CA Foundation Exam > CA Foundation Questions > If the covariance between two variable is 20 ...

Start Learning for Free

If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable

?

?

Verified Answer

If the covariance between two variable is 20 and the variance of one o...

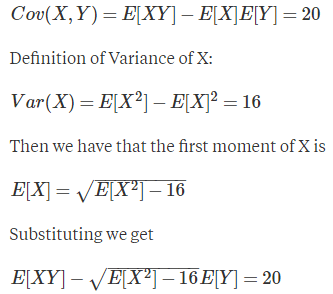

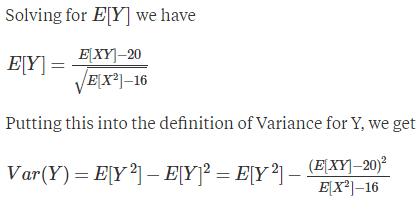

Definition of Covariance of X and Y:

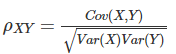

I’m not sure we have all of the quantities we need to get a number, but that’s what you get if you substitute what you know into the definitions.If we had the correlation coefficient between the variables X and Y, we could calculate the variance of the other variable, but without that information, I believe we’re left with three degrees of freedom, namely the product moment of X and Y and the second moments of both X and Y.Or, if you’re looking at it in terms of correlation, then the degree of freedom there is the correlation coefficient, defined bY

This question is part of UPSC exam. View all CA Foundation courses

This question is part of UPSC exam. View all CA Foundation courses

Most Upvoted Answer

If the covariance between two variable is 20 and the variance of one o...

Introduction:

To determine the variance of the other variable, we need to know the covariance between the two variables and the variance of one of the variables. Covariance measures the linear relationship between two variables, while variance measures the dispersion or spread of a single variable.

Given:

Covariance (X, Y) = 20

Variance (X) = 16

Relationship between Covariance and Variance:

The covariance between two variables, X and Y, can be calculated using the formula:

Cov(X, Y) = E[(X - μx)(Y - μy)]

Where Cov(X, Y) is the covariance, E is the expected value, X and Y are the variables, and μx and μy are the means of X and Y, respectively.

The variance of a variable, X, can be calculated using the formula:

Var(X) = E[(X - μx)²]

Where Var(X) is the variance, E is the expected value, X is the variable, and μx is the mean of X.

Calculating Variance of the Other Variable:

To find the variance of the other variable, let's denote it as Y. We can start by rearranging the covariance formula:

Cov(X, Y) = E[(X - μx)(Y - μy)]

Expanding the equation:

Cov(X, Y) = E[XY - Xμy - Yμx + μxμy]

Since E[XY] = μxμy as per the covariance formula, we can simplify the equation:

Cov(X, Y) = μxμy - μxμy - μxμy + μxμy

Cov(X, Y) = 0

Conclusion:

From the equation above, we can see that the covariance between X and Y is zero. This implies that there is no linear relationship between the two variables. Therefore, the variance of the other variable, Y, is independent of the variance of X. Given that the variance of X is 16, we cannot determine the variance of Y based on this information alone. Additional information or assumptions about the relationship between X and Y would be required to calculate the variance of Y.

To determine the variance of the other variable, we need to know the covariance between the two variables and the variance of one of the variables. Covariance measures the linear relationship between two variables, while variance measures the dispersion or spread of a single variable.

Given:

Covariance (X, Y) = 20

Variance (X) = 16

Relationship between Covariance and Variance:

The covariance between two variables, X and Y, can be calculated using the formula:

Cov(X, Y) = E[(X - μx)(Y - μy)]

Where Cov(X, Y) is the covariance, E is the expected value, X and Y are the variables, and μx and μy are the means of X and Y, respectively.

The variance of a variable, X, can be calculated using the formula:

Var(X) = E[(X - μx)²]

Where Var(X) is the variance, E is the expected value, X is the variable, and μx is the mean of X.

Calculating Variance of the Other Variable:

To find the variance of the other variable, let's denote it as Y. We can start by rearranging the covariance formula:

Cov(X, Y) = E[(X - μx)(Y - μy)]

Expanding the equation:

Cov(X, Y) = E[XY - Xμy - Yμx + μxμy]

Since E[XY] = μxμy as per the covariance formula, we can simplify the equation:

Cov(X, Y) = μxμy - μxμy - μxμy + μxμy

Cov(X, Y) = 0

Conclusion:

From the equation above, we can see that the covariance between X and Y is zero. This implies that there is no linear relationship between the two variables. Therefore, the variance of the other variable, Y, is independent of the variance of X. Given that the variance of X is 16, we cannot determine the variance of Y based on this information alone. Additional information or assumptions about the relationship between X and Y would be required to calculate the variance of Y.

Attention CA Foundation Students!

To make sure you are not studying endlessly, EduRev has designed CA Foundation study material, with Structured Courses, Videos, & Test Series. Plus get personalized analysis, doubt solving and improvement plans to achieve a great score in CA Foundation.

|

|

Explore Courses for CA Foundation exam

|

|

Similar CA Foundation Doubts

Top Courses for CA FoundationView all

If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ?

Question Description

If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? for CA Foundation 2024 is part of CA Foundation preparation. The Question and answers have been prepared according to the CA Foundation exam syllabus. Information about If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? covers all topics & solutions for CA Foundation 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ?.

If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? for CA Foundation 2024 is part of CA Foundation preparation. The Question and answers have been prepared according to the CA Foundation exam syllabus. Information about If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? covers all topics & solutions for CA Foundation 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ?.

Solutions for If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? in English & in Hindi are available as part of our courses for CA Foundation.

Download more important topics, notes, lectures and mock test series for CA Foundation Exam by signing up for free.

Here you can find the meaning of If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? defined & explained in the simplest way possible. Besides giving the explanation of

If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ?, a detailed solution for If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? has been provided alongside types of If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? theory, EduRev gives you an

ample number of questions to practice If the covariance between two variable is 20 and the variance of one of the variable is 16 , what would be the variance of the other variable ? tests, examples and also practice CA Foundation tests.

|

|

Explore Courses for CA Foundation exam

|

|

Suggested Free Tests

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup