Best Study Material for UPSC Exam

UPSC Exam > UPSC Notes > Commerce & Accountancy Optional Notes for UPSC > Salaries - 3

Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC PDF Download

| Table of contents |

|

| Provident Fund Schemes |

|

| Tax Treatment of Provident Funds |

|

| Certain Other Aspects of Taxable Salary |

|

| Deduction under Section 80C |

|

Provident Fund Schemes

A provident fund is a financial mechanism designed to provide for an individual's future needs, particularly after retirement or in the event of death. It involves regular contributions from both the employee and the employer, with the funds typically invested in government securities to earn interest. The accumulated amount is then given to the employee upon retirement or voluntary retirement and to their legal heirs in the event of their death.

There are various types of provident funds:

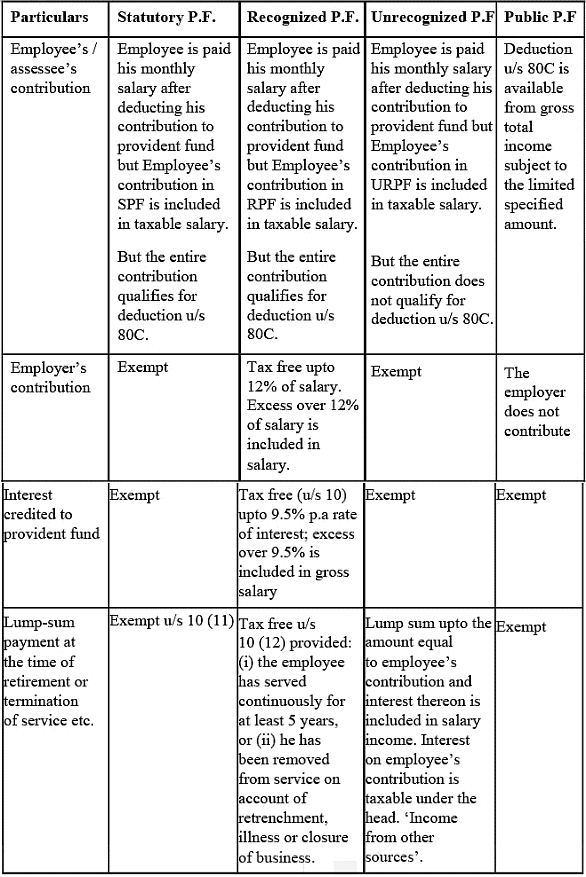

- Statutory Provident Fund: Established under the Provident Fund Act, 1925, this fund is maintained by government and semi-government departments, financial institutions like the Reserve Bank of India and the State Bank of India, railways, statutory corporations, universities, colleges, and local bodies.

- Recognized Provident Fund: This fund is recognized by the Commissioner of Income Tax in accordance with the rules outlined in the Fourth Schedule of the Income Tax Act, 1961. It includes provident funds established under the Employees Provident Fund Act, 1952, and is crucial for tax purposes. If a provident fund is recognized by the Provident Fund Commissioner but not by the Commissioner of Income Tax, tax concessions cannot be extended to the contributions to such a fund.

- Unrecognized Provident Fund: This fund is not recognized by the Commissioner of Income Tax and therefore does not receive tax relief. It is typically maintained by private employers.

- Public Provident Fund (PPF): This scheme, introduced by the central government, is aimed at encouraging savings, particularly for self-employed individuals such as doctors, lawyers, accountants, actors, and traders. It allows individuals and associations of persons to deposit funds, with accounts being opened at specified branches of nationalized banks and the State Bank of India. The minimum subscription amount is Rs. 500, and the maximum is Rs. 1,50,000 per year. Interest is credited annually but is payable only at maturity, which occurs after 15 years. The entire amount, along with interest, is tax-exempt upon maturity, and the account can be extended for another 5 years. Non-resident Indians and Hindu Undivided Families (HUFs) are not eligible for this account.

- Approved Superannuation Fund: This fund is approved by the Commissioner of Income Tax and is intended solely for providing annuities to employees upon retirement after a specified age or upon incapacitation prior to retirement, or for the widows or dependents of such employees in the event of their death.

Question for Salaries - 3

Try yourself:

What is the purpose of a provident fund?View Solution

Tax Treatment of Provident Funds

The tax exemptions related to these funds are as follows:

- Employer's contribution is tax-exempt.

- Employee's contribution is eligible for deduction under section 80C.

- Interest on the accumulated balance is tax-exempt.

Provisions of Provident Funds

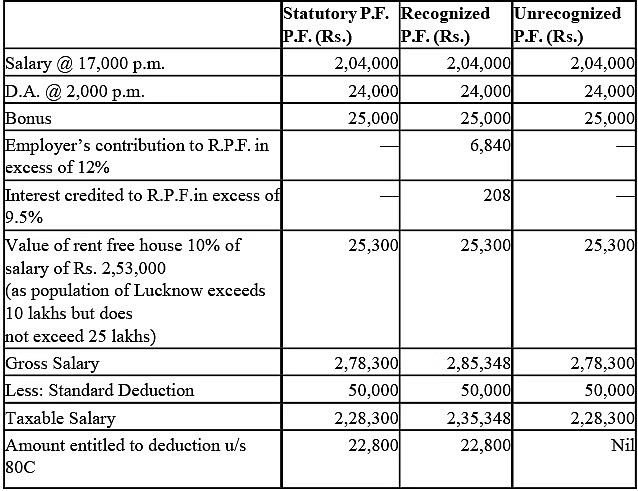

Illustration 1: Mr. Gaurav Modi is employed in Khadi Samiti in Lucknow. He is in receipt of a salary of Rs. 17,000 p.m. and a dearness allowance of Rs. 2,000 p.m. He contributes 10% of his salary and dearness allowance to a provident fund to which Khadi Samiti contributes 15%. He is provided with a rent free unfurnished house by his employer. He received Rs. 25,000 as bonus during previous year. The interest credited to his provident fund @ 12% amounted to Rs. 1,000. Compute taxable income of Mr. Gaurav Modi for the assessment year 2023-24, if the P.F. in question is (i) Statutory (ii) Recognized or (iii) Unrecognized. On what amount the assessee is entitled to deduction u/s 80C.

Computation of Taxable Income of Mr. Gaurav Modi for AY 2023-24

Note: Calculation of Recognized P.F.

Employer’s contribution RPF = 2, 28,000 (Salary + D.A.)

Assessee is entitled to deduction u/s 80C, upto a maximum amount of Rs. 1,50,000 in respect of his contribution to statutory or recognized provident fund, i.e. 10% of his salary and D.A., say Rs. 22,800. He is not entitled to deduction u/s 80C in respect of his contribution to unrecognized provident fund.

Salary = Basic Pay + D.A+ Bonus = 2,04,000+ 24,000+25,000 = Rs. 2,53,000

Certain Other Aspects of Taxable Salary

When calculating taxable income from salary, we must consider the following aspects of salary:

- Waivers of Salary: Once salary accrues to an employee, it becomes taxable under Section 15. Even if the employee waives their right to receive payment, it will be considered as a mere application of their income, and their tax liability will remain unaffected.

- Surrender of Salary: If an employee surrenders their salary to the central government under Section 2 of the Voluntary Surrender of Salaries, the surrendered salary will be excluded when computing their salary income.

- Tax-Free Salaries: An employer can choose to pay the tax on behalf of the employee and not deduct the same from the employee's salary. However, while computing the employee's income, the tax paid by the employer will be added to the salary income of the employee.

Question for Salaries - 3

Try yourself:

What is the tax treatment of provident funds in India?View Solution

|

Download the notes

Salaries - 3

|

Download as PDF |

Download as PDF

Deduction under Section 80C

Section 80C allows certain investments and expenditures to be tax-exempt. This deduction is available to individual or Hindu Undivided Family (HUF) taxpayers (assessees) for specified qualifying amounts paid or deposited during the previous year.

Gross Qualifying Amount: The deductions available under section 80C include:

- Life Insurance Premium

- Deferred Annuity

Contributions to Provident Fund, Public Provident Fund, and certain shares and debentures

- Eligibility of Assessee: This deduction is allowed only to individuals or Hindu Undivided Families (HUFs) from their gross total income computed as per the provisions of the Act.

- Deduction Limit: The deduction for the following savings/investments cannot exceed Rs. 1,50,000:

- Life Insurance Premium: The premium paid by an assessee on their life, their spouse's life, and their children's lives, as well as contributions to employee insurance plans, joint life premiums, and group insurance.

- Deferred Annuity: Payments for a deferred annuity on the life of the assessee, their spouse, or their children.

Contributions to Statutory Provident Fund, Recognized Provident Fund, and Public Provident Fund.

- Payment under Unit Linked Insurance Plans (ULIPs).

- Amounts deducted from a government employee's salary for deferred annuities or provisions for their wife and children (restricted to 1/5th of salary).

- Contributions to Approved Superannuation Funds.

- Contributions to Notified Central Government Securities or Deposit Schemes.

- Reinvestment of accrued interest on National Saving Certificates (NSCs).

- Deposits in National Housing Schemes or contributions to pension funds.

- Contributions to Mutual Funds established under section 10(23D) or Equity Linked Saving Schemes of Unit Trust of India.

- Tuition fees for children's education.

- Sukanya Samridhi accounts for girl children.

- Payments made for annuity plans of the Life Insurance Corporation or any other insurer.

For Hindu Undivided Families (HUFs), the following payments in the previous year qualify for deduction under section 80C:

- Premiums paid on life insurance for any family member.

- Contributions to Public Provident Fund.

- Contributions to Notified Central Government Securities or Deposit Schemes.

- Contributions to Mutual Funds established under section 10(23D).

- National Saving Certificates.

- Accrued interest on NSCs.

- Deferred Annuity payments.

- Contributions to deposit schemes provided by public sector companies or authorities established for solving residential problems or development.

- Payments for the purchase or construction of a new residential house.

- Stamp duty, registration fees, and other transfer expenses for house property.

- Contributions to National Housing Bank Deposit Schemes or pension funds.

- Contributions to Mutual Funds established under section 10(23D) or Equity Linked Saving Schemes of Unit Trust of India.

- Investments in term deposits.

- Payments for Sukanya Samridhi accounts.

- Payments for annuity plans of the Life Insurance Corporation or any other insurer.

Note:

- Investments/deposits are qualified on a payment basis under section 80C, meaning that the amount paid is eligible for deduction, whether the payment is related to the last year or the next year.

- If joint life premiums are paid on the life of the assessee, their spouse, or their children, the deduction is admissible. However, if the joint life policy involves outsiders, no such deduction is allowed.

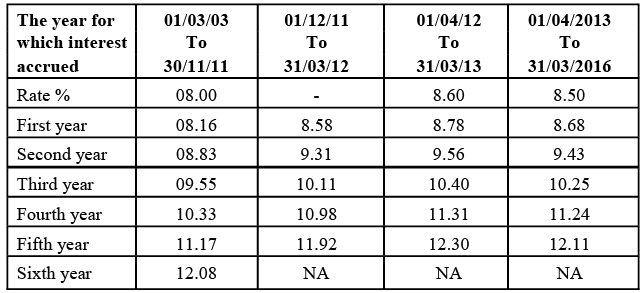

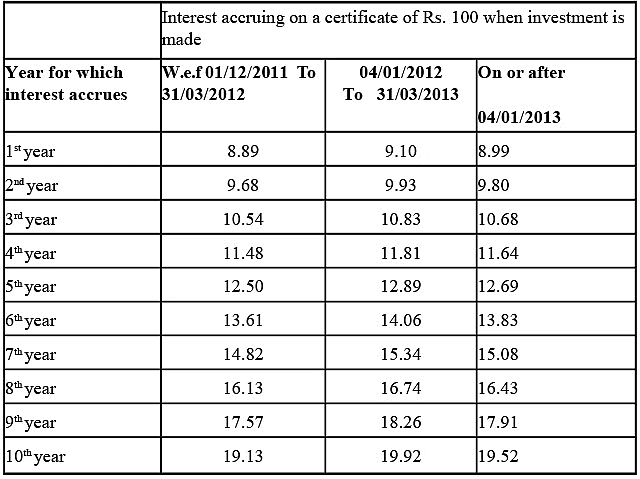

Interest Table accrued on N.S.C. (VIII Issue) Interest accruing on a certificate of Rs. 100

Interest accruing on a certificate of Rs. 100

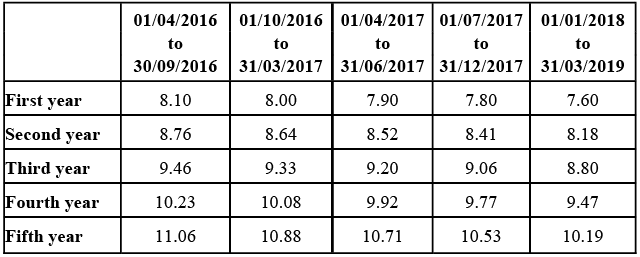

NSC IX ISSUE

The table shows the amount of interest accrued at the end of each year:

Important Note: National Saving Certificates VIII issue mature after 5 years. The accrued interest of the 5th year is not treated as reinvested. Hence, no deduction under Section 80C is allowed on this interest from the 5th year.

Cancellation of Deduction under Section 80C: Under the following circumstances, the deduction shall be cancelled:

- If the life policy is terminated on notice or due to non-payment of premium after two years of paying premiums, the premium of that year will not be eligible for deduction under Section 80C. The amount previously deducted under this section shall be added to the income of the assessee.

- If contributions to a policy or fund are stopped before 5 years, the deduction will not be allowed in the year of closing. The deduction previously allowed on such contributions shall be included in the income in the year of its closing.

- If an assessee has received a deduction under Section 80C for a loan taken for the purchase or construction of a residential house and sells that house within 5 years, the previously availed deduction shall be cancelled. This cancelled deduction shall be included in the taxable income of the year in which it is cancelled.

- If an assessee has received a deduction under Section 80C by purchasing shares or debentures of an infrastructure company and sells them within 3 years of the purchase date, the previously availed deduction will be cancelled. Such a deduction shall be included in the income of the year in which it is cancelled.

The document Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC is a part of the UPSC Course Commerce & Accountancy Optional Notes for UPSC.

All you need of UPSC at this link: UPSC

|

180 videos|153 docs

|

FAQs on Salaries - 3 - Commerce & Accountancy Optional Notes for UPSC

| 1. What is the tax treatment of Provident Fund schemes? |  |

| 2. Can employers contribute to employees' Provident Fund accounts? | |

Ans. Yes, employers can make contributions to employees' Provident Fund accounts. Employer contributions are also eligible for tax benefits under the Income Tax Act. However, the total contribution from both the employer and employee cannot exceed a certain limit.

| 3. Are withdrawals from Provident Fund accounts taxable? | |

Ans. Withdrawals from Provident Fund accounts are generally tax-free if certain conditions are met. If the employee has completed five years of continuous service, withdrawals from Provident Fund accounts are not taxable. However, if the withdrawal is made before five years, it may be subject to taxation.

| 4. How can employees claim deductions under Section 80C for Provident Fund contributions? | |

Ans. Employees can claim deductions under Section 80C for Provident Fund contributions by providing details of their contributions in the specified format while filing their income tax returns. The deduction can be claimed up to a certain limit, which is subject to change based on the prevailing tax laws.

| 5. Are there any other aspects of taxable salary related to Provident Fund schemes that employees should be aware of? | |

Ans. Apart from Provident Fund contributions, certain other components of the salary, such as bonus, commission, and allowances, may also be considered taxable. Employees should consult with a tax advisor or refer to the Income Tax Act to understand the tax implications of different salary components in relation to Provident Fund schemes.

Related Exams

About this Document

Apr 08, 2025

Last updated

Document Description: Salaries - 3 for UPSC 2025 is part of Commerce & Accountancy Optional Notes for UPSC preparation.

The notes and questions for Salaries - 3 have been prepared according to the UPSC exam syllabus. Information about Salaries - 3 covers topics

like Provident Fund Schemes, Tax Treatment of Provident Funds, Certain Other Aspects of Taxable Salary, Deduction under Section 80C and Salaries - 3 Example, for UPSC 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Salaries - 3.

Introduction of Salaries - 3 in English is available as part of our Commerce & Accountancy Optional Notes for UPSC

for UPSC & Salaries - 3 in Hindi for Commerce & Accountancy Optional Notes for UPSC course.

Download more important topics related with notes, lectures and mock test series for UPSC

Exam by signing up for free. UPSC: Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC

Description

Full syllabus notes, lecture & questions for Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC - UPSC | Plus excerises question with solution to help you revise complete syllabus for Commerce & Accountancy Optional Notes for UPSC | Best notes, free PDF download

Information about Salaries - 3

In this doc you can find the meaning of Salaries - 3 defined & explained in the simplest way possible. Besides explaining types of

Salaries - 3 theory, EduRev gives you an ample number of questions to practice Salaries - 3 tests, examples and also practice UPSC

tests

Related Searches

MCQs

,practice quizzes

,ppt

,mock tests for examination

,shortcuts and tricks

,Viva Questions

,Exam

,Semester Notes

,past year papers

,Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC

,Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC

,study material

,Important questions

,Previous Year Questions with Solutions

,Salaries - 3 | Commerce & Accountancy Optional Notes for UPSC

,Sample Paper

,Free

,Extra Questions

,Objective type Questions

,Summary

,video lectures

;

Additional Information about Salaries - 3 for UPSC Preparation

Salaries - 3 Free PDF Download

The Salaries - 3 is an invaluable resource that delves deep into the core of the UPSC exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Salaries - 3 now and kickstart your journey towards success in the UPSC exam.

Importance of Salaries - 3

The importance of Salaries - 3 cannot be overstated, especially for UPSC aspirants.

This document holds the key to success in the UPSC exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Salaries - 3 Notes

Salaries - 3 Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Salaries - 3.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Salaries - 3 Notes on EduRev are your ultimate resource for success.

Salaries - 3 UPSC Questions

The "Salaries - 3 UPSC Questions" guide is a valuable resource for all aspiring students preparing for the

UPSC exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Salaries - 3 on the App

Students of UPSC can study Salaries - 3 alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Salaries - 3,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Salaries - 3 is prepared as per the latest UPSC syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up

within 7 days!

within 7 days!

Takes less than 10 seconds to signup