B Com Exam > B Com Questions > A machine costing rupees 2,40,000 is deprecia...

Start Learning for Free

A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year

?

Most Upvoted Answer

A machine costing rupees 2,40,000 is depreciated at 18% per annum on r...

Community Answer

A machine costing rupees 2,40,000 is depreciated at 18% per annum on r...

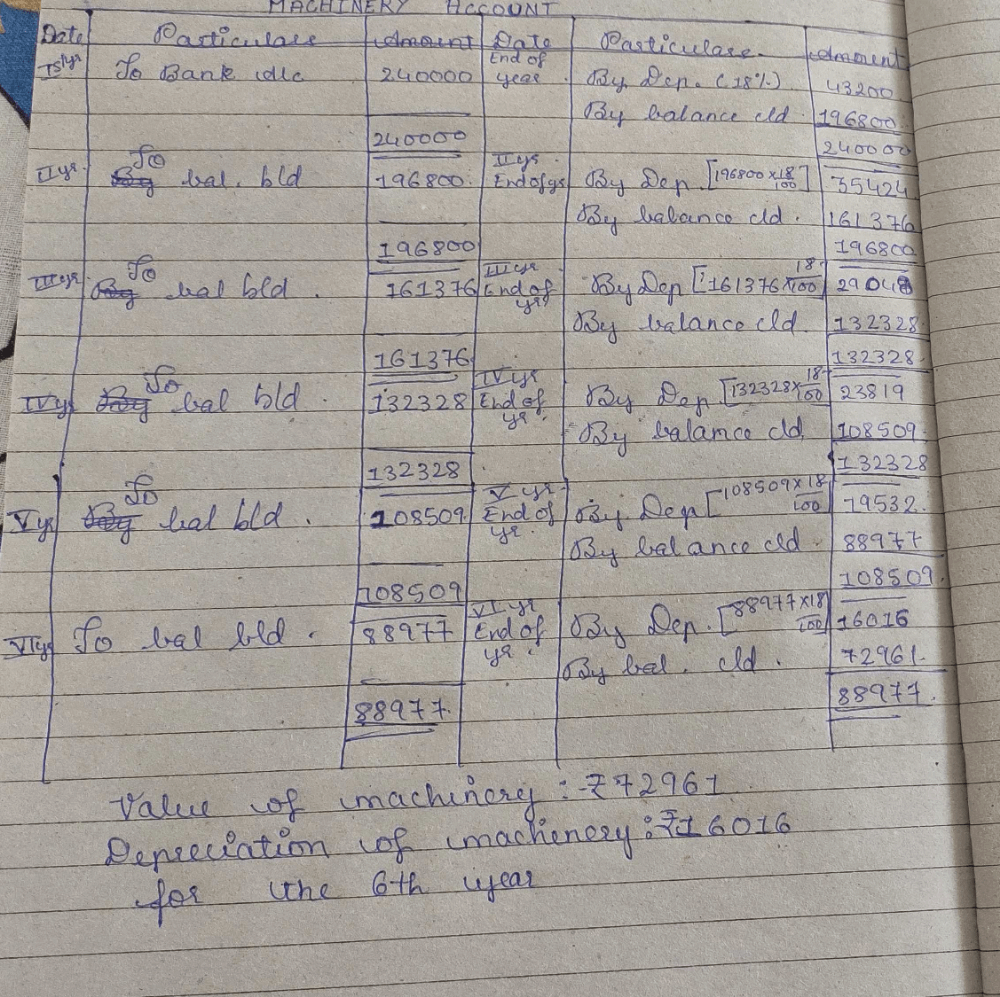

Given, cost of the machine = Rs. 2,40,000

Depreciation rate = 18% per annum

Using reducing balance method, the depreciation for each year will be calculated as follows:

Depreciation for the 1st year = 18% of 2,40,000 = Rs. 43,200

Value of the machine after 1st year = 2,40,000 - 43,200 = Rs. 1,96,800

Depreciation for the 2nd year = 18% of 1,96,800 = Rs. 35,424

Value of the machine after 2nd year = 1,96,800 - 35,424 = Rs. 1,61,376

Depreciation for the 3rd year = 18% of 1,61,376 = Rs. 29,048.64 (approx.)

Value of the machine after 3rd year = 1,61,376 - 29,048.64 = Rs. 1,32,327.36 (approx.)

Depreciation for the 4th year = 18% of 1,32,327.36 = Rs. 23,818.92 (approx.)

Value of the machine after 4th year = 1,32,327.36 - 23,818.92 = Rs. 1,08,508.44 (approx.)

Depreciation for the 5th year = 18% of 1,08,508.44 = Rs. 19,531.32 (approx.)

Value of the machine after 5th year = 1,08,508.44 - 19,531.32 = Rs. 88,977.12 (approx.)

Depreciation for the 6th year = 18% of 88,977.12 = Rs. 16,016.28 (approx.)

Value of the machine after 6th year = 88,977.12 - 16,016.28 = Rs. 72,960.84 (approx.)

Therefore, the value of the machine after 6 years is Rs. 72,960.84 (approx.) and the depreciation amount for the 6th year is Rs. 16,016.28 (approx.).

Depreciation rate = 18% per annum

Using reducing balance method, the depreciation for each year will be calculated as follows:

Depreciation for the 1st year = 18% of 2,40,000 = Rs. 43,200

Value of the machine after 1st year = 2,40,000 - 43,200 = Rs. 1,96,800

Depreciation for the 2nd year = 18% of 1,96,800 = Rs. 35,424

Value of the machine after 2nd year = 1,96,800 - 35,424 = Rs. 1,61,376

Depreciation for the 3rd year = 18% of 1,61,376 = Rs. 29,048.64 (approx.)

Value of the machine after 3rd year = 1,61,376 - 29,048.64 = Rs. 1,32,327.36 (approx.)

Depreciation for the 4th year = 18% of 1,32,327.36 = Rs. 23,818.92 (approx.)

Value of the machine after 4th year = 1,32,327.36 - 23,818.92 = Rs. 1,08,508.44 (approx.)

Depreciation for the 5th year = 18% of 1,08,508.44 = Rs. 19,531.32 (approx.)

Value of the machine after 5th year = 1,08,508.44 - 19,531.32 = Rs. 88,977.12 (approx.)

Depreciation for the 6th year = 18% of 88,977.12 = Rs. 16,016.28 (approx.)

Value of the machine after 6th year = 88,977.12 - 16,016.28 = Rs. 72,960.84 (approx.)

Therefore, the value of the machine after 6 years is Rs. 72,960.84 (approx.) and the depreciation amount for the 6th year is Rs. 16,016.28 (approx.).

|

Explore Courses for B Com exam

|

|

Similar B Com Doubts

A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics?

Question Description

A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6 years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? for B Com 2025 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6 years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? covers all topics & solutions for B Com 2025 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6 years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics?.

A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6 years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? for B Com 2025 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6 years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? covers all topics & solutions for B Com 2025 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6 years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics?.

Solutions for A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? in English & in Hindi are available as part of our courses for B Com.

Download more important topics, notes, lectures and mock test series for B Com Exam by signing up for free.

Here you can find the meaning of A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? defined & explained in the simplest way possible. Besides giving the explanation of

A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics?, a detailed solution for A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? has been provided alongside types of A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? theory, EduRev gives you an

ample number of questions to practice A machine costing rupees 2,40,000 is depreciated at 18% per annum on reducing balance method. Find the value of the machine after 6 years. Also find the value of the machine after 6

years. Also find the depreciation amount for the 6th year Related: Properties of Determinants - Matrices and Determinants, Business Mathematics & Statistics? tests, examples and also practice B Com tests.

|

|

Explore Courses for B Com exam

|

|

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup