Price Determination Class 12 Economics

Equilibrium Price

- It refers to a price where market demand is equal to market supply. In other words, there is no pressure on the price to either increase or decrease and this refers to the position of no price change.

- It is also called market price equilibrium quantity. It refers to the quantity demanded and supplied at an equilibrium price and this situation of zero excess demand and zero excess supply is called market equilibrium.

- Under perfect competition, the equilibrium price is determined by the intersection of market demand and the market supply curve.

- This free interplay of demand and supply is called the price mechanism or market mechanism.

Price Determination

Equality between Demand and Supply

- Price is determined between the two limits set by demand and supply.

- The equilibrium price is set where market demand is equal to market supply. In other words, there is no pressure on the price to either increase or decrease, which refers to a position of price change.

Adjustment Mechanism

Question: If for a given price there is excess supply, how will the equilibrium be reached? Use diagram.

Case A: Price Less Than Equilibrium Level or Situation of Excess Demand (Shortage of Supply) (M.D. > M.S)

Suppose the price is OP1 (Rs.30 ), there will be excess demand for ‘AB’ units (170-150 = 20 units).

- Situation: Excess demand is a situation when the quantity demanded is more than the quantity supplied at the prevailing market price.

- Cause: As the prevailing market price is less than the equilibrium price or the equilibrium price is more than the prevailing market price.

The buyers will be willing to buy more at a reduced price (acc. to LOD)

The seller would be selling lessat a reduced price (acc. to LOS)

Thus a situation will arise when Market demand will be greater than Market supply, known as excess demand. - Effect: This will

(i)result in competition among buyers, and some consumers will be unable to obtain the commodity

(ii) result in black marketing as some consumers will be willing to pay a high price - Mechanism: Accordingly, the price will start increasing up to the level where there is no excess demand, i.e, Q demanded is equal to Q supplied. This process is indicated by an arrow pointing upwards.Question for Chapter Notes - Price DeterminationTry yourself:If an increase in demand is greater than the increase in supply, then the equilibrium price?View Solution

Question:If, for a given price, there is excess demand, how will the equilibrium be reached ? Use diagram.

Case B: Price More Than Equilibrium Level or Situation Of Excess Supply (Shortage of Demand) (M.D. > M.S)

Suppose the price is OP2 (Rs.30 ), there will be excess demand of ‘CD’ units (170-150 = 20 units ).

- Situation: Excess supply is a situation when the quantity supplied is more than the quantity demandedat the prevailing market price.

- Cause: As the prevailing market price is more than the equilibrium price or the equilibrium price is less than the prevailing market price.

Buyers will be willing to buy less at a higher price (acc. to LOD)

The seller would be selling more at a higher price (acc. to LOS)

Thus a situation will arise when market Supply will be greater than Market Demand, known as excess supply. - Effect:

(i) Thus, competition among sellers will start, and some firms will not be able to sell the desired quantity

(ii) This will result in Stock Accumulation or Stock Piling - Mechanism: Accordingly, the price will start decreasing up to the level where there is no excess demand i.e. Q demanded is equal to Q supplied. This process is indicated by an arrow pointing downwards.

Numerical Solution

At equilibrium level

Qd = Qs

i.e. 200 - P = 120 +P

200 - 120 = P + P

80 = 2P

P = Rs 40

Putting the value of Price in Qd or Qs, we get, 200 - 40 or 120 + 40 = 160 units

Try Yourself

Question: “When the market is not in equilibrium, there will be a tendency of price to change” Justify.

Question:Which of these, demand or supply, is more important in the determination of price?

According to Marshall, both are equally helpful in the determination of price. He has given equal importance to both of them and has quoted that “as we need an upper blade and lower blade to cut cloth, as we require left and right leg to walk, similarlywe require both demand and supply to determine the price.”

But however, under exceptional situations, the importance may vary depending upon

(a) Time Period

(b)Type of Goods

- In case of a very short period, the supply of perishable goods (milk, vegetables) is fixed (inelastic). Therefore, demand has more influenceon the determination of price.

- In case of a long period, the supply of desirable goods can be stored, and hence the supply of goods is elastic. Moreover, the sellers have a reserve price below which they are not prepared to sell the commodity. Therefore, in this case, supply has more influence in the determination of price.

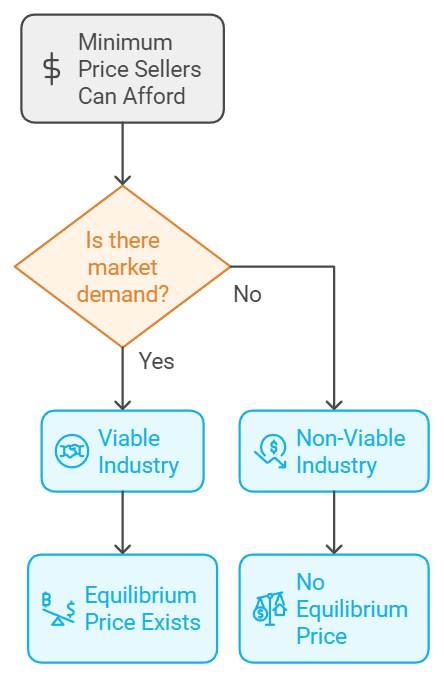

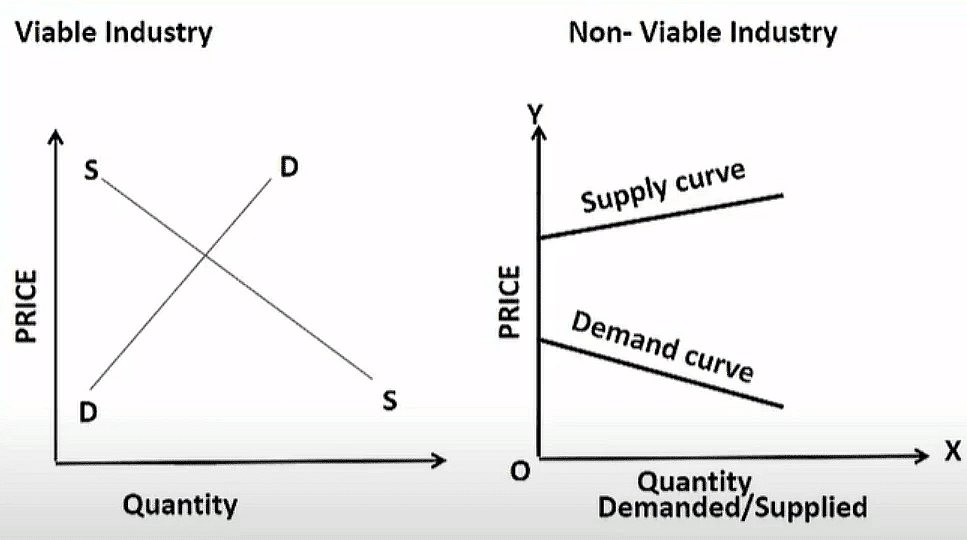

Viable Industry

An industry is said to be viable when for a minimum price that sellers can afford, there is demand in the market. Thus there is an equilibrium price, and graphically, demand and supply intersect at some common point.

Non-Viable Industry

An industry is said to be non-viable when for a minimum price that the seller can afford, there is no demand in the market. Graphically supply curve is above the demand curve, and both do not intersect i.e, no equilibrium price exists.

Examples

(a) aircraft industry in India as COP is very high so govt. Purchases it from Germany or France where it is a viable produce

(b) Robotics industry, Computer Memory Chips

Effect on Equilibrium Price / Market Price and Quantity

Change in Demand

Supply Unchanged or Supply Remaining Constant

Change in Supply

Demand Unchanged or Demand Remaining Constant

Numerical Solution

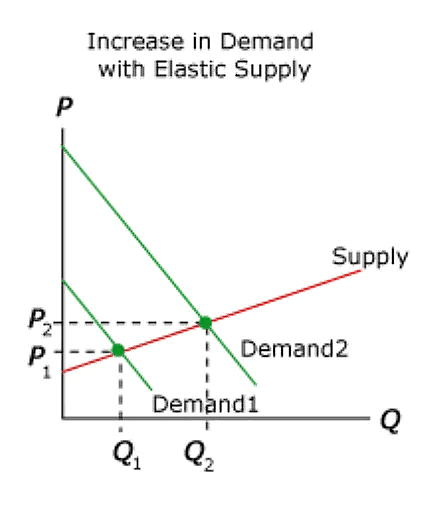

(Case 1) Increase in Demand (Rightward Shift)

Qd = 200 - P + 40

Qs = 120 +P

At equilibrium

Qd = Qs

200 - P + 40 = 120 +P

240 - P = 120 + P

120 = 2P

P = Rs 60 (increases)

Qd = Qs = 180 units (increases)

(Case2) Decrease in Demand (Leftward Shift)

Qd = 200 - P - 40

Qs = 120 +P

At equilibrium Qd = Qs

200 - P - 40 = 120 +P

160 - P = 120 + P

40 = 2P

P = Rs 20 (decreases)

Qd = Qs = 140 units (decreases)

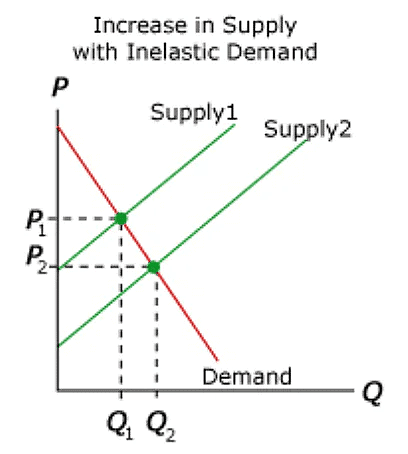

(Case 3) Increase in Supply (Rightward Shift)

Qd = 200 - P

Qs = 120 +P + 40

At equilibrium Qd = Qs

200 - P = 120 + P + 40

200 - P = 160 + P

40 = 2P

P = Rs 20 (decreases)

Qd = Qs = 180 units (increases)

(Case 4) Decrease in Supply (Leftward Shift)

Qd = 200 - P

Qs = 120 +P -40

At equilibrium Qd = Qs

200 - P = 120 + P - 40

200 - P = 80 + P

120 = 2P

P = Rs 60 (increases)

Qd = Qs = 140 units (decreases)

Exceptional or Miscellaneous Cases

(A) Demand Is Perfectly Elastic and Supply Changes

(B) Demand Is Perfectly Inelastic and Supply Changes

(C) Supply Is Perfectly Elastic and Demand Changes

(D)Supply Is Perfectly Inelastic and Demand Changes

Simultaneous Change in Demand and Supply

Question: “Change in demand and supply may or may not affect Price”

Question: “Change in demand and supply may increase, may decrease, or may not affect Price”

The statement is true as a change in price depends upon the proportion change in demand and the proportion change in supply

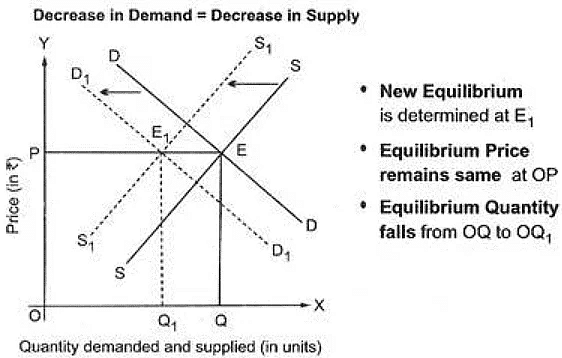

- Simultaneous Increases in Demand and Supply: This will result in an increase in equilibrium quantity always, and the change in equilibrium price will depend upon whether demand increases more than, equal to, or less than supply.

1. When a Proportionate Increase In Demand Is More Than a Proportionate Increase In Supply:

Price will rise, and quantity will rise

2. When Proportionate Increase In Demand Is Less Than Proportionate Increase In Supply:

Price will fall, and quantity will rise

3. When Proportionate Increase In Demand Is Equal To Than Proportionate Increase In Supply:

Price remains unchanged, and quantity will rise

- Simultaneous Decreases in Demand and Supply: This will result in a decrease in equilibrium quantity always, and the change in equilibrium price will depend upon whether demand decreases more than, equal to, or less than supply.

1. When a Proportionate Decrease In Demand Is More Than a Proportionate Decrease In Supply:

Price will fall, and quantity will fall

2. When a Proportionate Decrease In Demand Is Less Than a Proportionate Decrease In Supply:

Price will rise, and quantity will fall

3. When Proportionate Decrease In Demand Is Equal To Than Proportion Decrease In Supply:

Price remains unchanged, and quantity will fall

- Demand and Supply Shifts In Opposite Directions

- Demand Increases and Supply Decreases: This situation will result in excess demand, and hence there will be a price increase.

- Demand Decreases and Supply Increases: This situation will result in excess supply, and hence there will be a price decrease.

Increase or decrease in quantity depends upon proportionate change in demand and supply.

Various Cases Where Equilibrium Price Remains Same

(a) Proportionate Increase in Demand = Proportionate Increase in Supply

(b) Proportionate Decrease in Demand = Proportionate decrease in Supply

(c) Demand increases, and Supply is Perfectly elastic

(d) Demand decreases, and Supply is Perfectly elastic

(e) Supply Increases and Demand is perfectly elastic

(f) Supply Decreases and Demand is perfectly elastic

Application of Demand and Supply Analysis

Example of Imbalance between Demand and Supply

- In 1998 Indian economy suffered the ‘ onion crisis.’ The price of onion increased from Rs 5 per kilogram to Rs 60 per kilogram in the retail market.

- In 1978, the was a bumper crop of sugarcane in India, and the price of sugarcane crashed to Rs. 5 per quintal. The farm producers had to suffer huge losses. The same happened in 2001 in the case of the potato market. In these cases of excess supply, sellers stand to lose

Government Intervention in Markets: When the two sets of agents -buyers and sellers, fail to restore equilibrium in the commodity market, there is a need for the third agent, i.e. government, to resolve the problem. The government may be in the form of CG / SG, Central Authorities, Public Agencies, Public Bodies, Local Governments, etc.

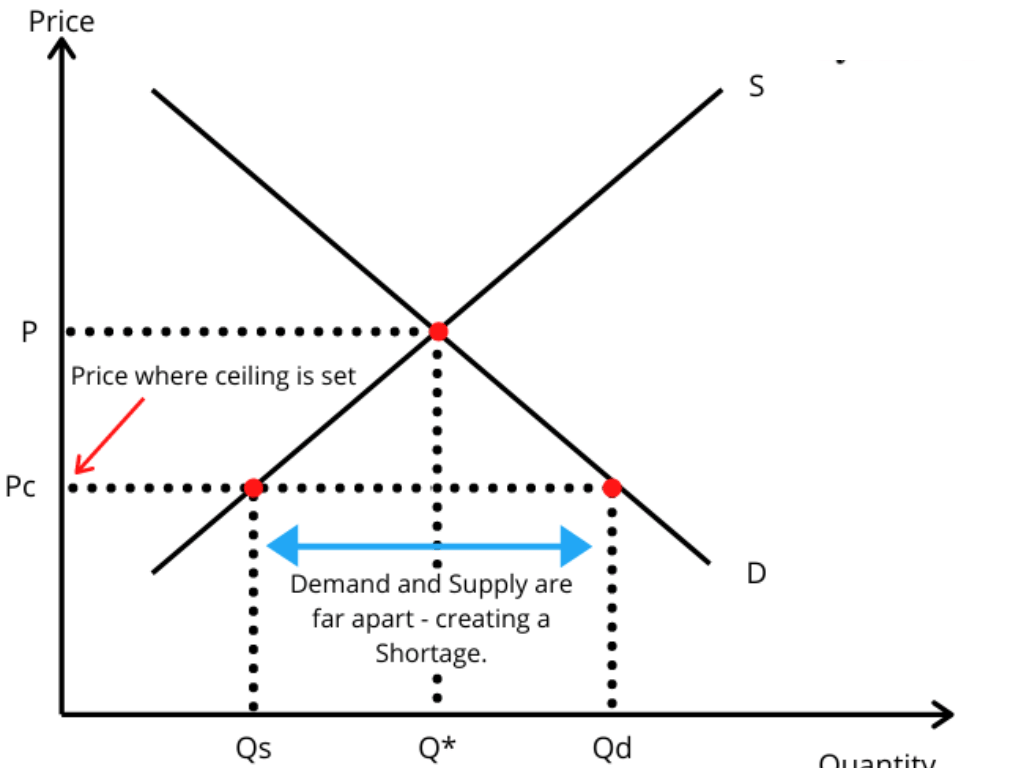

Price Control / Ceiling Price or Maximum Price Legislation

Meaning: Price control means that an upper limit (maximum price) has been imposed on the price of a good or service Producers of these commodities cannot charge a price higher than the ceiling price (i.e., the maximum price) fixed by the Government. Govt. fixes this price below the equilibrium market price of a commodity so that it becomes within the reach of the poorer sections of society.

Examples: The Government of India has imposed Price controls on a number of commodities, e.g., fertilizers, Petroleum products, LPG, life-saving drugs, essential commodities like sugar, wheat, rice, kerosene, etc.

Application of Price Control / Ceiling Price

Rent Control: The Imbalance between demand for and supply of housing accommodation causes an increase in rents.

The government passed the ‘Rent Control Act, which imposes a maximum limit on rent, i.e., landlords cannot charge a rent more than what is fixed by the government.

In Fig DD and SS are the original demand and supply curves, respectively, for a commodity. E is the equilibrium point, corresponding to which OQ quantity is being demanded and supplied at the price OP per unit. Suppose the Government decides to interfere with the free operation of the market forces and imposes a price ceiling at Pc, which lowers the equilibrium price level.

At the lower price quantity demanded will expand to Pc A, but suppliers will be ready to supply only Pc B quantity of goods. As a result, there will be excess demand or shortage of this commodity (equal to quantity demanded minus quantity supplied ).

This is represented by the line segment “AB”.

Consequences of Price Controls or Price Ceiling

- Shortage or Excess Demand: The quantity actually sold and bought in the market will reduce, and as a result, a large portion of consumers’ demand will be unsatisfied.

- Rationing: To ensure the availability of goods to everyone, governments generally have price controls with distribution controls. The most effective form of distribution control is rationing. Rationing implies that a ceiling(maximum amount) is imposed on the quantity that can be bought and consumed by a consumer.

This is done by giving ration coupons to the consumer so that no individual can buy more than a certain amount of controlled goods. - Queue System: The controlled goods are sold through ration shops which are also called fair price shops, and these are distributed on the basis of first-come-first-served. This situation results in the formation of long queues at the ration shop.

- Black Marketing: Black marketing is a direct consequence of price controls. Black marketing implies a situation in which the controlled commodity is sold unlawfully at a price higher than the lawfully enforced ceiling price. This situation arises largely because of the fact that:

(i) The number of potential consumers of the commodity is more than the available supplies of the commodity.

(ii) Some consumers are willing to pay more than the ceiling price.

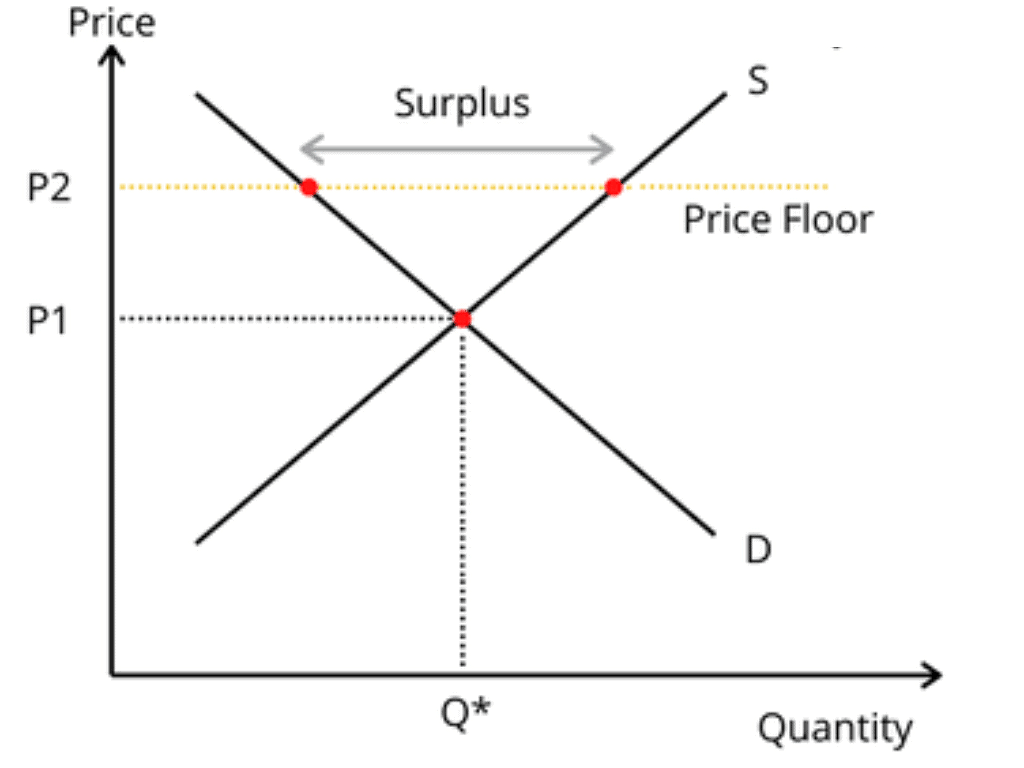

Floor Price or Price Support or Minimum Price Legislation

Meaning: Price support means a lower limit (minimum price) has been laid on the prices of some commodities. The floor price is a legal limit on the minimum price that the supplier may charge for a particular good or service. It benefits the suppliers of goods or services.

Example: The government of India fixes the minimum price of agricultural goods so that farmers are assured of some minimum income from their produce.

Application of Minimum Wage Legislation: Minimum wages are to be paid to the labour in factories or industrial establishments so that employers may be prohibited from paying less than the minimum wage fixed by the government.

The government decides to interfere with the free operation of the market forces and imposes a price floor at PF which is higher than the equilibrium price level.

At the higher price quantity demanded will contract to PFC, but suppliers will be ready to supply more PFD quantity of goods.

As a result, there will be excess supply or shortage of the commodity. This is represented by the line segment “CD”.

Consequences of Price Support (Above Equilibrium Price)

- Surpluses: The quantity actually bought and supplied will reduce as a direct consequence of price support, and as a result, a large proportion of the producer’s stocks will remain unutilized.

- Buffer Stocks: To maintain the support price, the Government would have to design some such programs like the government purchasing the surplus stocks available with the produces and stocking them for emergencies. The buffer stock operations benefit the producers as a group, but it has a negative impact on

(a) Consumers who have to pay higher prices for the product

(b) the people in general who have to pay taxes to support this program. - Subsidies: To offset the loss to the consumers, the government may undertake subsidies on the product. By subsidy, we mean that the government purchases the product at the support price and sells the product to consumers below its cost of procurement. The difference between cost and price is borne but the government.

Excess demand is a situation when the quantity demanded is more than the quantity supplied at the prevailing market price.

|

1365 videos|1312 docs|1010 tests

|

FAQs on Price Determination Class 12 Economics

| 1. What is equilibrium price and how is it determined? |  |

| 2. What factors can cause shifts in demand and supply that affect equilibrium price? | |

| 3. How does a surplus affect the equilibrium price? | |

| 4. How does a shortage impact the equilibrium price? | |

| 5. Can government interventions affect market equilibrium price? | |

|

6.7K Views |

|

4.60/5 Rating |

|

Dec 02, 2024 Last updated |

|

1365 videos|1312 docs|1010 tests

|

|

Explore Courses for SSC CGL exam

|

|

Sample Paper

,Important questions

,practice quizzes

,Price Determination Class 12 Economics

,Previous Year Questions with Solutions

,Summary

,shortcuts and tricks

,Price Determination Class 12 Economics

,Free

,Semester Notes

,past year papers

,Extra Questions

,video lectures

,MCQs

,Exam

,ppt

,Viva Questions

,mock tests for examination

,Price Determination Class 12 Economics

,Objective type Questions

,study material

;

Chapter Notes - Price Determination Free PDF Download

Importance of Chapter Notes - Price Determination

Chapter Notes - Price Determination

Chapter Notes - Price Determination SSC CGL Questions

Study Chapter Notes - Price Determination on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|