Railways Exam > Railways Questions > The break-even point can be lowered bya)Incre...

Start Learning for Free

The break-even point can be lowered by

- a)Increasing the fixed costs

- b)Increasing the variable costs

- c)Decreasing the slope of the income line

- d)Reducing the variable cost

Correct answer is option 'D'. Can you explain this answer?

| FREE This question is part of | Download PDF Attempt this Test |

Verified Answer

The break-even point can be lowered bya)Increasing the fixed costsb)In...

Breakeven analysis is used to find the minimum level of production required. It evaluates both fixed and variable costs.

A breakeven analysis is used to determine how much sales volume your business needs to start making a profit, based on your fixed costs, variable costs, and selling price.

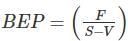

Break-even analysis consists of:

- Fixed cost (F)

- Variable cost (V)

- Sales revenue (S)

In can be seen that BEP will decrease when Fixed cost and variable cost will decrease.

BEP will decrease when selling cost increase or the slope of the income line will decrease.

Most Upvoted Answer

The break-even point can be lowered bya)Increasing the fixed costsb)In...

Explanation:

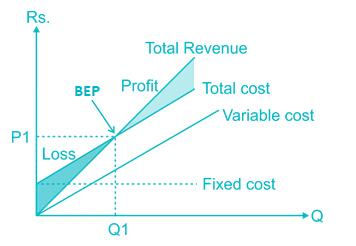

The break-even point is the point at which total revenue equals total costs, resulting in zero profit or loss. It is the level of sales or production at which a company neither makes a profit nor incurs a loss. Lowering the break-even point means reducing the amount of sales or production required to cover all costs.

Factors Affecting Break-Even Point:

There are several factors that can affect the break-even point, and these include both fixed costs and variable costs.

1. Fixed Costs:

- Fixed costs are expenses that do not change with the level of production or sales.

- Examples of fixed costs include rent, salaries, insurance, and depreciation.

- Increasing fixed costs would raise the break-even point because more sales or production would be required to cover these higher costs.

2. Variable Costs:

- Variable costs are expenses that change in proportion to the level of production or sales.

- Examples of variable costs include raw materials, direct labor, and utilities.

- Increasing variable costs would raise the break-even point because more sales or production would be required to cover these higher costs.

3. Slope of the Income Line:

- The slope of the income line represents the profit margin per unit of sales.

- A steeper slope indicates a higher profit margin, while a flatter slope indicates a lower profit margin.

- Decreasing the slope of the income line would lower the break-even point because it means that less sales or production would be required to achieve the same level of profit.

4. Reducing Variable Costs:

- Reducing variable costs would lower the break-even point because it means that less sales or production would be required to cover these lower costs.

- This can be achieved through various means such as negotiating better prices with suppliers, improving operational efficiency, or finding alternative raw materials.

Conclusion:

Out of the given options, reducing the variable cost (Option D) is the correct answer to lower the break-even point. By reducing variable costs, a company can achieve a lower break-even point, meaning that it would require fewer sales or production to cover its costs and start making a profit.

The break-even point is the point at which total revenue equals total costs, resulting in zero profit or loss. It is the level of sales or production at which a company neither makes a profit nor incurs a loss. Lowering the break-even point means reducing the amount of sales or production required to cover all costs.

Factors Affecting Break-Even Point:

There are several factors that can affect the break-even point, and these include both fixed costs and variable costs.

1. Fixed Costs:

- Fixed costs are expenses that do not change with the level of production or sales.

- Examples of fixed costs include rent, salaries, insurance, and depreciation.

- Increasing fixed costs would raise the break-even point because more sales or production would be required to cover these higher costs.

2. Variable Costs:

- Variable costs are expenses that change in proportion to the level of production or sales.

- Examples of variable costs include raw materials, direct labor, and utilities.

- Increasing variable costs would raise the break-even point because more sales or production would be required to cover these higher costs.

3. Slope of the Income Line:

- The slope of the income line represents the profit margin per unit of sales.

- A steeper slope indicates a higher profit margin, while a flatter slope indicates a lower profit margin.

- Decreasing the slope of the income line would lower the break-even point because it means that less sales or production would be required to achieve the same level of profit.

4. Reducing Variable Costs:

- Reducing variable costs would lower the break-even point because it means that less sales or production would be required to cover these lower costs.

- This can be achieved through various means such as negotiating better prices with suppliers, improving operational efficiency, or finding alternative raw materials.

Conclusion:

Out of the given options, reducing the variable cost (Option D) is the correct answer to lower the break-even point. By reducing variable costs, a company can achieve a lower break-even point, meaning that it would require fewer sales or production to cover its costs and start making a profit.

Attention Railways Students!

To make sure you are not studying endlessly, EduRev has designed Railways study material, with Structured Courses, Videos, & Test Series. Plus get personalized analysis, doubt solving and improvement plans to achieve a great score in Railways.

|

Explore Courses for Railways exam

|

|

Similar Railways Doubts

Top Courses for RailwaysView all

The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer?

Question Description

The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? for Railways 2024 is part of Railways preparation. The Question and answers have been prepared according to the Railways exam syllabus. Information about The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? covers all topics & solutions for Railways 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer?.

The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? for Railways 2024 is part of Railways preparation. The Question and answers have been prepared according to the Railways exam syllabus. Information about The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? covers all topics & solutions for Railways 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer?.

Solutions for The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? in English & in Hindi are available as part of our courses for Railways.

Download more important topics, notes, lectures and mock test series for Railways Exam by signing up for free.

Here you can find the meaning of The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? defined & explained in the simplest way possible. Besides giving the explanation of

The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer?, a detailed solution for The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? has been provided alongside types of The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? theory, EduRev gives you an

ample number of questions to practice The break-even point can be lowered bya)Increasing the fixed costsb)Increasing the variable costsc)Decreasing the slope of the income lined)Reducing the variable costCorrect answer is option 'D'. Can you explain this answer? tests, examples and also practice Railways tests.

|

|

Explore Courses for Railways exam

|

|

Suggested Free Tests

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

Follow Us

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup