d)MR=AR

Correct answer is option 'B'. Can you explain this answer?

For maximum profit, the condition is:

a)

MC=AC

b)

MR=MC

c)

AR=AC

d)

MR=AR

|

|

Rajat Patel answered |

This strategy is based on the fact that the total profit reaches its maximum point where marginal revenue equals marginal profit. This is the case because the firm will continue to produce until marginal profit is equal to zero, and marginal profit equals the marginal revenue (MR) minus the marginal cost (MC).

Supernormal profit occur, when?- a)Total revenue is equal to variable cost

- b)Average revenue is more than average cost

- c)Average revenue is equal to average cost

- d)Total revenue is equal to total cost

Correct answer is option 'B'. Can you explain this answer?

Supernormal profit occur, when?

a)

Total revenue is equal to variable cost

b)

Average revenue is more than average cost

c)

Average revenue is equal to average cost

d)

Total revenue is equal to total cost

|

|

Poonam Reddy answered |

Supernormal profit is defined as extra profit above that level of normal profit. Supernormal profit is also known as abnormal profit. Abnormal profit means there is an incentive for other firms to enter the industry.

The elasticity at a point on a straight line supply curve passing through the origin making an angle of 45°will be- a)4

- b)2

- c)3

- d)1.0

Correct answer is option 'D'. Can you explain this answer?

The elasticity at a point on a straight line supply curve passing through the origin making an angle of 45°will be

a)

4

b)

2

c)

3

d)

1.0

|

|

Sahil Khanna answered |

Degrees with the horizontal axis is equal to 1.

Explanation:

The elasticity of supply is defined as the percentage change in quantity supplied divided by the percentage change in price. Mathematically, it can be represented as:

Elasticity of Supply = (% Change in Quantity Supplied) / (% Change in Price)

For a linear supply curve passing through the origin, the slope of the curve represents the change in quantity supplied for a given change in price. This slope is constant along the curve, and equals the tangent of the angle made by the curve with the horizontal axis.

In this case, the angle is 45 degrees, which means the slope is 1. Therefore, for a given change in price, the quantity supplied changes by the same percentage. This implies that the elasticity of supply is 1, which means that supply is unit elastic at every point along the curve.

Explanation:

The elasticity of supply is defined as the percentage change in quantity supplied divided by the percentage change in price. Mathematically, it can be represented as:

Elasticity of Supply = (% Change in Quantity Supplied) / (% Change in Price)

For a linear supply curve passing through the origin, the slope of the curve represents the change in quantity supplied for a given change in price. This slope is constant along the curve, and equals the tangent of the angle made by the curve with the horizontal axis.

In this case, the angle is 45 degrees, which means the slope is 1. Therefore, for a given change in price, the quantity supplied changes by the same percentage. This implies that the elasticity of supply is 1, which means that supply is unit elastic at every point along the curve.

In which of the following types of market structures, are resources, assumed to be mobile?- a)Oligopoly

- b)Perfect competition

- c)Monopolistic competition

- d)Monopoly

Correct answer is option 'B'. Can you explain this answer?

In which of the following types of market structures, are resources, assumed to be mobile?

a)

Oligopoly

b)

Perfect competition

c)

Monopolistic competition

d)

Monopoly

|

|

Ishan Choudhury answered |

Pure or perfect competition is a theoretical market structure in which the following criteria are met:

1. All firms sell an identical product (the product is a "commodity" or "homogeneous").

2. All firms are price takers (they cannot influence the market price of their product).

3. Market share has no influence on prices.

4. Buyers have complete or "perfect" information—in the past, present and future—about the product being sold and the prices charged by each firm.

5. Resources for such a labor are perfectly mobile.

6. Firms can enter or exit the market without cost.

1. All firms sell an identical product (the product is a "commodity" or "homogeneous").

2. All firms are price takers (they cannot influence the market price of their product).

3. Market share has no influence on prices.

4. Buyers have complete or "perfect" information—in the past, present and future—about the product being sold and the prices charged by each firm.

5. Resources for such a labor are perfectly mobile.

6. Firms can enter or exit the market without cost.

A rational consumer is a person who?- a)Has perfect knowledge of the market

- b)Is not influenced by persuasive advertising

- c)Behaves at all times, other things being equal, in a judicious manner

- d)Knows the prices of goods in different market and buys the cheapest

Correct answer is option 'A'. Can you explain this answer?

A rational consumer is a person who?

a)

Has perfect knowledge of the market

b)

Is not influenced by persuasive advertising

c)

Behaves at all times, other things being equal, in a judicious manner

d)

Knows the prices of goods in different market and buys the cheapest

|

|

Alok Verma answered |

A rational consumer is considered to be that person who makes rational consumption decisions.

In other words, the consumer who makes his choices after considering all the other alternative goods (and services) available in the market is called a rational consumer.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): Oil Producing Companies have an oligopoly market.Reason (R): There are only few countries that produce and export crude oil in the whole world.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'A'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): Oil Producing Companies have an oligopoly market.

Reason (R): There are only few countries that produce and export crude oil in the whole world.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Priyanka Khatri answered |

Throughout history, there have been oligopolies in many different industries, including steel manufacturing, oil, railroads, tire manufacturing, grocery store chains, and wireless carriers. Other industries with an oligopoly structure are airlines and pharmaceuticals.

Beyond producer’s equilibrium when MR<MC, the firm earns only- a)Abnormal profit

- b)Normal loss

- c)Abnormal loss

- d)Normal Profit

Correct answer is option 'C'. Can you explain this answer?

Beyond producer’s equilibrium when MR<MC, the firm earns only

a)

Abnormal profit

b)

Normal loss

c)

Abnormal loss

d)

Normal Profit

|

Aravind Saha answered |

Marginal Cost < Marginal Revenue means abnormal loss situation, where the total revenue of a business does not cover total cost incurred for the business, due to which the profits of the business are below normal limits.

While a seller under perfect competition equates price and MC to maximize profits a monopolist should equate?- a)MR and MC

- b)AR and MR

- c)AR and MC

- d)TC and TR

Correct answer is option 'A'. Can you explain this answer?

While a seller under perfect competition equates price and MC to maximize profits a monopolist should equate?

a)

MR and MC

b)

AR and MR

c)

AR and MC

d)

TC and TR

|

|

Vikas Kapoor answered |

In a monopolistic market, there is only one firm that produces a product. There is absolute product differentiation because there is no substitute.

The marginal cost of production is the change in the total cost that arises when there is a change in the quantity produced.

The marginal revenue is the change in the total revenue that arises when there is a change in the quantity produced a firm maximizes its total profit by equating marginal cost to marginal revenue and solving for the price of one product and the quantity it must produce.

The elasticity at a point on a straight line supply curve passing through the origin will be- a)3

- b)1.0

- c)4

- d)2

Correct answer is option 'B'. Can you explain this answer?

The elasticity at a point on a straight line supply curve passing through the origin will be

a)

3

b)

1.0

c)

4

d)

2

|

|

Arun Yadav answered |

Regardless of the gradient of the linear supply curve or its position on the supply curve, the PES of a linear supply curve that passes through the origin is always equal to 1. Therefore, if the supply curve originates with P=0 and Q=0, the elasticity will always be 1.

Formula-

%Change in quantity

%change in price.

Formula-

%Change in quantity

%change in price.

A competitive firm in the short run incurs losses. The firm continues production, if?- a)P=AVC

- b)P>AVC

- c)P<AVC

- d)P>=AVC

Correct answer is option 'D'. Can you explain this answer?

A competitive firm in the short run incurs losses. The firm continues production, if?

a)

P=AVC

b)

P>AVC

c)

P<AVC

d)

P>=AVC

|

|

Om Desai answered |

With loss minimization, price exceeds average variable cost but is less than average total cost at the quantity that equates marginal revenue and marginal cost. In this case, the firm incurs a smaller loss by producing some output than by not producing any output.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): The vegetable market is a perfect example of perfect competition market.Reason (R): The marketers have no control over the prices of the product.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'A'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): The vegetable market is a perfect example of perfect competition market.

Reason (R): The marketers have no control over the prices of the product.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Naina Sharma answered |

Perfect competition occurs when all companies sell identical products, market share does not influence price, companies are able to enter or exit without barrier, buyers have “perfect” or full information, and companies cannot determine prices. For example consider a farmers market where each vendor sells the same type of jam. There is little differentiation between each of their products, as they use the same recipe, and they each sell them at an equal price. At the same time, sellers are few and free to participate in the market without any barrier. Buyers, in this case, would be fully knowledgeable of the product's recipe, and any other information relevant to the good.

Globalization has made Indian Market as?- a)Seller market

- b)Buyer market

- c)Monopsony market

- d)Monopoly market

Correct answer is option 'B'. Can you explain this answer?

Globalization has made Indian Market as?

a)

Seller market

b)

Buyer market

c)

Monopsony market

d)

Monopoly market

|

|

Nandini Iyer answered |

Globalisation is the rapid integration or interconnection between countries mostly on the economic plane. In other words Globalisation means integrating our economy with the world economy.Movement of people between countries increases due to globalisation. CORRECT OPTION IS (B).

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): In monopolistic competition, there is a fierce competition between the firms in the market.Reason (R): In monopolistic competition, there are a large number of sellers and buyers in the market.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'B'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): In monopolistic competition, there is a fierce competition between the firms in the market.

Reason (R): In monopolistic competition, there are a large number of sellers and buyers in the market.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

Mansi Mukherjee answered |

Explanation:

Assertion (A): In monopolistic competition, there is a fierce competition between the firms in the market.

Reason (R): In monopolistic competition, there are a large number of sellers and buyers in the market.

Correct Answer: Option B - Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

Explanation:

Monopolistic Competition:

Monopolistic competition is a market structure where there are a large number of sellers who offer differentiated products. In this market structure, each firm has some control over the price of its product due to product differentiation, but there is still competition from other firms.

Explanation of Assertion (A):

In monopolistic competition, there is fierce competition between the firms in the market. This is because each firm tries to differentiate its product from competitors in order to attract customers. Firms engage in advertising, branding, and other marketing strategies to create a unique image for their products. This creates competition among the firms as they try to capture a larger market share.

Explanation of Reason (R):

In monopolistic competition, there are indeed a large number of sellers and buyers in the market. This market structure is characterized by having many firms, each producing a slightly different product. This variety of products gives consumers choices and allows them to switch between different brands. Similarly, there are many firms competing for the same set of customers, which leads to intense competition.

Explanation of Correct Answer:

Both Assertion (A) and Reason (R) are true. In monopolistic competition, there is indeed fierce competition between firms, and there are a large number of sellers and buyers in the market. However, Reason (R) is not the correct explanation of the Assertion (A). The reason does not directly explain why there is fierce competition in monopolistic competition. The presence of a large number of sellers and buyers in the market is a characteristic of the market structure, but it does not directly explain the intensity of competition among the firms. The intense competition arises due to firms' efforts to differentiate their products and attract customers.

Assertion (A): In monopolistic competition, there is a fierce competition between the firms in the market.

Reason (R): In monopolistic competition, there are a large number of sellers and buyers in the market.

Correct Answer: Option B - Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

Explanation:

Monopolistic Competition:

Monopolistic competition is a market structure where there are a large number of sellers who offer differentiated products. In this market structure, each firm has some control over the price of its product due to product differentiation, but there is still competition from other firms.

Explanation of Assertion (A):

In monopolistic competition, there is fierce competition between the firms in the market. This is because each firm tries to differentiate its product from competitors in order to attract customers. Firms engage in advertising, branding, and other marketing strategies to create a unique image for their products. This creates competition among the firms as they try to capture a larger market share.

Explanation of Reason (R):

In monopolistic competition, there are indeed a large number of sellers and buyers in the market. This market structure is characterized by having many firms, each producing a slightly different product. This variety of products gives consumers choices and allows them to switch between different brands. Similarly, there are many firms competing for the same set of customers, which leads to intense competition.

Explanation of Correct Answer:

Both Assertion (A) and Reason (R) are true. In monopolistic competition, there is indeed fierce competition between firms, and there are a large number of sellers and buyers in the market. However, Reason (R) is not the correct explanation of the Assertion (A). The reason does not directly explain why there is fierce competition in monopolistic competition. The presence of a large number of sellers and buyers in the market is a characteristic of the market structure, but it does not directly explain the intensity of competition among the firms. The intense competition arises due to firms' efforts to differentiate their products and attract customers.

At producer’s equilibrium when MR=MC, the firm earns only- a)Abnormal loss

- b)Abnormal profit

- c)Normal Profit

- d)Normal loss

Correct answer is option 'C'. Can you explain this answer?

At producer’s equilibrium when MR=MC, the firm earns only

a)

Abnormal loss

b)

Abnormal profit

c)

Normal Profit

d)

Normal loss

|

|

Anjali Sharma answered |

Producer’s equilibrium refers to the state in which a producer earns his maximum profit or minimises its losses. According to the MR-MC approach, the producer is at equilibrium when the Marginal Revenue (MR) is equal to the Marginal Cost (MC), and the Marginal Cost curve must cut the Marginal Revenue curve from below.

Two conditions under this approach are:

(i) MR = MC

(ii) MC curve should cut the MR curve from below, or MC should be rising.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): Government imposes price floor to protect the interest of the producers.Reason (R): Price floor makes the goods beneficial for the sellers to sell in the market.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'B'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): Government imposes price floor to protect the interest of the producers.

Reason (R): Price floor makes the goods beneficial for the sellers to sell in the market.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Kiran Mehta answered |

The government imposes lower limit on the price that may be charged for a particular good or service is called price floor. When equilibrium price determined by market forces of demand and supply is considered to be unremunerative for the producer, the government intervenes to protect the interest of producers.

Marginal revenue in any competitive situation is?- a)Trn-Pn-1

- b)TRn-TRn-1

- c)TRn/Qn-1

- d)None of above

Correct answer is option 'B'. Can you explain this answer?

Marginal revenue in any competitive situation is?

a)

Trn-Pn-1

b)

TRn-TRn-1

c)

TRn/Qn-1

d)

None of above

|

Neha Choudhury answered |

Marginal revenue (MR) can be defined as additional revenue gained from the additional unit of output. Marginal revenue is the change in total revenue which results from the sale of one more or one less unit of output.

Formula:

Total revenue=TR

Total Unit = n

Total Unit less one unit = n-1

MR= TRn-TRn-1.

Formula:

Total revenue=TR

Total Unit = n

Total Unit less one unit = n-1

MR= TRn-TRn-1.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): There is no restriction on the entry and exit of the firms in the perfect competitive market.Reason (R): The perfect competition market is characterised by the sellers being a price taker and not a price maker.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'B'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): There is no restriction on the entry and exit of the firms in the perfect competitive market.

Reason (R): The perfect competition market is characterised by the sellers being a price taker and not a price maker.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

Maitri Sharma answered |

Assertion (A): There is no restriction on the entry and exit of the firms in the perfect competitive market.

Reason (R): The perfect competition market is characterized by the sellers being a price taker and not a price maker.

The correct answer is option 'B' - Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

Explanation:

Perfect competition is a market structure where there are many buyers and sellers, and no individual firm has control over the market price. In this type of market, there are no restrictions on the entry and exit of firms. Let's examine each statement in detail:

Assertion (A): There is no restriction on the entry and exit of the firms in the perfect competitive market.

In a perfectly competitive market, new firms are free to enter the market if they believe they can earn profits. Similarly, existing firms are free to exit the market if they are incurring losses. There are no legal or regulatory barriers that prevent firms from entering or exiting the market. This is because perfect competition promotes competition and allows for efficient allocation of resources.

Reason (R): The perfect competition market is characterized by the sellers being a price taker and not a price maker.

In a perfectly competitive market, each firm is a price taker, meaning they have no control over the market price. The market price is determined by the overall supply and demand in the market. Individual firms have to accept the prevailing market price and adjust their quantity of production accordingly. They cannot influence the market price by changing their output. This is because there are many buyers and sellers in the market, and no individual firm has enough market power to affect the market price.

Explanation of the Correct Answer:

Both Assertion (A) and Reason (R) are true. In a perfectly competitive market, there are no restrictions on the entry and exit of firms, and sellers are price takers. However, Reason (R) does not provide a direct explanation for Assertion (A). The fact that sellers are price takers does not necessarily imply that there are no restrictions on entry and exit. Therefore, option 'B' is the correct answer.

Reason (R): The perfect competition market is characterized by the sellers being a price taker and not a price maker.

The correct answer is option 'B' - Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

Explanation:

Perfect competition is a market structure where there are many buyers and sellers, and no individual firm has control over the market price. In this type of market, there are no restrictions on the entry and exit of firms. Let's examine each statement in detail:

Assertion (A): There is no restriction on the entry and exit of the firms in the perfect competitive market.

In a perfectly competitive market, new firms are free to enter the market if they believe they can earn profits. Similarly, existing firms are free to exit the market if they are incurring losses. There are no legal or regulatory barriers that prevent firms from entering or exiting the market. This is because perfect competition promotes competition and allows for efficient allocation of resources.

Reason (R): The perfect competition market is characterized by the sellers being a price taker and not a price maker.

In a perfectly competitive market, each firm is a price taker, meaning they have no control over the market price. The market price is determined by the overall supply and demand in the market. Individual firms have to accept the prevailing market price and adjust their quantity of production accordingly. They cannot influence the market price by changing their output. This is because there are many buyers and sellers in the market, and no individual firm has enough market power to affect the market price.

Explanation of the Correct Answer:

Both Assertion (A) and Reason (R) are true. In a perfectly competitive market, there are no restrictions on the entry and exit of firms, and sellers are price takers. However, Reason (R) does not provide a direct explanation for Assertion (A). The fact that sellers are price takers does not necessarily imply that there are no restrictions on entry and exit. Therefore, option 'B' is the correct answer.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): Reliance has a monopoly in the sector of telecommunication with its Jio in India.Reason (R): Monopoly is characterised when there is only one seller in the market and the firm is a price maker.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'D'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): Reliance has a monopoly in the sector of telecommunication with its Jio in India.

Reason (R): Monopoly is characterised when there is only one seller in the market and the firm is a price maker.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

Prashanth Banerjee answered |

Understanding the Assertion and Reason

The statement involves analyzing the relationship between the assertion about Reliance's monopoly in telecommunications and the reasoning behind the definition of monopoly.

Assertion (A): Reliance has a monopoly in the sector of telecommunications with its Jio in India.

Reason (R): Monopoly is characterized when there is only one seller in the market, and the firm is a price maker.

Analysis of Assertion (A)

- False Assertion:

- While Reliance Jio is a significant player in the Indian telecommunications market, it does not hold a monopoly.

- The Indian telecom sector has multiple competitors, including Airtel, Vodafone-Idea, and others.

- Therefore, the market is characterized by competition rather than a single seller.

Analysis of Reason (R)

- True Reason:

- The definition provided for monopoly is accurate.

- A monopoly exists when a single seller controls the entire market and can set prices without competition.

Conclusion

- Given that Assertion (A) is false and Reason (R) is true, the correct choice is:

Option D: Assertion (A) is false, but Reason (R) is true.

This analysis clarifies that while the concept of monopoly is correctly defined, the statement regarding Reliance Jio's position in the telecommunications market is incorrect, as it faces substantial competition.

The statement involves analyzing the relationship between the assertion about Reliance's monopoly in telecommunications and the reasoning behind the definition of monopoly.

Assertion (A): Reliance has a monopoly in the sector of telecommunications with its Jio in India.

Reason (R): Monopoly is characterized when there is only one seller in the market, and the firm is a price maker.

Analysis of Assertion (A)

- False Assertion:

- While Reliance Jio is a significant player in the Indian telecommunications market, it does not hold a monopoly.

- The Indian telecom sector has multiple competitors, including Airtel, Vodafone-Idea, and others.

- Therefore, the market is characterized by competition rather than a single seller.

Analysis of Reason (R)

- True Reason:

- The definition provided for monopoly is accurate.

- A monopoly exists when a single seller controls the entire market and can set prices without competition.

Conclusion

- Given that Assertion (A) is false and Reason (R) is true, the correct choice is:

Option D: Assertion (A) is false, but Reason (R) is true.

This analysis clarifies that while the concept of monopoly is correctly defined, the statement regarding Reliance Jio's position in the telecommunications market is incorrect, as it faces substantial competition.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): Government imposes price ceiling to protect the consumers.Reason (R): Price ceiling is imposed on essential commodities.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'B'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): Government imposes price ceiling to protect the consumers.

Reason (R): Price ceiling is imposed on essential commodities.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Amita Das answered |

A price ceiling is a limit on the price of a good or service imposed by the government to protect consumers. Consumer behavior reveals how to appeal to people with different habits by ensuring that prices do not become prohibitively expensive.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): In oligopoly market, the firms restrict the entry of new firms.Reason (R): Oligopoly market has few sellers which influence the decisions of the market and restrict the entry of new firms.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'A'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): In oligopoly market, the firms restrict the entry of new firms.

Reason (R): Oligopoly market has few sellers which influence the decisions of the market and restrict the entry of new firms.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Kiran Mehta answered |

One important source of oligopoly power is barriers to entry. Barriers to entry are obstacles that make it difficult to enter a given market. This means that new firms cannot enter the market whenever existing firms are making a positive economic profit, as is the case in perfect competition.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): The industries today are moving towards being perfect competitive market.Reason (R): In perfect competitive market, the firms sell homogeneous products.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'D'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): The industries today are moving towards being perfect competitive market.

Reason (R): In perfect competitive market, the firms sell homogeneous products.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Priyanka Khatri answered |

Perfect competition is a type of market structure where products are homogeneous and there are many buyers and sellers. It is held as the ideal market structure for economies to operate in.

Direction: Read the following passage and answer the questions that follows:A price floor is the lowest legal price that can be paid in a market for goods and services, labour, or financial capital. Perhaps the best-known example of a price floor is the minimum wage, which is based on the normative view that someone working full time ought to be able to afford a basic standard of living. The federal minimum wage at the end of 2014 was $7.25 per hour, which yields an income for a single person slightly higher than the poverty line. As the cost of living rises over time, Congress periodically raises the federal minimum wage.Price floors are sometimes called price supports because they support a price by preventing it from falling below a certain level. Around the world, many countries have passed laws to create agricultural price supports. Farm prices, and thus farm incomes, fluctuate—sometimes widely. So even if, on average, farm incomes are adequate, some years they can be quite low. The purpose of price supports is to prevent these swings.The most common way price supports work is that the government enters the market and buys up the product, adding to demand to keep prices higher than they otherwise would be.Q. Read the following statements–Assertion (A) and Reason (R).Assertion (A): Price floor is also known as price support.Reason (R): Price floor supports a price from falling the certain level Select the correct alternative from the following:- a)Both Assertion (A) and Reason ( R) are true.

- b)Both Assertion (A) and Reason (R) are false.

Correct answer is option 'A'. Can you explain this answer?

Direction: Read the following passage and answer the questions that follows:

A price floor is the lowest legal price that can be paid in a market for goods and services, labour, or financial capital. Perhaps the best-known example of a price floor is the minimum wage, which is based on the normative view that someone working full time ought to be able to afford a basic standard of living. The federal minimum wage at the end of 2014 was $7.25 per hour, which yields an income for a single person slightly higher than the poverty line. As the cost of living rises over time, Congress periodically raises the federal minimum wage.

Price floors are sometimes called price supports because they support a price by preventing it from falling below a certain level. Around the world, many countries have passed laws to create agricultural price supports. Farm prices, and thus farm incomes, fluctuate—sometimes widely. So even if, on average, farm incomes are adequate, some years they can be quite low. The purpose of price supports is to prevent these swings.

The most common way price supports work is that the government enters the market and buys up the product, adding to demand to keep prices higher than they otherwise would be.

Q. Read the following statements–Assertion (A) and Reason (R).

Assertion (A): Price floor is also known as price support.

Reason (R): Price floor supports a price from falling the certain level

Select the correct alternative from the following:

a)

Both Assertion (A) and Reason ( R) are true.

b)

Both Assertion (A) and Reason (R) are false.

|

Anu Basu answered |

Understanding Price Floor and Price Support

The assertion and reason presented in the passage are both true, which is why option 'A' is the correct answer. Here’s a detailed explanation:

Assertion (A): Price Floor is also known as Price Support

- Price floors, such as the minimum wage, are designed to maintain a minimum price level in various markets.

- They prevent prices from dropping below a certain threshold, which is essential for ensuring that producers, such as farmers, receive fair compensation for their goods and services.

- This concept is often referred to as "price support" because it supports the price level, protecting the income of those affected.

Reason (R): Price Floor Supports a Price from Falling Below a Certain Level

- The purpose of a price floor is to prevent prices from falling too low, which can lead to negative economic consequences like reduced income for workers or farmers.

- Governments implement price floors to stabilize market prices and provide a safety net during periods of economic downturns or agricultural fluctuations.

- For example, in agriculture, governments may intervene by purchasing surplus products to maintain higher prices, thus supporting farmers' incomes.

Conclusion

- Since both the assertion and reason accurately reflect the characteristics and functions of price floors, they align with the definition provided in the passage.

- Therefore, both statements being true supports the conclusion that option 'A' is correct.

This understanding helps clarify the role of price floors in economic policy and market regulation.

The assertion and reason presented in the passage are both true, which is why option 'A' is the correct answer. Here’s a detailed explanation:

Assertion (A): Price Floor is also known as Price Support

- Price floors, such as the minimum wage, are designed to maintain a minimum price level in various markets.

- They prevent prices from dropping below a certain threshold, which is essential for ensuring that producers, such as farmers, receive fair compensation for their goods and services.

- This concept is often referred to as "price support" because it supports the price level, protecting the income of those affected.

Reason (R): Price Floor Supports a Price from Falling Below a Certain Level

- The purpose of a price floor is to prevent prices from falling too low, which can lead to negative economic consequences like reduced income for workers or farmers.

- Governments implement price floors to stabilize market prices and provide a safety net during periods of economic downturns or agricultural fluctuations.

- For example, in agriculture, governments may intervene by purchasing surplus products to maintain higher prices, thus supporting farmers' incomes.

Conclusion

- Since both the assertion and reason accurately reflect the characteristics and functions of price floors, they align with the definition provided in the passage.

- Therefore, both statements being true supports the conclusion that option 'A' is correct.

This understanding helps clarify the role of price floors in economic policy and market regulation.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): Increase or decrease in demand causes a change in the price of the commodity. Equilibrium quantity remains constant.Reason (R): When demand increases more than supply, equilibrium price will increase.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'C'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): Increase or decrease in demand causes a change in the price of the commodity. Equilibrium quantity remains constant.

Reason (R): When demand increases more than supply, equilibrium price will increase.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Amita Das answered |

An increase in demand while the supply remains unchanged causes equilibrium price and quantity to increase. Due to increase in demand the quantity demanded will increase this will thereby increase competition in the market which will leaf to increase in price of the product. hence, when the price increases demand decreases to reach to equilibrium and new equilibrium quantity and price will be derived.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): Monopolistic competition market has free entry and exit of the firms.Reason (R): There is a presence of non-price competition in the market.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'B'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): Monopolistic competition market has free entry and exit of the firms.

Reason (R): There is a presence of non-price competition in the market.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Naina Sharma answered |

Monopolistically competitive markets exhibit the following characteristics: There is freedom to enter or leave the market, as there are no major barriers to entry or exit. A central feature of monopolistic competition is that products are differentiated.

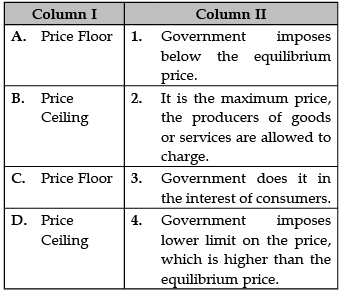

Identify the correct pair of items from the following Columns I and II:

- a)A–1

- b)B–2

- c)C–3

- d)D–4

Correct answer is option 'B'. Can you explain this answer?

Identify the correct pair of items from the following Columns I and II:

a)

A–1

b)

B–2

c)

C–3

d)

D–4

|

|

Arun Yadav answered |

A. Price Floor: Price floor is a situation when the price charged is more than or less than the equilibrium price determined by market forces of demand and supply. By observation, it has been found that lower price floors are ineffective. Price floor leads to a lesser number of workers than in case of equilibrium wage.

B. Price Ceiling: A price ceiling is the mandated maximum amount a seller is allowed to charge for a product or service. Usually set by law, price ceilings are typically applied to staples such as food and energy products when such goods become unaffordable to regular consumers.

C. Price Floor: Price floor is a situation when the price charged is more than or less than the equilibrium price determined by market forces of demand and supply. By observation, it has been found that lower price floors are ineffective. Price floor leads to a lesser number of workers than in case of equilibrium wage.

D. Price Ceiling: A price ceiling is the mandated maximum amount a seller is allowed to charge for a product or service. Usually set by law, price ceilings are typically applied to staples such as food and energy products when such goods become unaffordable to regular consumers.

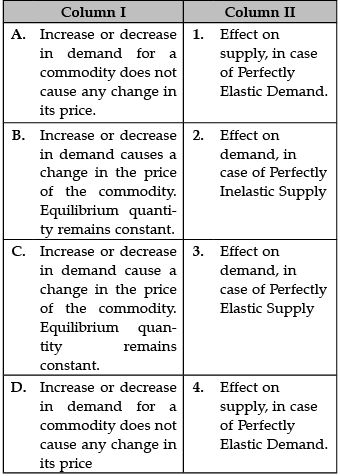

Identify the correct pair of items from the following Columns I and II:

- a)A–1

- b)B–2

- c)C–3

- d)D–4

Correct answer is option 'B'. Can you explain this answer?

Identify the correct pair of items from the following Columns I and II:

a)

A–1

b)

B–2

c)

C–3

d)

D–4

|

|

Naina Sharma answered |

A. Effect on supply, in case of perfectly Elastic Demand: If supply is perfectly elastic, it means that any change in price will result in an infinite amount of change in quantity.

B. Effect on demand, in case of Perfectly Inelastic Supply: When demand is perfectly inelastic, quantity demanded for a good does not change in response to a change in price. Finally, demand is said to be perfectly elastic when the PED coefficient is equal to infinity. When demand is perfectly elastic, buyers will only buy at one price and no other.

C. Effect on demand, in case of Perfectly Elastic Supply: The PES for perfectly elastic supply is infinite, where the quantity supplied is unlimited at a given price, but no quantity can be supplied at any other price.

D. Effect on supply, in case of Perfectly Elastic Demand: If supply is perfectly elastic, it means that any change in price will result in an infinite amount of change in quantity.

Identify the correctly matched statements from the Column I to that of Column II:

- a)A–1

- b)B–2

- c)C–3

- d)D–4

Correct answer is option 'D'. Can you explain this answer?

Identify the correctly matched statements from the Column I to that of Column II:

a)

A–1

b)

B–2

c)

C–3

d)

D–4

|

|

Amita Das answered |

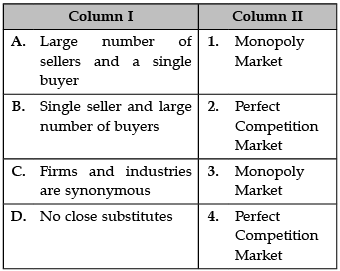

- Monopoly: A monopoly is a firm who is the sole seller of its product, and where there are no close substitutes. An unregulated monopoly has market power and can influence prices. Examples: Microsoft and Windows, DeBeers and diamonds, your local natural gas company.

- Perfect Competition: Perfect competition is an ideal type of market structure where all producers and consumers have full and symmetric information, no transaction costs, where there are a large number of producers and consumers competing with one another. Perfect competition is theoretically the opposite of a monopolistic market. Examples of this perfect market structure are: A large number of buyers. A large number of sellers. Every participant is a price taker, not having the ability to influence market prices.

- Monopolistic competition: Monopolistic competitive markets have highly differentiated products; have many firms providing the good or service; firms can freely enter and exits in the long-run; firms can make decisions independently; there is some degree of market power; and buyers and sellers have imperfect information.

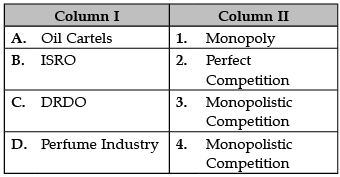

Identify the correctly matched items from Column I to that of Column II:

- a)A–1

- b)B–2

- c)C–3

- d)D–4

Correct answer is option 'C'. Can you explain this answer?

Identify the correctly matched items from Column I to that of Column II:

a)

A–1

b)

B–2

c)

C–3

d)

D–4

|

|

Amita Das answered |

- Monopoly Market: A market structure characterized by a single seller, selling a unique product in the market. In a monopoly market, the seller faces no competition, as he is the sole seller of goods with no close substitute. He enjoys the power of setting the price for his goods.

- Perfect Competition Market: Perfect competition is an ideal type of market structure where all producers and consumers have full and symmetric information, no transaction costs, where there are a large number of producers and consumers competing with one another. Perfect competition is theoretically the opposite of a monopolistic market.

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:Assertion (A): The deodorant industry is a monopolistic competitive market.Reason (R): There are a lot of varieties of deodorants present in the market.- a)Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

- b)Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

- c)Assertion (A) is true, but Reason (R) is false.

- d)Assertion (A) is false, but Reason (R) is true.

Correct answer is option 'A'. Can you explain this answer?

Direction: In the following questions, a statement of Assertion (A) is followed by a statement of Reason (R). Mark the correct choice as:

Assertion (A): The deodorant industry is a monopolistic competitive market.

Reason (R): There are a lot of varieties of deodorants present in the market.

a)

Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of the Assertion (A).

b)

Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of the Assertion (A).

c)

Assertion (A) is true, but Reason (R) is false.

d)

Assertion (A) is false, but Reason (R) is true.

|

|

Naina Sharma answered |

Soap, shampoo, deodorants, shaving cream, cold remedies, and many other items found in a drugstore are sold in monopolistic ally competitive markets. The markets for bicycles and other sporting goods are likewise monopolistic and all competitive.

Identify the correctly matched items from Column I to that of Column II:

- a)A–1

- b)B–2

- c)C–3

- d)D–4

Correct answer is option 'A'. Can you explain this answer?

Identify the correctly matched items from Column I to that of Column II:

a)

A–1

b)

B–2

c)

C–3

d)

D–4

|

|

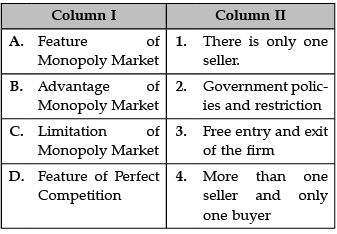

Kiran Mehta answered |

A. Features of Monopoly Market: A monopoly market is characterized by the profit maximizer, price maker, high barriers to entry, single seller, and price discrimination. Monopoly characteristics include profit maximizer, price maker, high barriers to entry, single seller, and price discrimination.

B. Advantages of Monopoly Market: The advantage of monopolies is the assurance of a consistent supply of a commodity that is too expensive to provide in a competitive market.

C. Limitation of Monopoly Market: A monopoly market is characterized by the profit maximizer, price maker, high barriers to entry, single seller, and price discrimination. Monopoly characteristics include profit maximizer, price maker, high barriers to entry, single seller, and price discrimination.

D. Feature of Perfect Competition: A perfectly competitive market is characterized by many buyers and sellers, undifferentiated products, no transaction costs, no barriers to entry and exit, and perfect information about the price of a good. The total revenue for a firm in a perfectly competitive market is the product of price and quantity (TR = P * Q).

MR curve=AR=Demand curve is a feature of which kind of market?- a)Perfect competition

- b)Oligopoly

- c)Monopolistic competition

- d)Monopoly

Correct answer is option 'A'. Can you explain this answer?

MR curve=AR=Demand curve is a feature of which kind of market?

a)

Perfect competition

b)

Oligopoly

c)

Monopolistic competition

d)

Monopoly

|

|

Pj Commerce Academy answered |

MR curve=AR=Demand curve is a feature of which kind of market?

The feature of MR curve=AR=Demand curve is characteristic of a perfect competition market. In a perfect competition market, there are numerous buyers and sellers of homogeneous products. Here is a detailed explanation:

1. Perfect competition:

- Perfect competition is a market structure where there are many buyers and sellers.

- The products sold in this market are identical or homogeneous, meaning they are indistinguishable from each other.

- There is free entry and exit of firms in the market, allowing for easy competition.

- The information is perfect, and all participants have full knowledge of prices and market conditions.

- In perfect competition, firms are price takers, meaning they cannot influence the market price.

- The demand curve faced by a firm in perfect competition is perfectly elastic, i.e., horizontal.

- Marginal revenue (MR) is equal to average revenue (AR), which is equal to the demand curve.

2. MR curve=AR=Demand curve:

- In perfect competition, since the firm is a price taker, it can only sell its output at the prevailing market price.