All Exams >

Commerce >

Economics CUET Preparation >

All Questions

All questions of Market Equilibrium for Commerce Exam

| 1 Crore+ students have signed up on EduRev. Have you? Download the App |

During excess demand- a)Market price is lower than the equilibrium price

- b)Market price is higher than the equilibrium price

- c)Market price is same as the equilibrium price

- d)None of these

Correct answer is option 'A'. Can you explain this answer?

During excess demand

a)

Market price is lower than the equilibrium price

b)

Market price is higher than the equilibrium price

c)

Market price is same as the equilibrium price

d)

None of these

|

|

Arun Khanna answered |

Excess Demand:

Excess demand refers to the situation when aggregate demand (AD) is more than the aggregate supply (AS) corresponding to full employment level of output in the economy. It is the excess of anticipated expenditure over the value of full employment output.

During deficient demand- a)Competition among sellers start

- b)Competition in the government start

- c)Competition among buyers start

- d)Competition among exporters start

Correct answer is option 'A'. Can you explain this answer?

During deficient demand

a)

Competition among sellers start

b)

Competition in the government start

c)

Competition among buyers start

d)

Competition among exporters start

|

|

Om Desai answered |

Excess Demand. When at the current price level, the quantity demanded is more than quantity supplied, a situation of excess demand is said to arise in the market. Excess demand occurs at a price less than the equilibrium price.

Can you explain the answer of this question below:Unfavorable change in the taste for a good leads to

- A:

Shift of the demand curve of the given good only

- B:

Movement of the demand and supply curves of the given good

- C:

Shift of the demand and supply curves of the given good

- D:

Contraction of the demand for the given good

The answer is D.

Unfavorable change in the taste for a good leads to

Shift of the demand curve of the given good only

Movement of the demand and supply curves of the given good

Shift of the demand and supply curves of the given good

Contraction of the demand for the given good

|

Kusum Chugh answered |

Ans :TASTE AND PREFERENCES --~The demand for a commodity is also affected by the taste and preference of the consumer. ~The demand for a commodity will increase if consumer’s taste changes in favour of the commodity and,~Any UNFAVORABLE CHANGE in taste or PREFERENCE will REDUCE the DEMAND for the COMMODITY.

Equilibrium price may or may not change with shifts in both demand and supply curve.- a)No

- b)Only may change

- c)Yes

- d)May not change only

Correct answer is option 'C'. Can you explain this answer?

Equilibrium price may or may not change with shifts in both demand and supply curve.

a)

No

b)

Only may change

c)

Yes

d)

May not change only

|

|

Om Desai answered |

Factors that can shift the demand curve for goods and services, causing a different quantity to be demanded at any given price, include changes in tastes, population, income, prices of substitute or complement goods, and expectations about future conditions and prices.

A rise in the price of the complementary good leads to- a)Shift of the demand curve of the given good only

- b)Expansion of the supply curve of the given good only

- c)Contraction of the demand for the given good

- d)Shift of the demand and supply curves of the given good

Correct answer is option 'C'. Can you explain this answer?

A rise in the price of the complementary good leads to

a)

Shift of the demand curve of the given good only

b)

Expansion of the supply curve of the given good only

c)

Contraction of the demand for the given good

d)

Shift of the demand and supply curves of the given good

|

|

Nandini Iyer answered |

Complementary good or complement is a good with a negative cross elasticity of demand, in contrast to a substitute good. This means a good's demand is increased when the price of another good is decreased. ... When two goods are complements, they experience joint demand.

A complementary good is a good whose use is related to the use of an associated or paired good. Two goods (A and B) are complementary if using more of good A requires the use of more of good B. For example, the demand for one good (printers) generates demand for the other (ink cartridges).

Excess demand occurs when- a)Market price fall below the equilibrium price

- b)Market price rise higher than the equilibrium price

- c)Market price remains the same

- d)none

Correct answer is option 'A'. Can you explain this answer?

Excess demand occurs when

a)

Market price fall below the equilibrium price

b)

Market price rise higher than the equilibrium price

c)

Market price remains the same

d)

none

|

|

Arjun Singhania answered |

Excess Demand. When at the current price level, the quantity demanded is more than quantity supplied, a situation of excess demand is said to arise in the market. Excess demand occurs at a price less than the equilibrium price.

Ring deficient demand- a)Market price remains the same

- b)Market price rise

- c)Market price falls below the equilibrium price

- d)Market price fall

Correct answer is option 'D'. Can you explain this answer?

Ring deficient demand

a)

Market price remains the same

b)

Market price rise

c)

Market price falls below the equilibrium price

d)

Market price fall

|

|

Rajat Patel answered |

Deficient demand refers to the situation when aggregate demand (AD) is less than the aggregate supply (AS) corresponding to full employment level of output in the economy. ... The situation of deficient demand arises when planned aggregate expenditure falls short of aggregate supply at the full employment level.

After excess demand- a)Market price rise

- b)Market price fall

- c)Market price remains the same

- d)Market price falls below the equilibrium price

Correct answer is option 'A'. Can you explain this answer?

After excess demand

a)

Market price rise

b)

Market price fall

c)

Market price remains the same

d)

Market price falls below the equilibrium price

|

|

Rajat Patel answered |

A Market Surplus occurs when there is excess supply- that is quantity supplied is greater than quantity demanded. ... In this situation, excess supply has exerted downward pressure on the price of the product. A Market Shortage occurs when there is excess demand- that is quantity demanded is greater than quantity supplied.

An imposition of tax on a good leads to- a)Shift of the demand curve of the given good only

- b)Shift of the supply curve of the given good only

- c)Rightward shift of the supply curve of the given good only

- d)Movement of the demand and supply curves of the given good

Correct answer is option 'C'. Can you explain this answer?

An imposition of tax on a good leads to

a)

Shift of the demand curve of the given good only

b)

Shift of the supply curve of the given good only

c)

Rightward shift of the supply curve of the given good only

d)

Movement of the demand and supply curves of the given good

|

|

Priyanshu Tiwari answered |

The imposition of either type of tax has an implication on the supply and demand framework. Specifically, it causes shifts in supply and demand, which in turn lead to new levels of quantity and prices in an economy.

The factor that causes a change in demand is- a)Price of the inputs

- b)An improvement in technology

- c)Price of the substitute good

- d)Price of the given good

Correct answer is option 'C'. Can you explain this answer?

The factor that causes a change in demand is

a)

Price of the inputs

b)

An improvement in technology

c)

Price of the substitute good

d)

Price of the given good

|

|

Rajdeep Rane answered |

Factors that cause a change in demand

The demand for a product or service refers to the quantity of that product or service that consumers are willing and able to purchase at a given price during a specific period. Several factors can influence the demand for a good or service, including changes in consumer preferences, income levels, population, and prices of related goods. However, among these factors, the price of substitute goods has a significant impact on the demand for a particular good or service.

Explanation:

1. Price of substitute goods:

- A substitute good is a product or service that can be used as an alternative to another good or service.

- When the price of a substitute good increases, consumers are more likely to switch to the lower-priced good, resulting in an increase in demand for the lower-priced good.

- For example, if the price of coffee increases significantly, some consumers may switch to tea as a substitute. This shift in consumer behavior would lead to an increase in the demand for tea.

- On the other hand, if the price of a substitute good decreases, consumers may choose to switch from the given good to the substitute, causing a decrease in the demand for the given good.

- The price of substitute goods is an important factor in determining consumer choices and can have a significant impact on the overall demand for a particular product or service.

Other factors that influence demand:

2. Price of the given good:

- The price of the given good itself has a direct impact on demand. When the price of a good decreases, consumers may be more willing to purchase it, resulting in an increase in demand. Conversely, when the price of a good increases, demand is likely to decrease.

3. Price of inputs:

- The cost of inputs required to produce a good or service can impact its price, which in turn affects demand. If the price of inputs increases, the cost of production will increase, leading to a higher price for the final product and potentially lower demand.

4. An improvement in technology:

- Technological advancements can lead to the production of goods and services at lower costs, which can result in lower prices and an increase in demand. Improved technology can also lead to the development of new and innovative products, which can create new demand in the market.

Conclusion:

While several factors can influence the demand for a good or service, the price of substitute goods is a crucial factor that directly affects consumer choices and can significantly impact demand. As the price of substitute goods changes, consumers may switch their preferences, leading to changes in demand for the given good or service.

The demand for a product or service refers to the quantity of that product or service that consumers are willing and able to purchase at a given price during a specific period. Several factors can influence the demand for a good or service, including changes in consumer preferences, income levels, population, and prices of related goods. However, among these factors, the price of substitute goods has a significant impact on the demand for a particular good or service.

Explanation:

1. Price of substitute goods:

- A substitute good is a product or service that can be used as an alternative to another good or service.

- When the price of a substitute good increases, consumers are more likely to switch to the lower-priced good, resulting in an increase in demand for the lower-priced good.

- For example, if the price of coffee increases significantly, some consumers may switch to tea as a substitute. This shift in consumer behavior would lead to an increase in the demand for tea.

- On the other hand, if the price of a substitute good decreases, consumers may choose to switch from the given good to the substitute, causing a decrease in the demand for the given good.

- The price of substitute goods is an important factor in determining consumer choices and can have a significant impact on the overall demand for a particular product or service.

Other factors that influence demand:

2. Price of the given good:

- The price of the given good itself has a direct impact on demand. When the price of a good decreases, consumers may be more willing to purchase it, resulting in an increase in demand. Conversely, when the price of a good increases, demand is likely to decrease.

3. Price of inputs:

- The cost of inputs required to produce a good or service can impact its price, which in turn affects demand. If the price of inputs increases, the cost of production will increase, leading to a higher price for the final product and potentially lower demand.

4. An improvement in technology:

- Technological advancements can lead to the production of goods and services at lower costs, which can result in lower prices and an increase in demand. Improved technology can also lead to the development of new and innovative products, which can create new demand in the market.

Conclusion:

While several factors can influence the demand for a good or service, the price of substitute goods is a crucial factor that directly affects consumer choices and can significantly impact demand. As the price of substitute goods changes, consumers may switch their preferences, leading to changes in demand for the given good or service.

A fall in the price of the good for a seller leads to- a)Movement of the demand and supply curves of the given good

- b)Shift of the demand curve of the given good only

- c)Shift of the demand and supply curves of the given good

- d)Contraction of the supply curve of the given good only

Correct answer is option 'D'. Can you explain this answer?

A fall in the price of the good for a seller leads to

a)

Movement of the demand and supply curves of the given good

b)

Shift of the demand curve of the given good only

c)

Shift of the demand and supply curves of the given good

d)

Contraction of the supply curve of the given good only

|

|

Ræjû Bhæï answered |

Garam money kal ko bataunga.

Deficient demand occurs when- a)Market price fall below the equilibrium price

- b)Market price rise higher than the equilibrium price

- c)Market price falls below the equilibrium price

- d)Market price remains the same

Correct answer is option 'B'. Can you explain this answer?

Deficient demand occurs when

a)

Market price fall below the equilibrium price

b)

Market price rise higher than the equilibrium price

c)

Market price falls below the equilibrium price

d)

Market price remains the same

|

Sai Kulkarni answered |

Deficient demand refers to the situation when aggregate demand (AD) is less than the aggregate supply (AS) corresponding to full employment level of output in the economy.

Market for a good is in equilibrium. An increase in supply for the good will- a)Raise the price

- b)Lower the price

- c)Only quantity exchanged is affected

- d)Price is unaffected

Correct answer is option 'B'. Can you explain this answer?

Market for a good is in equilibrium. An increase in supply for the good will

a)

Raise the price

b)

Lower the price

c)

Only quantity exchanged is affected

d)

Price is unaffected

|

|

Aryan Khanna answered |

According to basic economic theory, the supply of a good will increase when its price rises. Conversely, the supply of a good will decrease when its price decreases. There's also price elasticity of demand. This measures how responsive the quantity demanded is affected by a price change.

This a MCQ (Multiple Choice Question) based practice test of Chapter 5 - Market Equilibrium of Economics of Class XII (12) for the quick revision/preparation of School Board examinationsQ _____________ is the price at which demand for a commodity is equal to its supply?- a)Secular price

- b)Equilibrium price

- c)Short run price

- d)Normal price

Correct answer is option 'B'. Can you explain this answer?

This a MCQ (Multiple Choice Question) based practice test of Chapter 5 - Market Equilibrium of Economics of Class XII (12) for the quick revision/preparation of School Board examinations

Q _____________ is the price at which demand for a commodity is equal to its supply?

a)

Secular price

b)

Equilibrium price

c)

Short run price

d)

Normal price

|

|

Sanvi Kapoor answered |

At equilibrium price quantity demanded and quantity supplied of a commodity are equal. This quantity is called the equilibrium quantity of the commodity. In practical life, the price at which the seller/firm wants to sell a commodity, its quantity supplied may be greater or lesser than its quantity demanded.

Excess demand is a situation when- a)Market demand is equal to market supply

- b)individual demand is greater than individual supply

- c)Market demand is greater than market supply

- d)Market demand is less than market supply

Correct answer is option 'C'. Can you explain this answer?

Excess demand is a situation when

a)

Market demand is equal to market supply

b)

individual demand is greater than individual supply

c)

Market demand is greater than market supply

d)

Market demand is less than market supply

|

|

Poonam Reddy answered |

Explanation:

Excess demand is a situation that occurs when the market demand for a product or service exceeds the market supply. In this situation, there are more buyers willing and able to purchase a good or service than there are available units of that good or service.

Key Points:

- Excess demand occurs when the market demand exceeds the market supply.

- Market demand refers to the total quantity of a good or service that all buyers are willing and able to purchase at a given price.

- Market supply refers to the total quantity of a good or service that all sellers are willing and able to produce and offer for sale at a given price.

- Excess demand can lead to a shortage of the product, as there are not enough units available to satisfy all the buyers.

- When there is excess demand, buyers may compete with each other to purchase the limited supply, which can drive up the price of the product.

- Excess demand is an indicator of a seller's market, where sellers have more bargaining power and can potentially increase prices.

- In order to eliminate excess demand and restore equilibrium, either the market supply needs to increase or the market demand needs to decrease.

- Excess demand can be temporary or long-term, depending on the factors influencing supply and demand for the product or service.

Excess demand is a situation that occurs when the market demand for a product or service exceeds the market supply. In this situation, there are more buyers willing and able to purchase a good or service than there are available units of that good or service.

Key Points:

- Excess demand occurs when the market demand exceeds the market supply.

- Market demand refers to the total quantity of a good or service that all buyers are willing and able to purchase at a given price.

- Market supply refers to the total quantity of a good or service that all sellers are willing and able to produce and offer for sale at a given price.

- Excess demand can lead to a shortage of the product, as there are not enough units available to satisfy all the buyers.

- When there is excess demand, buyers may compete with each other to purchase the limited supply, which can drive up the price of the product.

- Excess demand is an indicator of a seller's market, where sellers have more bargaining power and can potentially increase prices.

- In order to eliminate excess demand and restore equilibrium, either the market supply needs to increase or the market demand needs to decrease.

- Excess demand can be temporary or long-term, depending on the factors influencing supply and demand for the product or service.

The factor that causes a change in supply is- a)Price of the substitute good

- b)Price of the given good

- c)Price of the inputs

- d)Price of the complementary good

Correct answer is option 'C'. Can you explain this answer?

The factor that causes a change in supply is

a)

Price of the substitute good

b)

Price of the given good

c)

Price of the inputs

d)

Price of the complementary good

|

|

Priyanshu Tiwari answered |

Supply is not constant over time. It constantly increases or decreases. Whenever a change in supply occurs, the supply curve shifts left or right. There are a number of factors that cause a shift in the supply curve: input prices, number of sellers, technology, natural and social factors, and expectations

Market for a good is in equilibrium. A decrease in supply for the good will- a)Price is unaffected

- b)Only quantity exchanged is affected

- c)Lower the price

- d)Raise the price

Correct answer is option 'D'. Can you explain this answer?

Market for a good is in equilibrium. A decrease in supply for the good will

a)

Price is unaffected

b)

Only quantity exchanged is affected

c)

Lower the price

d)

Raise the price

|

|

Om Desai answered |

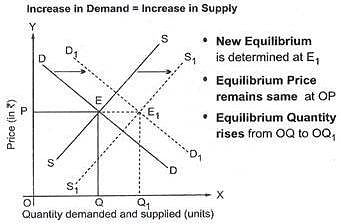

A decrease in demand and an increase in supply will cause a fall in equilibrium price, but the effect on equilibrium quantity cannot be determined. ... For any quantity, consumers now place a lower value on the good, and producers are willing to accept a lower price; therefore, price will fall.

Market for a good is in equilibrium. A decrease in price for the good will- a)Shift the demand curve

- b)Shift the supply curve

- c)Move the supply curve

- d)None of these

Correct answer is option 'C'. Can you explain this answer?

Market for a good is in equilibrium. A decrease in price for the good will

a)

Shift the demand curve

b)

Shift the supply curve

c)

Move the supply curve

d)

None of these

|

Sajid Hussain answered |

When only price will decrease or increase then moment will occur and other factors being constant.

Market equilibrium is a situation when- a)Market demand is less than market supply

- b)Market demand is greater than market supply

- c)Market Demand equals market supply

- d)None of these

Correct answer is option 'C'. Can you explain this answer?

Market equilibrium is a situation when

a)

Market demand is less than market supply

b)

Market demand is greater than market supply

c)

Market Demand equals market supply

d)

None of these

|

|

Dhruba Ghoshal answered |

Market Equilibrium:

Market equilibrium is a state of balance in a market where the quantity demanded by consumers is equal to the quantity supplied by producers. In other words, it is the point at which the demand and supply curves intersect, and there is no excess demand or excess supply in the market. When a market is in equilibrium, there is no pressure for prices to change, and both buyers and sellers are satisfied.

Explanation:

The correct answer to the given question is option C, which states that market demand equals market supply. Let's understand why this is the correct answer:

Market Demand:

Market demand refers to the total quantity of a product or service that consumers are willing and able to purchase at a given price during a specific period. It is determined by various factors such as price, income, tastes and preferences, and the availability of substitutes. The market demand curve is downward sloping, indicating that as the price of a product decreases, the quantity demanded increases, ceteris paribus.

Market Supply:

Market supply refers to the total quantity of a product or service that producers are willing and able to offer for sale at a given price during a specific period. It is determined by factors such as the cost of production, technology, resource availability, and government policies. The market supply curve is upward sloping, indicating that as the price of a product increases, the quantity supplied also increases, ceteris paribus.

Market Equilibrium:

Market equilibrium occurs when the quantity demanded by consumers is equal to the quantity supplied by producers at a specific price. At this point, there is no excess demand or excess supply in the market. The equilibrium price, also known as the market clearing price, is the price at which the quantity demanded equals the quantity supplied. It is determined by the intersection of the demand and supply curves.

Visual Representation:

To visually represent market equilibrium, we can draw a graph with price on the y-axis and quantity on the x-axis. The demand curve slopes downwards, while the supply curve slopes upwards. The point where these two curves intersect represents the equilibrium price and quantity.

Conclusion:

In conclusion, market equilibrium is a state of balance in a market where the quantity demanded equals the quantity supplied. It is the point at which the demand and supply curves intersect, and there is no excess demand or excess supply. Market equilibrium is an important concept in economics as it helps to determine the market price and quantity of a product or service.

Market equilibrium is a state of balance in a market where the quantity demanded by consumers is equal to the quantity supplied by producers. In other words, it is the point at which the demand and supply curves intersect, and there is no excess demand or excess supply in the market. When a market is in equilibrium, there is no pressure for prices to change, and both buyers and sellers are satisfied.

Explanation:

The correct answer to the given question is option C, which states that market demand equals market supply. Let's understand why this is the correct answer:

Market Demand:

Market demand refers to the total quantity of a product or service that consumers are willing and able to purchase at a given price during a specific period. It is determined by various factors such as price, income, tastes and preferences, and the availability of substitutes. The market demand curve is downward sloping, indicating that as the price of a product decreases, the quantity demanded increases, ceteris paribus.

Market Supply:

Market supply refers to the total quantity of a product or service that producers are willing and able to offer for sale at a given price during a specific period. It is determined by factors such as the cost of production, technology, resource availability, and government policies. The market supply curve is upward sloping, indicating that as the price of a product increases, the quantity supplied also increases, ceteris paribus.

Market Equilibrium:

Market equilibrium occurs when the quantity demanded by consumers is equal to the quantity supplied by producers at a specific price. At this point, there is no excess demand or excess supply in the market. The equilibrium price, also known as the market clearing price, is the price at which the quantity demanded equals the quantity supplied. It is determined by the intersection of the demand and supply curves.

Visual Representation:

To visually represent market equilibrium, we can draw a graph with price on the y-axis and quantity on the x-axis. The demand curve slopes downwards, while the supply curve slopes upwards. The point where these two curves intersect represents the equilibrium price and quantity.

Conclusion:

In conclusion, market equilibrium is a state of balance in a market where the quantity demanded equals the quantity supplied. It is the point at which the demand and supply curves intersect, and there is no excess demand or excess supply. Market equilibrium is an important concept in economics as it helps to determine the market price and quantity of a product or service.

Chapter doubts & questions for Market Equilibrium - Economics CUET Preparation 2024 is part of Commerce exam preparation. The chapters have been prepared according to the Commerce exam syllabus. The Chapter doubts & questions, notes, tests & MCQs are made for Commerce 2024 Exam. Find important definitions, questions, notes, meanings, examples, exercises, MCQs and online tests here.

Chapter doubts & questions of Market Equilibrium - Economics CUET Preparation in English & Hindi are available as part of Commerce exam.

Download more important topics, notes, lectures and mock test series for Commerce Exam by signing up for free.

Economics CUET Preparation

172 videos|18 docs|76 tests

|

Signup to see your scores go up within 7 days!

Study with 1000+ FREE Docs, Videos & Tests

10M+ students study on EduRev

|

© EduRev

|

Education Revolution

|

Follow Us

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup