Previous Year Questions: Economics- 1 - UPSC MCQ

30 Questions MCQ Test - Previous Year Questions: Economics- 1

The Phillip’s curve is the schedule showing the relationship between

A firm practising price discrimination will be

Minimum payment of factor of production is called

In a capitalistic economy the prices are determined by

A 'want' becomes a 'demand' only when it is backed by the

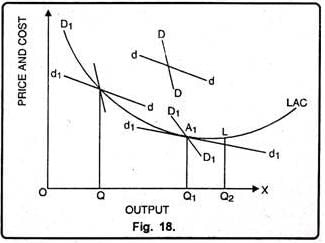

Under which market condition do firms have excess capacity?

“Economics is what it ought to be”. This statement refers to

Which one of the following is NOT a method of measurement of National Income?

Labour intensive technique would get choosen in a

Surplus earned by a factor other than land in the short period is referred to as

If two commodities are complements, then their cross-price elasticity is

Opportunity cost of production of a commodity is

Which one of the following is a developmental expenditure?

The national income consists of a collection of goods and services reduced to common basis by being measured in terms of money. Who says this?

All of the goods which are scarce and limited in supply are called

Engel’s Law states the relationship between

An expenditure that has been made and cannot be recovered is called

Seawater, fresh air etc are regarded in economics as

Excise duty on a commodity is payable with reference to its

Important Questions for Previous Year Questions: Economics- 1

Previous Year Questions: Economics- 1 MCQs with Answers

Online Tests for Previous Year Questions: Economics- 1

|

© EduRev

|

Education Revolution

|

|