Revision Notes: The Formulation of Budget | Indian Polity for UPSC CSE PDF Download

Formulation And Execution of Budget

The budgetary process involves the following four different operations :

- the preparation of the budget

- the enactment of the budget

- the execution of the budget and

- the legislative control of public finance.

The preparation of the Budget in India involves:

- Preparat ion o f t he preli mina ry est im ate s b y t he disbursing officers–heads of offices.

- The scr utin y an d review of thes e es tima tes by t he controlling officers.

- Scrutiny and review of the revised estimates by the Accountant General and the Administrative Department.

- Scrutiny and review of these revised estimates by the Finance Ministry.

- The final consideration of the estimates by the Cabinet.

The method of preparation of estimates is much the same in all countries. The responsibility rests on the Executive.

In India, the financial year of the Government begins on April 1 and ends on March 31. The budget period, therefore, is April to March (of the following year). (U.K and Commonwealth countries also follow this. France and some countries in the continent follow the calendar year. U.S.A. Australia, Italy, and Sweden use July 1 to June 30.)

The exercise of budget preparation begins around September/October, with the Finance Ministry asking the various Ministries and Departments to prepare and submit separately their estimates of revenue and expenditure for the coming year, in the proforma prescribed.

The estimates of expenditure would cover existing programmes in progress and new programmes which they want to include: the former computed on the basis of actual expenditures in the previous and current years; the latter on job details, staff requirements, and other costs likely to be incurred on these schemes.

The estimates of revenue would include those from current sources of revenue and from any additional items of resource mobilisation that may be contemplated in the coming year. Along with the estimates, actual expenses for the three preceding years, are also given.

The preliminary estimates prepared by the heads of offices (i.e. the disbursing officers) are vetted by the controlling officers and the Accountant General and the Administravtive Department, and the reviewed and revised estimates ultimately reach, by December, the Finance Ministry for final scrutiny, concurrence and consolidation.

The Finance Ministry has tremendous control over the estimates of the Departments – both by reason of its being disinterested guardian of tax payers' interests, and as the provider of funds.

The Budget Department prepares a budget forecast, consolidating all the estimates received. In January, this draft Budget is examined by the Prime Minister, in consultation with the Finance Minister. His (Prime Minister's) financial policy with regard to taxation, etc. is then drawn, discussed with the Cabinet and finalised for submission to the Parliament in the last week of February.

Difficulties experienced by disbursing officers to prepare estimates are as follows:

- Estimates are prepared in Sept/Oct i.e., some 6 to 18 months earlier than the point of actual expenditure (which goes up to March of next financial year).

- Whole economy depends on monsoon, which would not have set in before the preparation of the estimates.

- Estimates have to be given, not only for the next (budget) year, but even for a large part of the current financial year.

The estimates of revenue and expenditure prepared by the departments of the governments are scrutinised by the finance department. In such scrutiny, the usual practice for the Finance Department and the line departments in the field of revenue and expenditure is to pay more attention to the new schemes being proposed for the coming year and to allow the continuance of schemes already in operation without much scrutiny.

These new schemes form only a small part of the budget of any department and so it happens that in many government and private organizations a large part of the expenditure is not critically examined each year by either the spending department or the Finance Department.

The Finance Department examines the estimates of revenue and expenditure and attempts to bring about a balance between the revenues and expenditures of the government. The budget need not always be balanced but could be a surplus budget or a deficit budget. The Finance Department usually makes a rough estimate of the type of budget it wants and based on this decision it deals with the estimates submitted by the departments. If it wants more revenue raised it has to decide on new sources of revenue and it usually fixes ceilings on the expenditures of the spending departments and based on these ceilings it has to prune the budget requests of these departments and arrive at final figures for each department.

Usually the Finance Department has a series of discussions with the line departments and pruning of schemes is done taking into consideration the priorities of the spending departments. This exercise is done considering the time of presentation of the budget in the Parliament or legislature. In India, the budget is usually presented in late February or March by the centre and the states and the exercise of discussing the demands of the states and finalising the budget is usually done during the month of November to January.

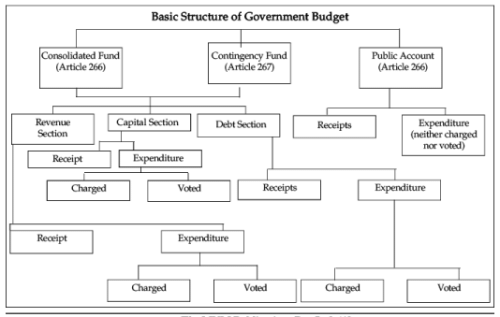

Once the budget is finalised, the budget document is printed, containing the revenue and expenditure estimates in great detail by detailed heads of expenditure and revenue. New proposals for raising revenue are kept secret till the presentation of the budget. The basic structure of the government budget is given below.

The Consolidated Fund is the fund into which all funds accruing to the government are credited and all expenditure by the government is done from this fund. Most items of expenditure can be made from this fund only after they are voted upon by the legislature. These items are called voted expenditure.

Only items like the salaries of the judges which are free from legislative scrutiny can be expended without the vote of the legislature and these items are called charged expenditures.

The Contingency Fund helps to provide for unforeseen expenditures due to sudden calamities etc.which are not provided for in the budget and which therefore have to be treated as contingencies. This fund has a fixed amount and this amount is recouped to the fund as and when the expenditure concerned is voted by the legislature.

The Public Account consists of items which are kept in suspense pending adjustment to their correct heads and other similar items. The loans raised by the government from various sources and the interest to be paid on such loans are kept separate under the head of the Public Debt. Such differentiation of expenditures is necessary to enable proper classification and accounting of governmental expenditures.

Form of Budget

The ‘Annual Financial Statement’ is composed of two parts—

(a) Budget speech of the Finance Minister, dealing with the general economic condition of the country, the proposed financial policy of the Government and explanations for the differences which occur between the budget estimates and the revised estimates of the current year.

(b) Budget estimates of the coming year, the revised estimates for the current year and the actual account for the past year showing separately, expenditure charged on the Consolidated Fund of India and on the Public Accounts of India.

Enactment of Budget

After the presentation of the budget to the legislature which in Britain and India is done through the budget speech of the Finance Minister, the budget is discussed in detail by the legislature.

Each department's budget (both the revenue and expenditure aspects) is discussed in detail after a general discussion on the budget as a whole.

This gives an opportunity to the legislators to discuss threadbare not only the finances of a department but its total functioning. Due to paucity of time the budgets of all the departments are not taken up for detailed scrutiny every year but only a few departments are subjected to detailed scrutiny in each year by the legislature. However, even during this restricted debate it is possible for the members of the legislature to exercise effective control over the department if they are well prepared and bring out any glaring defects in the working of the department.

However, in India and in Britain, the members of the legislature cannot exercise too much of a detailed control over the individual items of expenditure in the budget because under the parliamentary system the budget is considered sacrosant by the government and even a small cut in the budget is considered as a vote of no confidence in the government.

Hence the members of the legislature in India can change the individual items in the budget or add to the items of expenditure only if the government agrees to these changes. This is therefore a limitation on legislative powers in the Anglo-Saxon countries in terms of finances of the government. At the same time this ensures that the government has complete control over the budget and avoids budgetary problems as in the USA.

Mention must be made of the Committees of the legislature which help in exercise of control over the budget by the legislature.

One such Committee of importance is the Estimates Committee of the legislature which examines the budget estimates of the various government departments and attempts to find out whether the budget estimates are being prepared realistically when compared to the actual expenditures and this helps to keep the government departments on their toes in the preparation of their budgets. Another Committee of the legislature of importance in the field of financial administration is the Public Accounts Committee.

In the USA, the legislature, namely the Congress, has greater control over the budget than in the Anglo-Saxon countries. There the budget is not sacrosant like the Anglo-saxon countries and any changes made in the budget by the legislature are not considered serious enough to affect the government.

Due to the Presidential executive the leadership provided by the government in terms of the formulation and passage of the budget through Congress is not the same as in the Anglo-Saxon countries. The various Committees of the Congress exercise great powers not only in deleting items of expenditure which they do not approve of but also in reducing the overall expenditure even under such important items as Defence.

In addition these Committees add items of expenditure desired by their members and hence the powers of the legislature in financial matters is very real under this system. However, this system does lead at times to chaos in financial administration when the administration and the Congress do not agree on important expenditures and the President threatens to veto legislation not to his liking.

The powers of the legislature thus lead to financial chaos at times and even in the USA there has been moves in recent years to reduce the legislative powers in the realm of finance in order to bring some order to the system of financial administration.

In India, the Budget goes through five stages in the course of its passage in the Parliament, namely:

- Introduction in the Legislature

- General Discussion (20 - 25 hrs)

- Voting of the Demands for Grants (120-140 hrs)

- consideration and passing of the appropriation bill, and

- Consideration and passing of the taxation propos als, i.e. the Finance Bill.

Presentation of the Railway Budget by the Railway Minister precedes the presentation of the General Budget by the Finance Minister by about a week. The procedure is the same for both budgets. Unlike in Great Britainn, in India, there is no introduction of the Budget. Instead, the Finance Minister only presents the Annual Financial Statement to the Lok Sabha, with the budget speech.

This is followed by a general discussion of the Statement as a whole, in both the Houses separately. During the week of discussion, only general principles and policy under consideration, and ways and means of programme of the Government are covered but not details, or motions. The procedure follows the British practice of “voting of supplies is preceded by a ventilation of grievances”.

The next stage is voting of demands by the Lok Sabha. The Speaker fixes the date, time for discussion per item and total duration. A cut in the head of expenditure is proposed by the member who wishes to discusss the item of expenditure or generally air the grievances against the administration of the concerned department.

It may be a “Policy cut”, to disapprove of the policy underlying a demand; or an “Economy cut” to highlight the possibility of effecting economy in the proposed expenditure; or a “Token cut” to ventilate a specific grievance within the responsibility of the Government of India.

The Minister in charge of the Department replies to the point raised, at the end of the discussion.

Then, the mover may withdraw his cut motion, or the House votes. If the motion is carried, it is tantamount to “a vote of no-confidence,” on the Government. Time allotted may not be enough for discussing all the demands. So, the undiscussed demands are clubbed together and put to vote. This is called guillotine.

This is followed by the introduction of the Appropriation Bill, which comprises all the demands for grants voted. The Bill becomes an Act when it is voted. This is followed by the Finance Bill, containing proposals for taxation. When it is voted, it becomes the Finance Act.

The cardinal rule governing the voting of supplies is that no demand for a grant can be made except on the recommendations of the President. The President, for the Central Budget, and the Governor, for the State Budgets, recommend before presentation to Parliament/State Legislature.

After the passage of the Budget in the Lower House, it goes to the Upper House, which can, if considered necessary make recommendations for modifications or amendments within 14 days to the Lower House. But, the Lower House has the right to include or reject them in the Budget.

When the Budget has been passed or is deemed to have been passed by Parliament, it goes for the assent of the Head of State— the President of India. He may return the Bill for reconsideration within a period of 10 days of its submission to him. If he neither returns it, nor signs it within that date limit, it automatically becomes law. But, if he returns it to the Lower House with his recommendations, the House has to consider them but not necessarily accept them.

Altogether, there are 109 demands in the General Budget, 103 for civil and 6 for defence expenditure. The Railway Budget is divided into 23 demands. Each demand is the subject of vote, separately, by the House of People.

A demand, when voted duly, becomes a “grant”.

The Budget contains the ordinary annual estimates which constitutes the bulk of the annual receipts and charges. To meet special circumstances, there are four other kinds of grants which the House of People may be asked to make. These are:

- Votes on Account: Since the passing of the Budget can continue into the financial year (beyond April 1) advance grants are taken as “Votes on Account” for estimated expenditure, from April 1 to a part of the financial year, pending the regular passage of the Budget.

- Votes on Credit or Special Grants: To cover expenditure whose details cannot be precisely stated in the Budget on account of the indefinite character of the service to be financed (e.g., for impending war).

- Supplementary Grants: To cover insufficiency/overruns in grants taken, or if expenditure on some new services become necessary. This has to be passed by the usual procedure for the appropriation bills.

- Authorisation of charges involved in ordinary legislation: To safeguard against the possibility that ordinary legislation may, in an express or implied way, impose certain charges on the public exchequer. No bill involving such charges can go beyond second reading, unless authorised by a financial resolution of the House of People, on being moved by the Minister.

Once the budget is voted, the respective grants are communicated to the administrative ministries concerned. They, in turn, inform their respective subordinate agencies, offices, etc.

Budget-Plan Link

India has more than four decades of experience in developmental planning. Policies, which are explicily stated and implied in the plans, are sought to be translated into the budget document. The first point of linkage is at the time of formulation of Five-Year Plans.

The Second, when the annual planning exercises are undertaken, details are worked out. There are also organisational linkages: like the Prime Minister holding office of the Chairman of the Planning Commission presiding over its meetings; Finance Minister being member of the Commission; the Deputy Chairman of the Planning Commission attending meetings of the Economic Committee of the Cabinet; Cabinet Secretary being the Secretary of the Planning Commission (up to 1964); the Chief Economic Adviser of Ministry of Finance being the Economic Adviser to the Planning Commission (similarly also, some other Government officials, at various times).

An integration between planning and budgeting is sought through a combination of membership and joint participation in various Committees and decision-making agencies. However, it is a fact that finance dominates the entire exercise, relating to annual plan, both at the Centre and in the States.

The physical side of the plans and Budget are relegated to the background; exigencies of the time and political expediency prevail for deciding priorities or allocations; departmental or sectoral approach and bilateral bargaining and negotiated settlements run counter to a coordinated scheduling of programmes, schemes and projects.

Even with these limitations, the Planning Commission and the Ministries, jointly discuss and draft the programmes and budget requirements every year.

|

147 videos|780 docs|202 tests

|

FAQs on Revision Notes: The Formulation of Budget - Indian Polity for UPSC CSE

| 1. What is the purpose of budget formulation? |  |

| 2. How is a budget formulated? | |

| 3. What factors are considered during budget formulation? | |

| 4. Why is budget formulation important for effective financial management? | |

| 5. What challenges can be encountered during budget formulation? | |

ppt

,Revision Notes: The Formulation of Budget | Indian Polity for UPSC CSE

,Viva Questions

,past year papers

,Important questions

,Sample Paper

,Semester Notes

,Free

,shortcuts and tricks

,Previous Year Questions with Solutions

,practice quizzes

,study material

,Extra Questions

,Exam

,video lectures

,Objective type Questions

,Revision Notes: The Formulation of Budget | Indian Polity for UPSC CSE

,Revision Notes: The Formulation of Budget | Indian Polity for UPSC CSE

,MCQs

,mock tests for examination

,Summary

;

Revision Notes: The Formulation of Budget Free PDF Download

Importance of Revision Notes: The Formulation of Budget

Revision Notes: The Formulation of Budget

Revision Notes: The Formulation of Budget UPSC Questions

Study Revision Notes: The Formulation of Budget on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!