Mechanical Engineering Exam > Mechanical Engineering Questions > The breakeven volume for a product can be red...

Start Learning for Free

The breakeven volume for a product can be reduced by

- a)increasing the fixed costs

- b)reducing its selling price

- c)reducing its unit cost

- d)increasing its unit cost

Correct answer is option 'C'. Can you explain this answer?

Verified Answer

The breakeven volume for a product can be reduced bya)increasing the f...

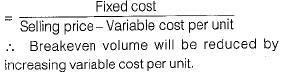

Breakeven volume

Most Upvoted Answer

The breakeven volume for a product can be reduced bya)increasing the f...

Explanation:

The breakeven volume for a product refers to the point at which the total revenue generated from sales is equal to the total costs incurred to produce and sell the product. It is the volume of sales required to cover all costs and achieve neither a profit nor a loss.

Reducing the unit cost of a product can help to reduce the breakeven volume. This means that for each unit sold, the cost of producing that unit is lower. By reducing the unit cost, the breakeven volume is reduced because fewer units need to be sold in order to cover the fixed costs and reach the breakeven point.

How reducing unit cost reduces breakeven volume:

- Definition of unit cost: The unit cost is the cost incurred to produce one unit of a product. It includes both variable costs (such as materials and labor) and a portion of the fixed costs (such as rent and utilities).

- Calculation of breakeven volume: The breakeven volume can be calculated by dividing the total fixed costs by the contribution margin per unit. The contribution margin per unit is the difference between the selling price per unit and the variable cost per unit.

- Effect of reducing unit cost: When the unit cost is reduced, the contribution margin per unit increases. This is because the selling price per unit remains the same, but the variable cost per unit decreases. As a result, the breakeven volume decreases because the contribution margin per unit is higher, meaning that fewer units need to be sold to cover the fixed costs.

- Example: Let's consider an example to illustrate this concept. Suppose a product has a selling price of $10 per unit, a variable cost of $5 per unit, and fixed costs of $10,000. The contribution margin per unit is $10 - $5 = $5. The breakeven volume is calculated as $10,000 / $5 = 2,000 units. Now, if the unit cost is reduced to $4 per unit, the contribution margin per unit increases to $10 - $4 = $6. The new breakeven volume is $10,000 / $6 ≈ 1,667 units. As we can see, reducing the unit cost has reduced the breakeven volume.

In conclusion, reducing the unit cost of a product can help to reduce the breakeven volume. This is because a lower unit cost increases the contribution margin per unit, resulting in a lower volume of sales required to cover the fixed costs and reach the breakeven point.

The breakeven volume for a product refers to the point at which the total revenue generated from sales is equal to the total costs incurred to produce and sell the product. It is the volume of sales required to cover all costs and achieve neither a profit nor a loss.

Reducing the unit cost of a product can help to reduce the breakeven volume. This means that for each unit sold, the cost of producing that unit is lower. By reducing the unit cost, the breakeven volume is reduced because fewer units need to be sold in order to cover the fixed costs and reach the breakeven point.

How reducing unit cost reduces breakeven volume:

- Definition of unit cost: The unit cost is the cost incurred to produce one unit of a product. It includes both variable costs (such as materials and labor) and a portion of the fixed costs (such as rent and utilities).

- Calculation of breakeven volume: The breakeven volume can be calculated by dividing the total fixed costs by the contribution margin per unit. The contribution margin per unit is the difference between the selling price per unit and the variable cost per unit.

- Effect of reducing unit cost: When the unit cost is reduced, the contribution margin per unit increases. This is because the selling price per unit remains the same, but the variable cost per unit decreases. As a result, the breakeven volume decreases because the contribution margin per unit is higher, meaning that fewer units need to be sold to cover the fixed costs.

- Example: Let's consider an example to illustrate this concept. Suppose a product has a selling price of $10 per unit, a variable cost of $5 per unit, and fixed costs of $10,000. The contribution margin per unit is $10 - $5 = $5. The breakeven volume is calculated as $10,000 / $5 = 2,000 units. Now, if the unit cost is reduced to $4 per unit, the contribution margin per unit increases to $10 - $4 = $6. The new breakeven volume is $10,000 / $6 ≈ 1,667 units. As we can see, reducing the unit cost has reduced the breakeven volume.

In conclusion, reducing the unit cost of a product can help to reduce the breakeven volume. This is because a lower unit cost increases the contribution margin per unit, resulting in a lower volume of sales required to cover the fixed costs and reach the breakeven point.

|

Explore Courses for Mechanical Engineering exam

|

|

Top Courses for Mechanical EngineeringView all

Question Description

The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? for Mechanical Engineering 2025 is part of Mechanical Engineering preparation. The Question and answers have been prepared according to the Mechanical Engineering exam syllabus. Information about The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? covers all topics & solutions for Mechanical Engineering 2025 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer?.

The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? for Mechanical Engineering 2025 is part of Mechanical Engineering preparation. The Question and answers have been prepared according to the Mechanical Engineering exam syllabus. Information about The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? covers all topics & solutions for Mechanical Engineering 2025 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer?.

Solutions for The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? in English & in Hindi are available as part of our courses for Mechanical Engineering.

Download more important topics, notes, lectures and mock test series for Mechanical Engineering Exam by signing up for free.

Here you can find the meaning of The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? defined & explained in the simplest way possible. Besides giving the explanation of

The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer?, a detailed solution for The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? has been provided alongside types of The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? theory, EduRev gives you an

ample number of questions to practice The breakeven volume for a product can be reduced bya)increasing the fixed costsb)reducing its selling pricec)reducing its unit costd)increasing its unit costCorrect answer is option 'C'. Can you explain this answer? tests, examples and also practice Mechanical Engineering tests.

|

|

Explore Courses for Mechanical Engineering exam

|

|

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup on EduRev and stay on top of your study goals

10M+ students crushing their study goals daily