Bank Exams Exam > Bank Exams Notes > IBPS PO Prelims & Mains Preparation > BASEL Norms

BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams PDF Download

Introduction

Basel is a city in Switzerland which is also the headquarters of Bureau of International Settlement (BIS).- BIS fosters co-operation among central banks with a common goal of financial stability and common standards of banking regulations.

- The Bank for International Settlements (BIS) established on 17 May 1930, is the world's oldest international financial organisation. There are two representative offices in the Hong Kong and in Mexico City. In total BIS has 60 member countries from all over the world and covers approx 95% of the world GDP.

Objective

- The set of the agreement by the BCBS (BASEL COMMITTEE ON BANKING SUPERVISION), which mainly focuses on risks to banks and the financial system are called Basel accord.

- The purpose of the accord is to ensure that financial institutions have enough capital on account to meet the obligations and absorb unexpected losses.

- India has accepted Basel accords for the banking system.

- BASEL ACCORD has given us three BASEL NORMS which are BASEL 1,2 and 3.

Tier 1 - The Tier- I Capital is the core capital

- Paid up Capital, Statutory Reserves, Other disclosed free reserves, Capital Reserves which represent surplus arising out of the sale proceeds of the assets, other intangible assets belong from the category of Tier1 capital.

Tier 2 - Tier-II capital can be said to be subordinate capitals.

- Undisclosed reserves, Revaluation Reserves, General Provisions and loss reserves , Hybrid debt capital instruments such as bonds, Long term unsecured loans, Debt Capital Instruments etc belong from the category of Tier 2 capital.

Risk Weighted Assets

- RWA means assets with different risk profiles; it means that we all know that is much larger risk in personal loans in comparison to the housing loan, so with different types of loans the risk percentage on these loans also varies.

BASEL - I

- In 1988, The Basel Committee on Banking Supervision (BCBS) introduced capital measurement system called Basel capital accord, also called as Basel 1.

- It focused almost entirely on credit risk, It defined capital and structure of risk weights for banks.

- The minimum capital requirement was fixed at 8% of risk-weighted assets (RWA).

- India adopted Basel 1 guidelines in 1999.

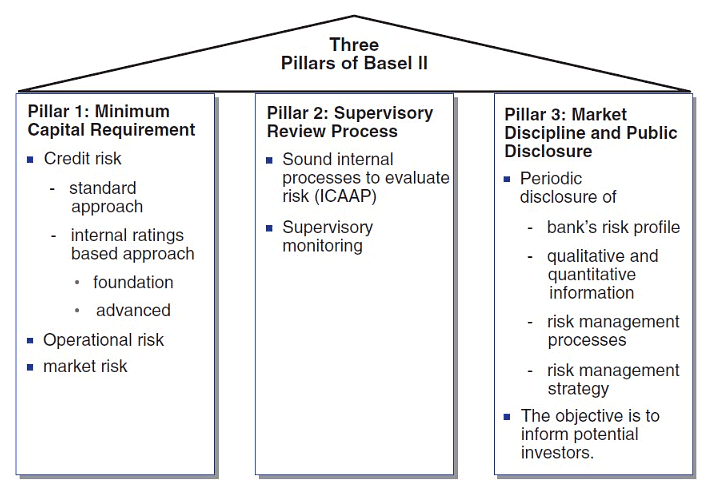

BASEL - II

In 2004, Basel II guidelines were published by BCBS, which were considered to be the refined and reformed versions of Basel I accord.

The guidelines were based on three parameters which are as follows:

- Banks should maintain a minimum capital adequacy requirement of 8% of risk assets.

- Banks were needed to develop and use better risk management techniques in monitoring and managing all the three types of risks that is credit and increased disclosure requirements.

- The three types of risk are- operational risk, market risk, capital risk.

- Banks need to mandatory disclose their risk exposure, etc to the central bank.

- Basel II norms in India and overseas are yet to be fully implemented.

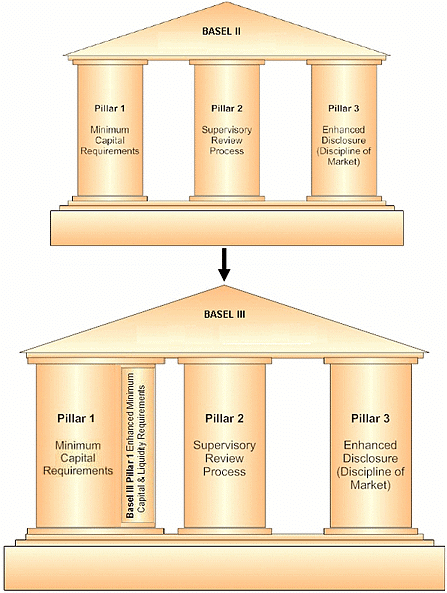

The three pillars of BASEL-3 can be understood from the following figure

Basel III

- In 2010, Basel III guidelines were released. These guidelines were introduced in response to the financial crisis of 2008.

- In 2008, Lehman Brothers collapsed in September 2008, the need for a fundamental strengthening of the Basel II framework had become apparent.

- Basel III norms aim at making most banking activities such as their trading book activities more capital-intensive.

- The guidelines aim to promote a more resilient banking system by focusing on four vital banking parameters viz. capital, leverage, funding and liquidity.

- Presently, the Indian banking system follows Basel III norms. Additionally, the RBI has extended Basel III capital framework to All India Financial Institutions (AIFIs) from April 2024.

- The Reserve Bank of India has fully implemented Basel III capital regulations, with continuous refinements based on evolving risk factors

Important Points Regarding Implementation of Basel III

- The Government of India has been infusing capital into Public Sector Banks (PSBs) to strengthen their financial position and ensure compliance with Basel III norms

- The government has announced a capital infusion of Rs 55,250 crore in ten public sector banks, including Punjab National Bank (Rs 16,000 crore), Union Bank (Rs 11,700 crore), Bank of Baroda (Rs 7,000 crore), and Canara Bank (Rs 6,500 crore), to enhance their capital and meet global risk norms

- This capital infusion is part of the government's ongoing efforts to strengthen PSBs, with significant allocations made in recent budgets to support these bank

- The Indian government has infused significant capital into PSBs over the years. However, in 2025, the focus has shifted to strategic stake sales in public sector banks to ensure compliance with the 25% public shareholding mandat

- The Finance Minister has highlighted the need for capital infusion in public sector banks but has also introduced alternative strategies, such as stake sales, to enhance their financial health and governance.

The document BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams is a part of the Bank Exams Course IBPS PO Prelims & Mains Preparation.

All you need of Bank Exams at this link: Bank Exams

|

670 videos|994 docs|322 tests

|

FAQs on BASEL Norms - IBPS PO Prelims & Mains Preparation - Bank Exams

| 1. What are the BASEL norms in banking? |  |

Ans.The BASEL norms, established by the Basel Committee on Banking Supervision, are a set of international banking regulations aimed at enhancing the stability and resilience of the financial system. They focus on capital adequacy, stress testing, and market liquidity risk. The key agreements are BASEL I, II, and III, with each iteration introducing more stringent capital requirements and risk management practices.

| 2. How do BASEL norms affect banks' capital requirements? | |

Ans.BASEL norms require banks to maintain a minimum level of capital to cover risks associated with their operations. Under BASEL III, banks must hold a common equity tier 1 (CET1) capital ratio of at least 4.5% of risk-weighted assets, along with additional capital buffers. This ensures banks have enough capital to absorb losses and continue operations during financial stress.

| 3. What is the significance of capital adequacy ratios in BASEL norms? | |

Ans.Capital adequacy ratios (CAR) are crucial in BASEL norms as they measure a bank's available capital relative to its risk-weighted assets. This ratio is essential for ensuring that banks can absorb a reasonable amount of loss and comply with statutory capital requirements. Higher CAR indicates a stronger financial position, reducing the likelihood of bank failure.

| 4. How do BASEL norms impact risk management practices in banks? | |

Ans.BASEL norms promote improved risk management practices within banks by requiring them to identify, assess, and manage various risks, including credit, market, operational, and liquidity risks. Banks must implement robust risk management frameworks and conduct regular stress testing to ensure they can withstand adverse economic conditions, thereby enhancing their overall stability.

| 5. What challenges do banks face in complying with BASEL norms? | |

Ans.Banks face several challenges in complying with BASEL norms, including the need for significant investments in technology and systems to track and manage risk exposures. Additionally, the complexity of regulations can lead to difficulties in interpretation and implementation. Balancing compliance costs with profitability while maintaining sufficient capital levels can also pose a significant challenge for financial institutions.

About this Document

4.79/5

Rating

Sep 02, 2025

Last updated

Related Exams

Document Description: BASEL Norms for Bank Exams 2025 is part of IBPS PO Prelims & Mains Preparation preparation.

The notes and questions for BASEL Norms have been prepared according to the Bank Exams exam syllabus. Information about BASEL Norms covers topics

like Introduction and BASEL Norms Example, for Bank Exams 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for BASEL Norms.

Introduction of BASEL Norms in English is available as part of our IBPS PO Prelims & Mains Preparation

for Bank Exams & BASEL Norms in Hindi for IBPS PO Prelims & Mains Preparation course.

Download more important topics related with notes, lectures and mock test series for Bank Exams

Exam by signing up for free. Bank Exams: BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams

Description

Full syllabus notes, lecture & questions for BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams - Bank Exams | Plus excerises question with solution to help you revise complete syllabus for IBPS PO Prelims & Mains Preparation | Best notes, free PDF download

Information about BASEL Norms

In this doc you can find the meaning of BASEL Norms defined & explained in the simplest way possible. Besides explaining types of

BASEL Norms theory, EduRev gives you an ample number of questions to practice BASEL Norms tests, examples and also practice Bank Exams

tests

Related Searches

Objective type Questions

,Viva Questions

,Free

,mock tests for examination

,shortcuts and tricks

,past year papers

,video lectures

,Exam

,study material

,Previous Year Questions with Solutions

,Extra Questions

,Sample Paper

,BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams

,BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams

,Important questions

,BASEL Norms | IBPS PO Prelims & Mains Preparation - Bank Exams

,practice quizzes

,Summary

,Semester Notes

,ppt

,MCQs

;

Additional Information about BASEL Norms for Bank Exams Preparation

BASEL Norms Free PDF Download

The BASEL Norms is an invaluable resource that delves deep into the core of the Bank Exams exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the BASEL Norms now and kickstart your journey towards success in the Bank Exams exam.

Importance of BASEL Norms

The importance of BASEL Norms cannot be overstated, especially for Bank Exams aspirants.

This document holds the key to success in the Bank Exams exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

BASEL Norms Notes

BASEL Norms Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to BASEL Norms.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, BASEL Norms Notes on EduRev are your ultimate resource for success.

BASEL Norms Bank Exams Questions

The "BASEL Norms Bank Exams Questions" guide is a valuable resource for all aspiring students preparing for the

Bank Exams exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study BASEL Norms on the App

Students of Bank Exams can study BASEL Norms alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the BASEL Norms,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of BASEL Norms is prepared as per the latest Bank Exams syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup on EduRev and stay on top of your study goals

10M+ students crushing their study goals daily