Chapter Notes- Unit 2: Basic Problems of an Economy & Role of Price Mechanism

Basic Problems of an Economy

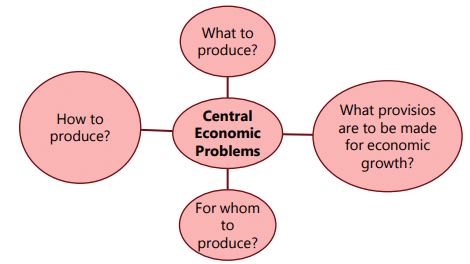

As discussed in the previous unit, all nations, without exception, encounter the issue of scarcity. Their resources-such as natural productive resources, man-made capital goods, consumer goods, money, and time-are finite, and these resources have alternative applications. For instance, coal can serve multiple purposes: it can be utilized as fuel for industrial production, for generating electricity, or for domestic cooking, among other uses. Likewise, financial resources can be allocated to various needs. If resources were unlimited, individuals would meet all their desires, eliminating any economic issues. Conversely, if a resource had only one application, the economic problem would not exist either.Every economic system, whether capitalist, socialist, or mixed, must confront this fundamental issue of resource scarcity in relation to the demands for them. This is commonly referred to as 'the central economic problem'. The central economic problem can be further categorized into four primary economic questions:

- What to produce?

- How to produce?

- For whom to produce?

- What measures (if any) should be taken for economic growth?

(i) What to produce?: Given limited resources, every society must determine which goods and services to produce and in what quantities. An economy must decide between producing more guns or butter, or whether to focus on capital goods like machinery and dams versus consumer goods like cell phones. Essentially, a society needs to establish how much wheat, hospitals, schools, machines, and meters of cloth should be produced.

(ii) How to produce?: There are various methods to produce a commodity. For instance, cotton cloth can be made using handlooms, power looms, or automatic looms. Handloom production is more labor-intensive, while automatic looms require more capital. A society must choose between labor-intensive and capital-intensive techniques based on the availability and cost of production factors. The goal is to utilize production methods that optimize the use of available resources.

(iii) For whom to produce?: A critical decision for any society is determining for whom to produce goods and services. Since not all wants can be satisfied, a society must decide how to distribute the total output among its members, essentially determining the shares of different individuals in the collective production of goods and services.

(iv) What provision should be made for economic growth?: Societies must not allocate all resources solely for current consumption. Failing to do so risks stagnating production capacity, which could lead to a decline in living standards. Therefore, decisions must be made regarding the amount of savings and investments necessary for future progress.

An economic system refers to the complete arrangement for the production and distribution of goods and services within a society. It encompasses all mechanisms that facilitate economic choices, involving various individuals and economic institutions.

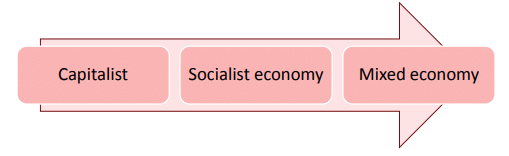

The world's economies tackle these central problems differently, and they can be broadly classified into three categories based on their production, exchange, distribution methods, and the role of government in economic activities.

Capitalist Economy

Capitalism is the primary economic system in today's global economy, characterized by private individuals owning and controlling all means of production for profit. In essence, private property is central to capitalism, and the profit motive drives economic activity. Consumer and business decisions dictate economic dynamics, and ideally, the government's role in economic management is minimal. Examples of capitalist economies include the United States, United Kingdom, Hong Kong, and South Korea, although many exhibit mixed traits rather than pure capitalism.

An economy is termed capitalist, free market, or laissez-faire if it possesses the following features:

- Right to Private Property: This allows individuals to own productive resources such as land, factories, and machinery, with the autonomy to utilize and transfer these assets, albeit with some societal restrictions imposed by the government.

- Freedom of Enterprise: Individuals are free to participate in any economic activity, enabling producers to establish firms and create goods and services of their choice.

- Freedom of Economic Choice: All individuals have the liberty to make their own economic decisions regarding consumption, work, production, and exchange.

- Profit Motive: The pursuit of profit is the fundamental driving force in a free enterprise economy, incentivizing entrepreneurs to organize production effectively to maximize profits.

- Consumer Sovereignty: In capitalism, consumers hold significant power, determining which goods and services are produced and in what amounts based on their preferences. Their purchasing decisions influence the allocation of the economy's limited resources.

- Competition: Competition is vital in a capitalist economy, fostering efficiency among buyers and sellers and optimizing resource use.

- Absence of Government Interference: A purely capitalist economy operates without central planning or regulation by the government, with economic activities guided by self-interest and the price mechanism functioning autonomously.

How do capitalist economies solve their central problems?

A capitalist economy operates without a central planning authority to determine what, how, and for whom to produce. This absence of central control might seem chaotic, especially if consumers prefer cars, producers focus on cloth, and workers choose the furniture sector. However, this chaos does not manifest in a capitalist economy. Instead, it utilizes the impersonal forces of market demand and supply, or the price mechanism, to address its central issues.

Deciding 'what to produce': Entrepreneurs aim to maximize profits, prompting competition among businesses to create the goods consumers desire. For instance, if there is a higher demand for cars, their prices will rise. An increase in car prices, assuming costs remain stable, will lead to higher profits, incentivizing producers to manufacture more cars. Conversely, if demand for cloth decreases, its price will drop, reducing profits and thereby discouraging production of cloth. This results in an increased production of cars and decreased production of cloth. In capitalist economies (like the USA, UK, and Germany), the decision regarding what to produce is ultimately governed by consumer preferences, reflected through their spending on desired goods.

Deciding 'how to produce': Entrepreneurs select production techniques that minimize costs. If labor is inexpensive, a labor-intensive method will be adopted; if labor is costly, a capital-intensive method will be chosen. Thus, the relative costs of production factors influence the decision on how to produce.

Deciding 'for whom to produce': Goods and services are produced for those with purchasing power. An individual's buying capacity is determined by their income, which is influenced by their work effort, the value of the factors they own, and their property ownership. Higher income results in greater buying capacity and increased demand for goods.

Deciding about consumption, saving, and investment: Consumption and savings are determined by consumers, while investments are made by entrepreneurs. Consumers' savings are affected by the prevailing interest rate; higher income and interest rates lead to increased savings. Investment decisions are based on expected returns; the higher the anticipated profit (i.e., return on capital), the more investment occurs in a capitalist economy. The interest rate on savings and the return rate on capital serve as the pricing mechanism for capital.

In summary, the production of goods, the methods employed, the target consumers, and considerations for economic growth are all determined by the price mechanism or market mechanism.

Merits of Capitalist Economy

- Capitalism operates on its own through the price mechanism, eliminating the need for expenses related to gathering and processing information or for formulating, implementing, and monitoring policies.

- The presence of private property and the profit motive lead to increased efficiency and motivation to work.

- Economic growth tends to occur more rapidly in a capitalist system, as investors focus on projects that are financially viable.

- Resources are allocated to the most productive activities, resulting in the optimal use of the economy's available productive resources.

- There is typically a high level of operational efficiency in capitalism.

- Production costs are reduced as producers aim to maximize profits by utilizing cost-effective production methods.

- The capitalist system provides incentives for sound economic decision-making and implementation.

- Consumers benefit from competition, which compels producers to offer a wide range of high-quality products at reasonable prices. This, combined with consumer choice, leads to maximum satisfaction and improved living standards.

- Capitalism encourages innovation and technological advancements, benefiting the country through the development of business skills and research.

- Capitalism upholds fundamental rights, including the right to freedom and private property, allowing participants to enjoy significant autonomy and freedom.

- It rewards initiative and enterprise while penalizing those who are imprudent or inefficient.

- Capitalism generally operates within a democratic framework.

- This system fosters entrepreneurship and risk-taking, leading to the emergence of a class of entrepreneurs willing to take risks.

Demerits of Capitalism

- There is significant economic inequality and social injustice in capitalism. Inequalities diminish the overall economic welfare of society and divide it into two classes: the 'haves' and the 'have-nots', fostering social unrest and class conflict.

- In capitalism, property rights take precedence over human rights.

- Economic inequalities result in substantial differences in economic opportunities and perpetuate societal unfairness.

- The capitalist system overlooks human welfare, prioritizing profit over the well-being of individuals.

- Income inequality distorts demand patterns, failing to reflect the true needs of society.

- Labor exploitation is prevalent in capitalism, often leading to strikes and lockouts. Additionally, there is a lack of job security, leaving workers more vulnerable.

- Consumer sovereignty is a myth, as consumers frequently fall victim to exploitation. Intense competition and profit motives can undermine consumer welfare.

- Resource allocation is inefficient, with resources diverted towards luxury goods. Consequently, fewer wage goods are produced due to their lower profitability.

- Merit goods like education and healthcare are also underproduced, while harmful goods that are more profitable may be produced excessively.

- Unplanned production leads to economic instability, characterized by overproduction, economic depression, and unemployment, causing significant human suffering.

- There is a considerable waste of productive resources, as firms invest heavily in advertising and sales promotion.

- Capitalism can foster monopolies, as larger firms may eliminate smaller competitors through various means.

- Furthermore, excessive materialism and conspicuous, unethical consumption contribute to environmental degradation.

Socialist Economy

The concept of a socialist economy was introduced by Karl Marx and Frederic Engels in their 1848 work, The Communist Manifesto. In this economic system, the material means of production-such as factories, capital, and mines-are owned collectively by the community, represented by the State. All individuals have the right to benefit from the outcomes of this socialized planned production based on equal rights. A socialist economy is also referred to as a "Command Economy" or a "Centrally Planned Economy," where resources are allocated according to the directives of a central planning authority, rendering market forces ineffective in resource allocation. The primary aim of production and distribution of goods in a socialist economy is to maximize the welfare of the community as a whole. Consequently, the central economic issues are addressed through planning within this framework.

Key Characteristics of a Socialist Economy:

- Collective Ownership: All means of production are collectively owned, with exceptions for small farms, workshops, and trading firms that may remain privately owned. Social ownership eliminates profit motives and self-interest as primary drivers of economic activity, focusing instead on achieving specific socio-economic objectives.

- Economic Planning: A Central Planning Authority is responsible for establishing and achieving socio-economic goals, hence the term "centrally planned economy." This authority makes major economic decisions, such as what to produce, when, and in what quantities.

- Absence of Consumer Choice: While freedom from hunger is assured, consumer sovereignty is limited by selective production. The variety of goods available is restricted by planned production, although individuals can choose from the options provided. The right to work exists, but occupational choices are determined by the central planning authority based on specific socio-economic objectives.

- Relatively Equal Income Distribution: A notable characteristic of socialism is the relative equality of income. Income and wealth disparities are reduced due to limited opportunities for private capital accumulation. Educational and other resources are distributed more equally, addressing the root causes of inequality.

- Minimum Role of Price Mechanism or Market Forces: While a price mechanism exists, it plays a secondary role, primarily for managing accumulated stocks. Resource allocation follows a predetermined plan, diminishing the influence of the price mechanism on economic decisions. Prices in a socialist economy are "administered prices," set by the central authority based on socio-economic goals.

- Absence of Competition: The state acts as the sole entrepreneur, resulting in a lack of competition.

The former U.S.S.R. exemplified a socialist economy from 1917 to 1990. Currently, no country operates purely as a socialist state, though examples include Vietnam, China, and Cuba. North Korea is also recognized as a socialist economy and is considered the most totalitarian state in the world.

Merits of Socialism

- The fair distribution of wealth and income, along with equal opportunities for everyone, promotes economic and social justice.

- In a socialist economy, rapid and balanced economic development is feasible as the central planning authority efficiently coordinates all resources according to established priorities.

- A socialist economy operates as a planned economy, leading to better resource utilization and maximum production. Economic planning minimizes all types of waste. With the absence of competition, there is no resource wastage on advertising and sales promotions.

- In a planned economy, unemployment is reduced, business cycles are stabilized, and economic stability is established and maintained.

- The lack of a profit motive fosters a cooperative mindset within the community and mitigates class conflict. Coupled with equality, this promotes the overall welfare of society.

- Socialism guarantees the right to work and a minimum standard of living for all individuals.

- Under socialism, workers and consumers receive protection from exploitation by employers and monopolistic practices, respectively.

- Socialism provides comprehensive social security, which gives citizens a sense of security.

Demerits of Socialism

- Socialism is characterized by a dominance of bureaucracy, leading to inefficiency and delays. It is also associated with issues like corruption, red tape, and favoritism.

- This system limits individual freedoms due to state ownership of the means of production and comprehensive state control over economic activities.

- Basic rights, including the right to private property, are compromised under socialism.

- It fails to offer necessary incentives for hard work through profit motives.

- Prices are not set by market forces based on buyer-seller negotiations, which disrupts cost calculation. This lack of practice hinders optimal resource allocation and the efficient operation of the economic system.

- State monopolies formed under socialism may become unmanageable and harder to regulate than private monopolies in capitalism.

- In a socialist framework, consumer choice is limited, meaning consumers must accept what the state produces.

- Personal efficiency and productivity are undervalued, and laborers are not compensated based on their effectiveness, serving as a disincentive to work.

- The extreme form of socialism is not feasible.

The Mixed Economy

The mixed economic system relies on both markets and governments for resource allocation. In reality, all economies utilize both markets and governments, making them inherently mixed economies. The goal of a mixed economy is to create a system that incorporates the best elements of both controlled and market economies while minimizing their drawbacks. It values the benefits of private enterprise and property, emphasizing self-interest and profit motives. The significant economic development in countries like England and the USA can be attributed to private enterprise. However, the interests of private property, profit, and self-interest may not always align with the community's well-being, necessitating government intervention to address these issues. Therefore, the government must oversee essential industries and mitigate the free rein of profit motives and self-interest, while still allowing private enterprise to positively contribute. The state enforces necessary regulations to ensure that the private sector aligns with national welfare objectives.

Features of Mixed Economy

- Co-existence of private and public sector:The primary feature of a mixed economy is the simultaneous existence of both private and public enterprises. There are three industrial sectors in a mixed economy:

- Private sector: Managed by private individuals and groups, focusing on self-interest and profit motives. This sector operates under a system of private property and allows for personal initiative, although government regulation may apply.

- Public sector: Established by the State for community welfare, rather than profit.

- Combined sector: A sector where both government and private enterprises collaborate to produce goods and services, leading to joint ventures.

Merits of Mixed Economy

- Economic freedom and the presence of private property, ensuring incentives to work.

- Price mechanisms and competition drive the private sector towards efficient decision-making and resource allocation.

- Consumers benefit from consumer sovereignty and freedom of choice.

- Incentives for innovation and technological advancements.

- Encouragement of enterprise and risk-taking.

- Advantages of economic planning and rapid development based on prioritized plans.

- Greater economic and social equality and reduced exploitation due to increased state involvement in economic activities.

- Government legislative measures help prevent excessive competition and its negative effects.

However, a mixed economy is not always a perfect compromise between capitalism and socialism; it can also face significant uncertainties.

Demerits of Mixed Economy

- Excessive government controls can lead to diminished incentives, stunted private sector growth, poor planning implementation, high taxes, inefficiency, corruption, resource wastage, delays in economic decisions, and underperformance of the public sector.

- Maintaining a balance between the public and private sectors is challenging.

- Without strong government initiatives, the private sector may disproportionately expand, resulting in a system akin to capitalism with its inherent disadvantages.

FAQs on Chapter Notes- Unit 2: Basic Problems of an Economy & Role of Price Mechanism

| 1. What are the basic problems faced by an economy? |  |

| 2. How does a capitalist economy address economic problems? | |

| 3. What are the key features of a socialist economy? | |

| 4. What is a mixed economy and how does it function? | |

| 5. What role does the price mechanism play in an economy? | |