Worksheet: Accounting for Not-for-Profit Organizations | Accountancy Class 12 - Commerce PDF Download

Q1: Differentiate between ‘Receipts and Payments Account’ and ‘Income and Expenditure Account’ on the basis of ‘Period’.

Q2: What is meant by ‘Life membership fees’?

Q3: State the main aim of a not-for-profit organisation.

Q4: How is the life membership fee treated while preparing the financial statements of a not-for-profit organisation?

Q5: How are specific donations treated while preparing final accounts of a ‘Not-for-Profit Organisation’?

Q6: State the basis of accounting of preparing the ‘Income and Expenditure Account’ of a ‘Not-for-Profit Organisation’.

Q7: Not-for-profit organisations have some distinguishing features from that of profit organisations. State any one of them.

Q8: Give two main sources of income of not-for-profit organisations.

Q9: Name any two financial statements required to be prepared by not-for-profit organisations at the end of the year.

Q10: Unrestricted funds raised by non-profit organisations through various sources are credited to which account?

Q11: What is the capital of a non-profit organisation generally known as?

Q12: From the following information, calculate the amount of subscriptions received by Happy Sports Club during the year ended 31st March, 2018.

The Club has 2,000 members each paying an annual subscription of Rs 500.

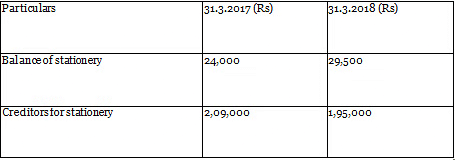

Q13: Calculate the amount of stationery to be debited to the ‘Income and Expenditure Account’ of New Friends Club for the year ended 31st March, 2018. Also present the relevant information in the Balance Sheet of the Club as of 31st March, 2018.

During the year Rs 46,000 were paid to the creditors for stationery and stationery of Rs 6,000 was purchased in cash.

Q14: From the following information, calculate the amount of ‘Sports Material’ to be debited to Income and Expenditure Account of Young Football Club for the year ended 31st March, 2018.

During the year, the creditors for sports materials were paid ₹ 1,10,000.

Q15: From the following information, calculate the amount of sports material consumed by Durga Sports Club for the year ended 31st March, 2018.

During the year, sports material purchased was ₹ 4,94,000.

Q16: From the following information, calculate the amount of stationery consumed by Shree Club for the year ended 31st March, 2018.

During the year, creditors were paid ₹ 3,00,000.

Q17: From the following information, calculate the amount of medicines to be debited to the ‘Income and Expenditure Account’ of a Charitable Hospital for the year ended 31st March, 2018. Also, present the relevant information in the Balance Sheet of the hospital; as at 31st March, 2018.

Cash paid to the creditors of medicines during the year was ₹ 25,00,000.

Q18: Janta Kalayan Club has 1,250 members each paying an annual subscription of? 150. During the year ending 31st March, 2018 the club did not receive subscriptions from 45 members and received subscriptions in advance from 46 members for the year ending 31st March, 2019. On 31st March, 2017 the outstanding subscriptions were ₹ 15,000 and subscriptions received in advance were ₹ 3,000.

Calculate the amount of subscription that will be debited to the Receipts and Payments Account for the year ended 31st March, 2018.

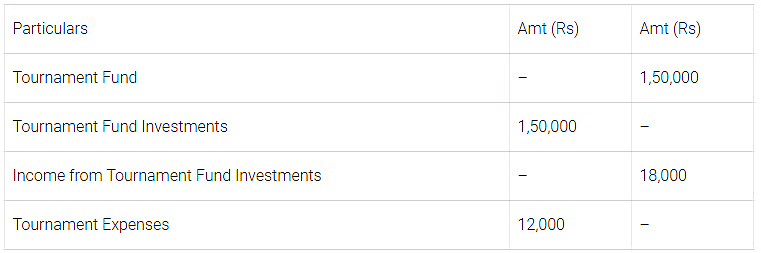

Q19: How the following items for the year ended 31st March, 2018 will be presented in the financial statements of Aisko Club. Additional Information: Interest accrued on tournament fund investments Rs 6,000.

Additional Information: Interest accrued on tournament fund investments Rs 6,000.

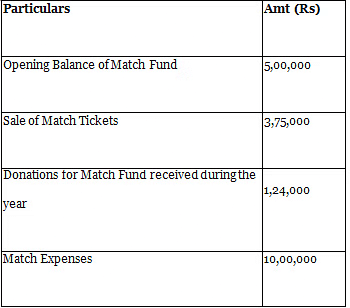

Q20: Present the following information for the year ended 31st March, 2018 in the financial statements of a not-for-profit organisation.

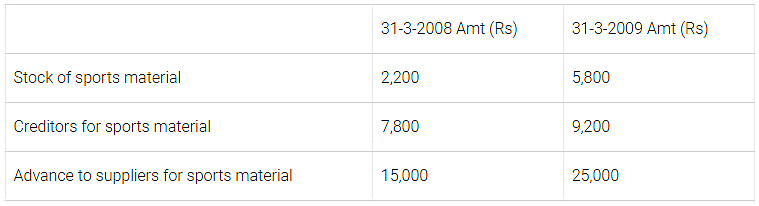

Q21: From the following information, calculate the amount of subscriptions outstanding as on 31st March, 2009.

A club has 250 members each paying an annual subscription of ₹ 1,000. The receipts and payments account for the year showed a sum of ₹ 2,65,000 received as subscriptions. The following additional information is provided

Subscriptions outstanding on 31st March, 2008 – 40000

Subscriptions received in advance on 31st March, 2009 – 30000

Subscriptions received in advance on 31st March, 2008 – 12000

Q22: State the meaning of non-profit organisation.

Q23: What is the capital fund? How is it calculated?

Q24: What is subscription? How is it calculated?

Q25: Show the treatment of the following items by a not-for-profit organisation.

(i) Annual subscription

(ii) Specific donation

(iii) Sale of fixed assets

(iv) Sale of old periodicals

(v) Sale of sports material

(vi) Life membership fees

Q26: Distinguish between not-for-profit organisations and profit-earning organisations.

Q27: Are entrance/admission fees a revenue receipt?

Q28: State the nature of the receipts and payments account.

Q29: Name the account that shows the classified summary of transactions of a cash book in a not-for-profit organisation.

Q30: Why adjustments for outstanding expenses, prepaid expenses or depreciation are not made in the receipts and payments account?

Q31: State the basis of accounting, on which a receipts and payments account is prepared in the case of a not-for-profit organisation.

Q32: Can the balance in the receipts and payments account be treated as income for the period?

Q33: Every receipt and payment, whether capital or revenue and irrespective of the period is recorded in the receipts and payments account. Why? Give reason.

Q34: Explain the statement, ‘receipts and payments account is a summarised version of cash book’.

Q35: What are the features of receipts and payments accounts?

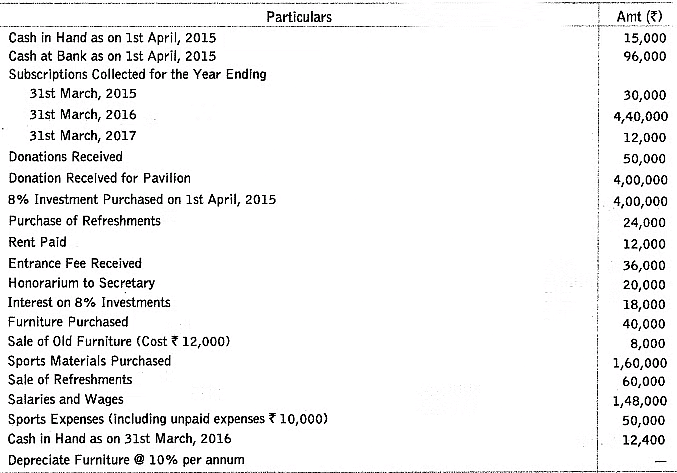

Q36: From the following particulars relating to Royals Club, New Delhi, prepare a receipts and payments account for the year ending 31st March, 2016.

Q37: Where is general donation received shown in the final accounts of a non-profit organisation?

Q38: Where will you record the life membership fees while preparing the final accounts of a non-profit organisation?

Q39: The income and expenditure account is prepared following which basis of accounting?

Q40: State the nature of the income and expenditure account.

Q41: Write one difference between ‘receipts and payments account’ and ‘income and expenditure account’.

Q42: Receipts and payments account and income and expenditure account have a similarity between them. State the similarity.

Q43: How is the capital fund of a non-profit organisation calculated if it is not given in the question?

Q44: What is the amount or property received by a non-profit organisation as stated by the will of a deceased person commonly known as?

Q45: Name the account that is similar to a profit and loss account in the case of a not-for-profit organisation.

Q46: All the revenue items relating to the current accounting period are shown in the income and expenditure account. Why?

Q47: Name the term used for denoting ‘excess of income over expenditure’ in the case of non-profit organisations

Q48: What is the term given to excess of expenditure over income in the case of non-profit organisations?

Q49: Honorarium is a kind of remuneration paid to a person who is not an employee of a non-profit organisation. What kind of expenditure is it?

Q50: ‘Income and expenditure account of a not-for-profit organisation is akin to profit and loss account of a business concern.” Explain the statement,

Q51: Explain the basic features of income and expenditure accounts,

Q52: Show the treatment of items of income and expenditure account when there is a specific fund for those items.

Q53: Distinguish between income and expenditure account and profit and loss account.

Q54: Distinguish between income and expenditure accounts and receipts and payment accounts.

Q55: From the following information of a not-for-profit organisation, show the ‘sports material’ items in the ‘income and expenditure account’ for the year ending 31st March, 2009 and the balance sheets as of 31st March, 2008 and 31st March, 2009. Payment to suppliers for the sports material during the year was ₹ 1,20,000, there were no cash purchases made.

Payment to suppliers for the sports material during the year was ₹ 1,20,000, there were no cash purchases made.

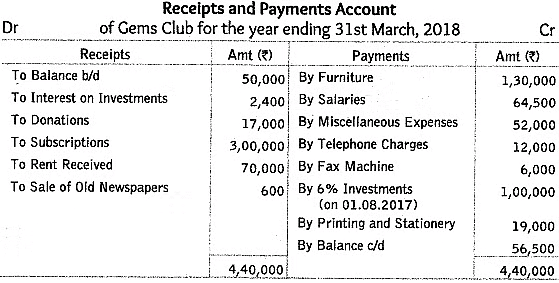

Q56: Prom the following information of Gems Club, prepare income and expenditure account for the year ended 31st March, 2018.

Receipts and Payments Account

Additional Information: Subscriptions received included ₹ 15,000 for 2018-19. The amount of subscriptions outstanding on 31st March, 2018 was ₹ 20,000. Salaries unpaid on 31st March, 2018 were ₹ 8,000 and rent receivable was ₹ 2,000. The opening stock of printing and stationery was ₹ 12,000, whereas the closing stock was ₹ 15,000.

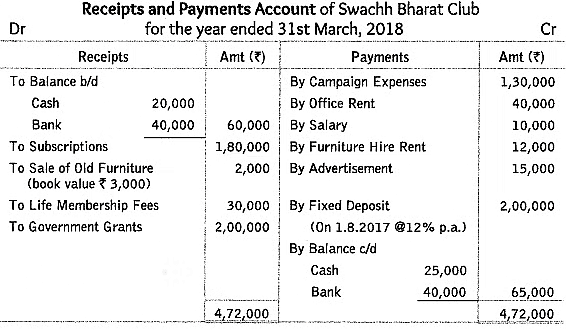

Q57: From the following receipts and payments account and additional information of Swachh Bharat Club, New Delhi for the year ended 31st March, 2018, prepare income and expenditure account and balance sheet.

Receipts and Payments Account of Swachh Bharat Club

Additional Information: Assets on 1.4.2017 were Books ₹ 50,000 and computers ₹ 75,000. liabilities and Capital fund on 1.4.2017 were Creditors ₹ 60,000; Capital fund ₹ 1,28,000.

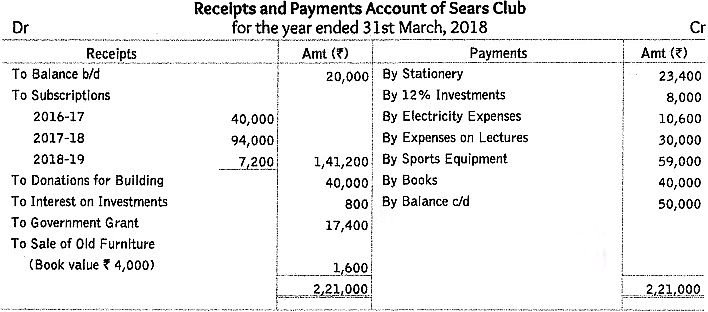

Q58: From the following receipts and payments account and additional information, prepare the income and expenditure account and balance sheet of Sears Club, Noida as on 31st March, 2018.

Additional Information:(i) The club has 200 members each paying an annual subscription of ₹ 1,000. ₹ 60,000 were in arrears for last year and 25 members paid in advance in the last year for the current year.

(ii) Stock of stationery on 1-4-2017 was ₹ 3,000 and 31-3-2018 was ₹ 4,000.

Q59: Which of the following is/are account(s) in NPO where outstanding expenses, prepaid expenses, etc are not recorded?

(a) Receipt and payment account

(b) Income and expenditure account

(c) Balance sheet

(d) All of these

Q60: What is the source of income for a non-profit organisation?

(a) Subscriptions from members

(b) Donations

(c) Legacies

(d) All of these

Q61: Non-profit organisations provide its services in the field of

(a) education

(b) healthcare

(c) Both (a) and (b)

(d) manufacturing of goods

Q62: Receipt and payment account is

(a) personal account

(b) real account

(c) capital account

(d) final account

Q63: Which of the following cannot be recorded in the receipt and payment account?

(a) Subscription received in advance

(b) Last year subscription received

(c) Current year outstanding subscription

(d) All of the above

Q64: On 1st January, 2017 outstanding subscription ₹ 160. For 2017, the amount received from subscription was ₹ 4,200. On 31st December, 2017 outstanding subscription ₹ 240. Which of the following will be recorded in the receipt and payment account as a subscription received?

(a) ₹ 4,200

(b) ₹ 4,280

(c) ₹ 4,120

(d) ₹ 4,600

Q65: Specific donations appearing on the receipts side of the receipt and payment account are to be carried to

(a) debit side of income and expenditure account

(b) assets side of the balance sheet

(c) liabilities side of the balance sheet

(d) credit side of income and expenditure account

Q66: The income and expenditure account is

(a) personal account

(b) real account

(c) nominal account

(d) None of these

Q67: Income and expenditure account records transactions of

(a) capital nature

(b) revenue nature

(c) Both (a) and (b)

(d) None of these

Q68: Subscription

2014 – 2015 – ₹ 1,200

2015 – 2016 – ₹ 26,500

2016 – 2017 – ₹ 500

Subscription outstanding as on 31st March, 2015 was ₹ 2,000 and on 31st March, 2016 ₹ 2,500. Amount to be shown in income and expenditure account will be

(a) ₹ 25,800

(b) ₹ 24,800

(c) ₹ 28,200

(d) ₹ 27,500

Q69: The balance of income and expenditure account before adjustment is ₹ 400 deficit. Accrued interest-? 600 Outstanding wages ₹ 300 Prepaid insurance ₹ 200 Amount after adjustment will be

(a) ₹ 200 deficit

(b) ₹ 100 deficit

(c) ₹ 100 saving/surplus

(d) ₹ 300 surplus

Q70: Any excess of assets over liabilities in non-profit organisation is called

(a) cash

(b) working capital

(c) loan

(d) capital fund

Q71: Balance of income and expenditure account is transferred to

(a) assets side of the balance sheet

(b) liabilities side of the balance sheet

(c) capital fund

(d) adjusted in assets

Q72: Consider the following information.

Tournament fund ₹ 20,000;

Tournament expenses ₹ 6,000;

Receipt from tournament ₹ 9,000.

Amount to be transferred to liabilities side of balance sheet will be

(a) ₹ 22,000

(b) ₹ 23,000

(c) ₹ 18,000

(d) ₹ 230

Q73: Find insurance premium to be debited to income and expenditure account?

If prepaid premium (opening) is ₹ 2,000, Prepaid premium closing ₹ 2,800,

Premium paid during the year ₹ 7,200.

(a) ₹ 6,400

(b) ₹ 8,000

(c) ₹ 12,000

(d) None of these

Access the Worksheet Solutions here.

|

51 videos|270 docs|51 tests

|

FAQs on Worksheet: Accounting for Not-for-Profit Organizations - Accountancy Class 12 - Commerce

| 1. What are the main differences between accounting for for-profit and not-for-profit organizations? |  |

| 2. How should not-for-profit organizations report their financial statements? | |

| 3. What is fund accounting, and why is it important for not-for-profit organizations? | |

| 4. How do not-for-profit organizations handle donations in their accounting? | |

| 5. What are the key financial indicators for assessing the performance of a not-for-profit organization? | |

Sample Paper

,MCQs

,Semester Notes

,Viva Questions

,mock tests for examination

,practice quizzes

,Previous Year Questions with Solutions

,study material

,ppt

,past year papers

,Objective type Questions

,shortcuts and tricks

,Exam

,Extra Questions

,Worksheet: Accounting for Not-for-Profit Organizations | Accountancy Class 12 - Commerce

,Worksheet: Accounting for Not-for-Profit Organizations | Accountancy Class 12 - Commerce

,Important questions

,Summary

,Free

,Worksheet: Accounting for Not-for-Profit Organizations | Accountancy Class 12 - Commerce

,video lectures

;

Worksheet: Accounting for Not-for-Profit Organizations Free PDF Download

Importance of Worksheet: Accounting for Not-for-Profit Organizations

Worksheet: Accounting for Not-for-Profit Organizations Notes

Worksheet: Accounting for Not-for-Profit Organizations Commerce Questions

Study Worksheet: Accounting for Not-for-Profit Organizations on the App

|

© EduRev

|

Education Revolution

|

|