Vivek Singh Summary: India’s Tax System

India's Tax System

1. Progressive, Proportional, and Regressive Taxes:

- Progressive Tax: As income increases, the tax percentage also increases. For example, higher income brackets may be taxed at higher rates.

- Proportional Tax: The tax percentage remains constant, regardless of income levels. For instance, everyone pays the same tax rate, regardless of how much they earn.

- Regressive Tax: The tax percentage decreases as income increases. This means that higher-income individuals pay a smaller percentage of their income in tax compared to lower-income individuals.

2. Specific Tax and Ad-Valorem Tax:

- Specific Tax: This tax is fixed based on each unit of a good or service, regardless of its value. For example, a specific tax may be imposed per kilogram of a particular product.

- Ad-Valorem Tax: This tax is levied as a percentage of the value of the item, rather than its quantity, size, or weight. For instance, a tax based on the value of a luxury item rather than its physical attributes.

3. Production and Consumption-Based Tax (Indirect Taxes):

- Production Tax: Also known as origin-based tax, this is levied where goods and services are produced. For example, taxes imposed on manufacturers in a specific location.

- Consumption Tax: Also known as destination tax, this is levied where goods and services are consumed. For instance, taxes applied in the location where a product is sold to the end consumer.

4. Direct and Indirect Taxes:

- Direct Taxes: These taxes are paid directly by individuals or organizations to the government. Examples include income tax and property tax. Taxpayers pay these taxes directly to the government for various purposes.

- Indirect Taxes: These taxes are collected by intermediaries, such as retail stores, from the individuals who bear the ultimate economic burden of the tax. For example, taxes levied on goods and services purchased by consumers. Retailers collect these taxes from consumers and remit them to the government.

Classification of Taxes in India

Direct Taxes

1. Personal Income Tax

- Imposed on individuals based on their total income from various sources such as salary, rental income, and interest.

- There are two tax regimes: the old tax regime and the new tax regime. Individuals can choose either, but the new regime is the default option.

- New Tax Regime:

- No tax for income up to ₹7 lakh.

- Income slabs:

- ₹0 to ₹3 lakh: Nil

- ₹3 lakh to ₹6 lakh: 5%

- ₹6 lakh to ₹9 lakh: 10%

- ₹9 lakh to ₹12 lakh: 15%

- ₹12 lakh to ₹15 lakh: 20%

- Above ₹15 lakh: 30%

- Old Tax Regime:

- No tax for income up to ₹5 lakh.

- Allows exemptions for savings under schemes like PPF and NPS.

- Income slabs:

- ₹0 to ₹2.5 lakh: Nil

- ₹2.5 lakh to ₹5 lakh: 5%

- ₹5 lakh to ₹10 lakh: 20%

- Above ₹10 lakh: 30%

2. Corporate Income Tax (CIT)

- Imposed on the profits of companies and corporate entities.

- Two structures of CIT:

- 25.17% CIT for companies that do not claim tax exemptions.

- 34.94% CIT for companies that claim tax exemptions.

- Exemptions: Deductions allowed under various provisions.

- Surcharge and Cess: Additional charges on the tax rate.

- Minimum Alternate Tax (MAT): Introduced to ensure that companies with substantial book profits but zero tax liability due to exemptions contribute to the tax revenue.

Indirect Taxes (Before GST)

- Indirect taxes were categorized into various types before the implementation of Goods and Services Tax (GST) on July 1, 2017.

(i) MAT:

MAT is applicable to companies whose tax liability under the normal provisions is lower than 15% of their book profit.

Example:

- Company A has a taxable income of Rs. 10,00,000 and a tax rate of 30%. Normal tax liability = Rs. 3,00,000.

- Book profit = Rs. 20,00,000. MAT = 15% of Rs. 20,00,000 = Rs. 3,00,000.

- Company A pays MAT as it is higher.

(ii) Capital Gain Tax:

- Tax on profit from selling assets like stocks, bonds, property.

- Common assets: shares, real estate, art.

- Example: Buying property for Rs. 50,00,000 and selling for Rs. 70,00,000 results in a capital gain of Rs. 20,00,000, taxed accordingly.

(iii) Dividend Distribution Tax (DDT):

- Tax on dividends paid by companies to shareholders.

- Abolished in 2019; now taxed in shareholders' hands.

- Example: Company B pays Rs. 1,00,000 as dividend; previously, it paid DDT, now shareholders pay tax on this income.

(iv) Securities Transaction Tax (STT):

- Tax on buying and selling securities like shares and mutual funds on Indian stock exchanges.

- Rates vary by security type and transaction nature (purchase/sale).

- Example: Buying or selling equity shares incurs 0.1% STT on share value.

Equalization Levy

- Before 2016, only companies with permanent residence in India were subject to tax under the Income Tax Act of 1961. These companies had to register their business and establish a physical presence in India to conduct business, as there were limited digital or online services at that time.

- However, with the advancement of Information Technology, it became feasible for companies like "Google," registered in the US, to generate revenue in India through digital advertisements on their platforms. Since the Income Tax Act of 1961 did not apply to income earned by non-resident companies without a registered office or permanent residence in India, the Act could not tax Google's income from advertising in India. To address this issue, India introduced the "Equalization Levy," also known as the "Google Tax," in 2016.

- The Equalization Levy applies to foreign companies providing digital services in India without a physical presence. For instance, if a US-based company "A" and its Indian subsidiary "B" are involved in digital services, the levy would not apply to "B," which would pay normal Income Tax under the Income Tax Act of 1961. However, if "B" is not registered in India and has no physical presence but is still providing digital services in India, the Equalization Levy would apply to "B," while Income Tax would not.

- For example, if an Indian educational institute, XYZ, hires Google for advertising services, XYZ would deduct a 6% Equalization Levy from the payment to Google and remit it to the government. The Equalization Levy is not classified as an income tax under the Income Tax law but as an independent levy introduced through the Finance Act of 2016. Different types of services fall under this levy, which has been made effective on various dates. For instance, the sale of digital services (ads) was notified three years ago, and from April 1, 2020, a 2% Equalization Levy became applicable to e-commerce firms as well.

- For example, if an e-commerce firm like Amazon, registered in the US and classified as a non-resident in India, earns a revenue (not profit) of Rs. 100 from its online services, the Equalization Levy would apply.

- When companies like Amazon sell products to Indian residents through their e-commerce platforms, they are required to pay a 2% Equalization Levy on the revenue generated from these sales. This means that out of every Rs. 100 earned, Rs. 2 goes to the Government of India as this levy. However, these companies do not have to pay income tax under the Income Tax Act of 1961 in such cases.

Permanent Establishment and Income Tax

- If Amazon had a permanent establishment in India, meaning a physical presence in the country, it would be liable to pay income tax on its profits according to the Income Tax Act of 1961.

- The Equalization Levy is a direct tax imposed on revenue, not profit. This is because it is challenging for India to determine the profit of companies like Amazon, which have extensive operations in the United States and other countries.

Global Minimum Corporate Tax (GMCT)

- Profit Shifting: Large technology companies often shift their profits to countries with lower corporate tax rates. This practice involves financial transactions rather than the actual relocation of business operations. To attract more business and investment, countries compete by lowering their corporate tax rates, leading to a loss of tax revenue for the home country governments.

- Global Minimum Corporate Tax: In response to this issue, countries have agreed to implement a Global Minimum Corporate Tax (GMCT). For example, if a company based in the US with a corporate tax rate of 20% shifts its revenues to a country like Mauritius with a 5% tax rate, the GMCT of 15% allows the US government to collect an additional 10% tax from the company. This ensures that companies shifting their revenues to tax havens still pay a minimum level of tax.

- Applicability: GMCT applies to companies that have shifted their business to tax havens with lower tax rates. Companies based in countries with higher tax rates, like Mauritius, can pay the lower tax rate.

- Pillar 1: This pillar aims to distribute profits and taxing rights more fairly among countries concerning large multinational enterprises (MNEs), including digital companies. It reallocates some taxing rights over MNEs from their home countries to the markets where they have business activities and earn profits, regardless of physical presence. This aspect may reduce the need for the Equalization Levy.

- Pillar 2: This pillar introduces a global minimum corporate tax rate to set a floor on competition over corporate income tax. It allows countries to protect their tax bases by implementing a minimum corporate tax rate, related to the GMCT of 15%.

- Once the 'Global Minimum (Corporate) Tax' is implemented, India might need to eliminate the 'Equalization Levy' currently imposed on multinational technology companies like Google and Facebook.

Land Revenue

- Land revenue is determined by various State Government Acts.

- It is usually based on the classification of different land types and the cash value of the average yield from that land.

- Factors affecting productivity in monetary terms are also considered.

- The tax is levied at a rate per acre or hectare of land.

Property Tax

- Property tax in India is imposed on "real property," which includes land and any improvements made on it.

- The government assesses the monetary value of each property and levies tax in proportion to its value.

- Revenue from property tax is used for local amenities such as road repairs, park maintenance, and public schools.

- The tax rate varies by location and can differ between cities and municipalities.

- Urban local bodies like municipal boards, municipal corporations, and town area committees levy property tax under applicable laws.

Indirect Taxes

- Indirect taxes are considered regressive.

- For instance, a wealthy person buying bread for Rs. 25 (including Rs. 5 tax) pays Rs. 5 in tax.

- A poorer person buying the same bread also pays Rs. 5, but this tax constitutes a larger percentage of their income.

- This makes the tax burden heavier for the poorer individual relative to their income, illustrating the regressive nature of indirect taxes.

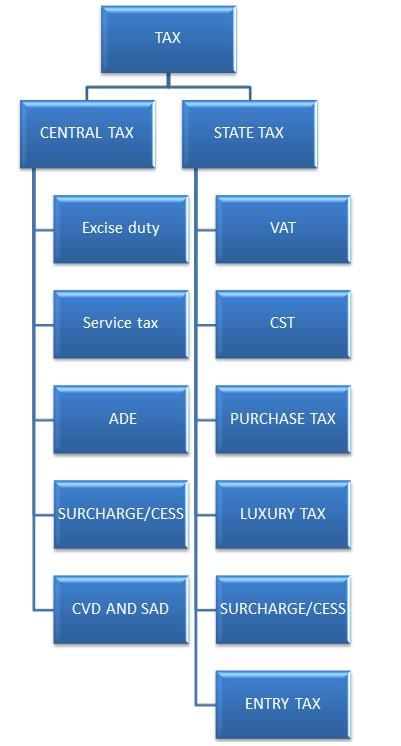

Types of Indirect Taxes

- Excise Duty : This was imposed on manufactured goods and levied when the goods left the factory premises.

- Customs Duty : This is imposed on the export and import of goods.

- Service Tax : This was imposed on the sale of services.

- Central Sales Tax (CST) : This was levied by the Centre on the sale of goods from one state to another, with the tax proceeds collected and retained by the origin state, hence it was also known as an origin-based tax.

- Value Added Tax (VAT) : This was imposed on the sale of goods within a state, and the Central government could not impose taxes on such sales. VAT was charged only on the value added at each stage of the sale.

Illustration of VAT

- Consumer A : Purchases goods worth Rs. 100 plus Rs. 10 VAT. Total cost Rs. 110.

- Consumer B : Buys goods for Rs. 300 plus Rs. 30 VAT. Total cost Rs. 330.

- Government A : Sells goods for Rs. 100, collects Rs. 10 VAT.

- Government B : Sells goods for Rs. 300, collects Rs. 30 VAT, refunds Rs. 10 VAT to Consumer B.

- In the example provided, A adds value worth Rs. 100 to a product and sells it to B for Rs. 110. A pays Rs. 10 as VAT to the government. B, in turn, adds value of Rs. 200 and pays Rs. 20 VAT to the government.

- In practice, B initially pays the total VAT of Rs. 30 to the government based on the total value addition of the product. However, when B presents the tax receipt of Rs. 10 (which B paid to A for the purchase of inputs, and A subsequently paid to the government), the government refunds this Rs. 10 to B. This process is known as the Input Tax Credit Mechanism.

- The Input Tax Credit Mechanism is designed to prevent tax avoidance by ensuring that every entity in the value chain requests a tax receipt from the previous entity to claim credits for the taxes paid on input purchases.

- Entry Tax was a tax imposed by state governments in India on the movement of goods from one state to another. It was levied by the recipient state to protect its tax base.

- Stamp Duty is a tax levied on all legal property transactions. It required a physical stamp to be attached to or impressed upon the document to indicate that the stamp duty had been paid. Since stamp duty is imposed by states, the rate varies from state to state.

Goods and Services Tax (GST)

Introduction to GST

- To grasp the concept of Goods and Services Tax (GST), it's essential to first understand the problems present in the indirect taxation system before GST was implemented on July 1, 2017.

- Let's consider an example to illustrate these problems.

Example of Taxation Before GST

- Suppose the Central Excise Duty is set at 12.5% and the Value Added Tax (VAT) rate is 10%.

- When a seller, A, sells a product to buyer B, with a value addition or sale price of Rs. 100:

- Excise Duty Calculation:

- Excise Duty (12.5%) = Rs. 100 × 12.5% = Rs. 12.5

- VAT Calculation:

- VAT (10%) = (Rs. 100 + Rs. 12.5) × 10% = Rs. 11.25

- Invoice Price: Invoice Price = Rs. 100 + Rs. 12.5 + Rs. 11.25 = Rs. 123.75

Issue of Cascading Effect

- In the example above, VAT is applied on top of the excise duty, leading to a tax-on-tax situation.

- This creates a cascading effect, increasing the effective tax rate to 23.75%.

Fragmented Tax System Before GST

- Before June 30, 2017, the Central Government imposed its own indirect taxes, such as Service Tax and Excise Duty, while State Governments imposed their own indirect taxes, like VAT and Entertainment Tax.

- When a producer manufactured a product, they had to pay both Excise Duty to the Centre and VAT to the State.

- This led to a tax-on-tax situation and a cascading effect, making products more expensive in the market.

- Additionally, VAT credits were not available across states, and different states had varying VAT rates (e.g., 1%, 4%, 12.5%, 20%) and exemptions for different product categories.

- These issues resulted in different effective tax rates in different states for various goods and services, leading to price discrepancies and fragmenting India into a heterogeneous market, adversely affecting business and investment.

Goods and Services Tax (GST)

The implementation of Goods and Services Tax (GST) nationwide is the most significant indirect tax reform since India's independence.

- It took nearly 16 years from the initial idea, through the formation of a task force, to its passage in Parliament.

- GST represents a massive, nationwide effort to build consensus across multiple political parties and is a prime example of "cooperative federalism."

- This reform is the result of a grand compromise between 29 states, seven Union Territories (UTs), and the Central government.

- States agreed to relinquish their authority to impose sales tax on goods (Value Added Tax or VAT), while the Centre gave up its rights to impose excise and service taxes.

- In return, they would each receive a share of the unified GST collected nationally.

- The promise of greater efficiency, competitiveness, easier business operations, and increased overall tax collections motivated this agreement.

What GST Replaces

- GST has replaced 17 different Central and State indirect taxes, including:

- Central Excise Duty

- Additional Excise Duty

- Service Tax

- State taxes like VAT, Entertainment Tax, Entry Tax, Purchase Tax, and Luxury Tax

How GST Works

- GST is a single indirect tax on the supply of goods and services across India, creating one unified common market.

- When a product or service is sold to consumers in India, only one indirect tax is applied: GST, which includes:

- Central GST (CGST) for the Central government

- State GST (SGST) for the State government

- For products sold across states, Integrated GST (IGST) is levied by the Centre.

- GST is essentially a value-added tax imposed only on the value added at each stage of the supply chain.

Constitutional Amendment and Legislative Framework

- To introduce GST, the Constitution (101st) Amendment Act 2016 was passed in September 2016.

- Following this, the Central Government enacted the Central GST (CGST) Act, and each State Government enacted the State GST (SGST) Act in their respective States.

- The Central Government also enacted the Integrated Goods and Services Tax (IGST) Act for interstate transactions and the GST (Compensation to States) Act 2017 to address revenue shortfalls for States.

GST Council

- The Constitution (101st) Amendment Act 2016 established the GST Council, comprising:

- The Union Finance Minister

- The Union Minister of State in charge of Revenue or Finance

- The Minister in charge of Finance or Taxation, or any other Minister nominated by each State Government

Role of GST Council

The GST Council is responsible for making recommendations to the Union and State governments regarding:

- The GST Council plays a crucial role in making important decisions about the Goods and Services Tax (GST). Here are the key points regarding its composition, functions, and the process of decision-making:

Composition of the GST Council

- The GST Council consists of the following members:

- Union Finance Minister: The Union Finance Minister is the chairperson of the GST Council.

- State Finance Ministers: The Finance Ministers of the states and Union territories are also part of the Council.

Functions of the GST Council

The GST Council has the authority to make recommendations on various aspects of GST, including:

- Taxes, cesses, and surcharges that may be included in GST.

- Goods and services that may be exempt from GST.

- Integrated Goods and Services Tax (IGST).

- Threshold limits for turnover below which goods and services may be exempt from GST.

- GST rates, including floor rates and bands for goods and services.

- Special rates for specific periods to raise additional resources during natural disasters.

- Any other matters related to GST as decided by the Council.

Decision-Making Process

Decisions within the GST Council are made during meetings by a majority vote of not less than three-fourths of the weighted votes of the members present and voting. The voting weightage is as follows:

- Central Government: One-third of the total votes cast.

- State Governments: Two-thirds of the total votes cast.

Supreme Court Judgment (May 2022)

The Supreme Court's judgment in May 2022 clarified several important points regarding the GST Council and its recommendations:

- Nature of Recommendations: The recommendations made by the GST Council are not binding on the Union and State governments. They are advisory in nature.

- Legislative Power: Both the Parliament and State Legislatures have simultaneous power to legislate on GST matters.

- Binding Nature: The recommendations of the GST Council are binding on the government for secondary or subordinate legislations, such as changes in tax rates or framing rules under CGST, SGST, and IGST. However, for primary legislations, such as amendments to the CGST or SGST Acts, the recommendations carry only persuasive value.

Example to Understand GST

To illustrate the concept of GST, let's consider an example involving two businesses, A and B, and their value additions, sales, and GST payments:

1. Business A

- Value Addition: Rs. 100

- Cost of Inputs: Rs. 0

- Sale Price: Rs. 100

- GST (18%): Rs. 18

- Invoice to Business B: Rs. 118

2. Business B

- Value Addition: Rs. 200

- Cost of Inputs: Rs. 118 (Invoice from A)

- Sale Price: Rs. 300

- GST (18%): Rs. 54

- Invoice to Customers: Rs. 354

In this example:

- Business A adds value by producing goods worth Rs. 100 and sells them to Business B for Rs. 118, charging Rs. 18 GST.

- Business B further adds value by processing the goods and selling them for Rs. 354, charging Rs. 54 GST.

- The total GST paid to the government by Business B is Rs. 54. However, Business B can claim an Input Tax Credit (ITC) of Rs. 18 for the GST paid to Business A.

- This means that Business B effectively pays Rs. 36 (Rs. 54 - Rs. 18) to the government.

- The Input Tax Credit mechanism ensures that each entity in the value chain pays GST only on their value addition, avoiding double taxation.

1. Introduction (a) The Goods and Services Tax (GST) is a single tax that applies across India, with input tax credits available at each stage of production and distribution. This prevents the cascading effect of taxes, which was a problem under the previous Value Added Tax (VAT) system where input credit was only available within the same State. This feature is a fundamental advantage of GST.

2. Implementation Aspects

- When a transaction involves parties from different States, such as A in Uttar Pradesh (UP) and B in Bihar, the State Goods and Services Tax (SGST) is collected based on the location of the consumer. In this case, the SGST of Rs. 27 (Rs. 9 from A and Rs. 18 from B) is passed on to Bihar, the consuming State, while UP does not receive any SGST. This feature makes GST a consumption-based and destination-based tax.

- If both parties are in different States, the transaction is subject to Integrated Goods and Services Tax (IGST), which is equal to the sum of Central Goods and Services Tax (CGST) and SGST. IGST is collected by the Centre and then distributed equally between the Centre and the consuming State.

- In cases where goods are exported, IGST is imposed on the inter-State supply. However, the GST paid throughout the value chain and the IGST paid at the border are refunded or credited back to the suppliers, making exports effectively tax-free. This is why exports are referred to as "zero-rated" supplies. Supplies to Special Economic Zones (SEZs) also fall under zero-rated supplies.

- For imports, Customs Duty is levied first, followed by IGST, as imports are considered inter-State supplies.

3. Electronic Way Bill (E-Way Bill)

- The E-Way Bill is a document issued by a carrier providing details and instructions related to the shipment of goods. It includes information such as the names of the consignor and consignee, the point of origin, destination, and route of the consignment.

- E-Way Bills are mandatory for the transportation of goods valued over Rs. 50,000. This digital compliance mechanism allows the person responsible for the movement of goods to upload relevant information and generate an e-way bill on the GST portal before the commencement of goods movement.

- The E-Way Bill system ensures compliance with GST law, facilitates tracking of goods movement, and helps curb tax evasion. It replaces the physical Way Bill required under the VAT regime for the movement of goods.

Composition Levy

- Composition levy is a simplified tax option for small businesses with a turnover of up to Rs. 1.5 crore. It aims to reduce compliance costs and make tax payment easier for these businesses. Under this scheme, eligible taxpayers can opt to pay a flat tax rate of 1% on their turnover instead of the regular GST rates. For small service providers with a turnover of Rs. 50 lakhs, the composition scheme allows them to pay GST at a rate of 6%.

- However, businesses under the composition scheme cannot claim input tax credit. It's important to note that this scheme is optional, and businesses can choose to pay the standard GST rate if they prefer.

GST Compensation Cess

- Before the implementation of GST, there were concerns that state tax revenues might decline and that states would lose the ability to impose additional taxes. To address these concerns, the Government of India analyzed the growth of state indirect tax revenues from 2012-13 to 2015-16 and found an average annual growth rate of 14%.

- The government promised states that if their indirect revenue growth fell below 14% annually starting from 2015-16, it would impose a cess on luxury and demerit goods to compensate for the shortfall. This compensation mechanism was established through the Goods and Services Tax (Compensation to States) Act 2017.

- The Centre collects the GST compensation cess, which is deposited into the Consolidated Fund of India. From there, it is transferred to the GST Compensation Fund and then distributed to the states' Consolidated Funds.

- Initially, this system worked well, but during the COVID-19 pandemic, the revenue shortfall increased significantly. Since it was not feasible to raise the cess on luxury and demerit goods to cover the shortfall, the Centre decided to borrow the additional shortfall amount and lend it to the states on a back-to-back basis. States are expected to repay the principal and interest amounts in the future, as the Centre's borrowing costs are lower due to its better credit rating and lower default risk.

- To repay the principal and interest amount, a cess will be imposed from 1st July 2022 to 31st March 2026. Initially, states wanted the cess to continue for 5 years, but the Centre agreed only for the repayment of the loan taken due to the Covid crisis.

- GST simplifies the tax system from a complex, multi-layered one to a unified tax system for both goods and services, enabling tax set-off across the value chain. This will lower product costs, enhance competitiveness against imports, and boost company profitability. It creates a unified national market with common rules and administration, widening the tax base and simplifying procedures for clarity and transparency.

Benefits of GST

For businesses and industry

- Easy compliance: GST is supported by a robust IT system, making online services like registrations, returns, and payments easy and transparent. Unlike the pre-GST era, where separate returns were needed for VAT and Central Excise, GST requires only one return.

- Uniform tax rates: GST has standardised indirect tax rates and structures across the country, reducing compliance costs and making business operations more predictable. Previously, different excise and state VAT rates applied, but now there are only six rates, simplifying the structure.

- Removal of cascading: GST allows seamless tax credits throughout the value chain and across state boundaries, eliminating tax cascading. This enhances competitiveness for trade and industry.

For Manufacturers and Exporters

- Cost Reduction: GST has merged major Central and State taxes, allowing for a complete set-off of taxes on input goods and services. This has lowered the cost of locally produced goods and services.

- Increased Competitiveness: The reduction in costs has made Indian goods and services more competitive in the international market.

- Boost to Exports: With enhanced competitiveness, Indian exports have received a significant boost.

For Central and State Governments

- Cooperative Federalism: GST promotes cooperative federalism by ensuring that domestic indirect tax decisions are made jointly by the Centre and the states.

- Simplified Administration: Multiple indirect taxes at both the Central and State levels have been consolidated into one GST. This, supported by a robust IT system, makes GST simpler and easier to administer compared to previous indirect taxes.

- Reduced Compliance Scrutiny: The elimination of inter-state check posts (Entry Tax) under GST has reduced compliance scrutiny for the movement of goods between states, addressing a major concern for businesses.

- Better Controls and Reduced Corruption: GST's self-policing nature, through invoice matching for input tax credit claims, enhances compliance and reduces non-compliance. This system was previously limited to intra-state VAT transactions.

- Increased Tax Compliance: The robust IT infrastructure of GST has improved tax compliance. The seamless transfer of input tax credit throughout the value chain incentivizes tax compliance among traders.

- Expanded Tax Base: The inclusion of new agents who were previously outside the tax net has expanded the tax base and increased tax buoyancy.

- Higher Revenue Efficiency: GST has lowered the cost of tax revenue collection for the Government, leading to higher revenue efficiency.

For the Consumer

- Single and Transparent Tax: Before GST, goods and services were burdened with multiple indirect taxes from both the Centre and State, often without proper input tax credits at various stages of value addition. This made the cost of most goods and services opaque due to hidden taxes.

- Under the GST regime, there is only one tax applied from the manufacturer to the consumer, ensuring transparency in the taxes paid to the final consumer.

- Relief in Overall Tax Burden: GST has led to efficiency gains, prevention of leakages, and the removal of the cascading effect, resulting in a reduced overall tax burden on most commodities, benefiting consumers.

GST and Industry Formalization

- The GST regime is effective in formalizing sectors where India's formal industry interacts with the informal sector, thanks to its input tax credit mechanisms.

- Large companies in various industries are incentivized to bring their informal supply chains into the formal tax system to benefit from input tax credits.

Example - Textiles and Clothing:

- Historically, the textiles and clothing sector paid minimal tax (in the form of duty or VAT). With GST, there is now a formal GST rate, compelling businesses in this sector to register, formalize, and digitize their operations.

- Previously, parts of the value chain, particularly fabrics, were outside the tax net, leading to informalization and tax evasion. Under GST, the entire textile and clothing sector is now part of the tax net.

Impact on Small Manufacturers:

- Before GST, the exemption threshold for many small manufacturers was Rs 1.5 crore. Under GST, this threshold is Rs 40 lakhs.

- As a result, thousands of previously informal or unorganized MSMEs (Micro, Small, and Medium Enterprises) have registered for GST and come into the tax net.

- GST has thus brought informal enterprises into the formal economy, curbing tax evasion practices and expanding India's tax base.

Challenges Faced by GST

- Complicated Tax Structure: The GST council has established a complex tax structure with multiple rates: 5%, 12%, 18%, and 28%, along with exempt categories (0%) and specific rates for gold (3%). This creates a complicated system with effectively six or seven tax slabs.

- Exclusions from GST: Certain essential sectors like alcohol, petroleum, energy products, electricity, land, and real estate are excluded from the GST base. These are taxed separately by the Centre and states outside the GST framework. For instance, excluding electricity from GST harms the competitiveness of Indian industries, as taxes on power are embedded in manufacturing costs and cannot be claimed back as input tax credits.

- Revenue Principle Contradiction: The current GST regime contradicts the principle of increasing revenue through lower tax rates. A more effective taxation system would involve taxing more items at lower rates, which the new GST regime fails to achieve.

- GST Threshold Limit Issues: The GST threshold limit, which exempts businesses with a turnover under 40 lakhs per year from registration, is exploited by various business units to underreport sales figures. This creates disparities and undermines the integrity of the system.

- Impact on Informal Sector: There are over six crore firms in India's informal sector, with 2.5 crore small businesses exempt from GST due to the turnover threshold. However, the remaining four crore firms lack digital infrastructure and literacy, facing increased operating costs to comply with the new GST regime. This makes some businesses unviable, especially with the heavy filing requirements for service providers under GST.

- Inverted Duty Structure: The inverted duty structure is a significant issue where the GST rate on raw materials is higher than the rate on finished products. For example, if a product sold by A to B has a higher GST rate (18%) than the product sold by B to the consumer (12%), it creates an inverted duty structure. Ideally, raw materials should have lower tax rates, and finished products should have higher tax rates to avoid this issue.

- Remission of Duties or Taxes on Exported Products (RoDTEP): Before GST, customs duties on inputs required for manufacturing exported products were refunded through the Merchandise Export of India Scheme (MEIS) by providing Duty Credit Scrips to exporters. This system allowed exporters to adjust their customs duties on imported raw materials using these scrips based on a percentage of the export value. For instance, exporting goods worth Rs. 100 crores would earn the exporter a Duty Credit Scrip worth Rs. 2 crores (a certain percentage of the export value), which could be used to pay customs duties on imported raw materials.

- Initially, there were exemptions on domestic taxes for exports. However, the World Trade Organization (WTO) deemed the Merchandise Exports from India Scheme (MEIS) as non-compliant with WTO trade rules. This led to the replacement of MEIS with the Remission of Duties or Taxes on Exported Products (RoDTEP) in 2020.

- Under the Goods and Services Tax (GST) regime, the government exempts GST/IGST on exports, a process known as "zero-rated exports." In this process, exporters initially pay GST/IGST to the government and later provide proof of export, leading to a full reimbursement of the tax. This effectively means there is no tax on exports.

- However, certain products are excluded from GST, and the taxes, duties, and levies imposed on these products are not refunded for exports even under the current GST regime. These include VAT on fuel used for transportation, Mandi tax, and taxes on electricity and petroleum products, which are embedded in the product price.

- Under the new RoDTEP scheme, which became effective on January 1, 2021, these taxes will be refunded to exporters in their ledger accounts with Customs. The credits received can be used to pay basic customs duty on imported goods and raw materials. The RoDTEP scheme is applicable to all types of exports.

Direct Tax Reforms

Overview of Direct Taxpayers

- There are approximately 7.5 crore direct taxpayers in India.

- These taxpayers are responsible for paying taxes and filing tax returns.

- Some taxpayers use various methods to evade taxes and report their income significantly lower than their actual income.

Government's Response

- To address this issue, the government has established specific parameters to identify cases for assessment and review.

- For instance, taxpayers with high incomes (e.g., ₹30 lakhs) but low tax payments (e.g., ₹2 lakhs) or those with substantial deposits in savings accounts (e.g., over ₹10 lakhs in a financial year) may trigger scrutiny.

- If there are 5 lakh such cases, the government might randomly select 50,000 cases for review due to resource constraints.

- Taxpayers receiving such notices must provide clarifications, and if discrepancies are found, penalties may be imposed.

1. Faceless Assessment

- Previously, tax officials selected cases for assessment, leading to face-to-face meetings that often involved harassment of taxpayers.

- With the introduction of the e-assessment scheme, cases are now randomly picked by computer, eliminating face-to-face interactions.

- Assessments are conducted through electronic communication, enhancing transparency, efficiency, and governance.

2. Faceless Appeal

- Faceless appeal refers to the process of challenging a tax assessment without direct interaction with tax officials.

- Appeals are randomly assigned to officers across the country, and the identity of the officer remains unknown to the taxpayer.

- Taxpayers are not required to visit income tax offices, and decisions are made by a team and reviewed collectively.

- The Income Tax Act 1961 has been amended to incorporate faceless assessment and appeal processes.

3. Taxpayers' Charter

- The Taxpayers' Charter is a mutual document outlining the commitments of the government to taxpayers and vice versa.

- The government promises fair and courteous treatment, considering taxpayers as honest, providing mechanisms for appeal and review, ensuring privacy and confidentiality, and collecting the correct amount of tax.

- Taxpayers are also given the right to choose their representatives and hold authorities accountable.

The Taxpayers' Charter outlines the government's commitments to taxpayers, including:

- Providing a mechanism for lodging complaints and ensuring a fair and just system.

- Publishing service standards and reporting on them periodically.

- Reducing the cost of compliance for taxpayers.

It also emphasizes the obligations of taxpayers, which include:

- Being honest, informed, and compliant.

- Keeping accurate records.

- Knowing what your representative does on your behalf.

- Responding and paying on time.

Recent Developments

1. Income Tax Reforms

New Tax Regime as Default: The new tax regime under Section 115BAC is the default for individuals, HUFs, AOPs, and BOIs since FY 2024-25 (AY 2025-26). Taxpayers can opt for the old regime annually for non-business income or via Form 10-IEA for business income (one-time switch).

Revised Income Tax Slabs (FY 2025-26, AY 2026-27):

New Regime:

Up to ₹4 lakh: Nil

₹4-8 lakh: 5%

₹8-12 lakh: 10%

₹12-16 lakh: 15%

₹16-20 lakh: 20%

₹20-24 lakh: 25%

Above ₹24 lakh: 30%

Rebate under Section 87A increased to ₹60,000, making income up to ₹12 lakh tax-free (₹12.75 lakh with ₹75,000 standard deduction).

Old Regime: Unchanged, with basic exemption at ₹2.5 lakh (₹3 lakh for senior citizens, ₹5 lakh for super senior citizens). Rebate of ₹12,500 for income up to ₹5 lakh.

Standard Deduction and Rebates:

Standard deduction for salaried employees in the new regime raised to ₹75,000 from ₹50,000. Family pension deduction increased to ₹25,000 from ₹15,000.

NPS employer contribution deduction limit raised to 14% for FY 2024-25.

Income Tax Bill 2025: Tabled in Lok Sabha on February 13, 2025, to replace the Income Tax Act, 1961. Aims to simplify tax laws, remove obsolete provisions, and introduce a unified tax year from April 1, 2026. Includes presumptive taxation updates for businesses with turnover up to ₹30 million (95% online transactions).

TDS/TCS Changes:

TDS threshold for rent payments increased from ₹2.4 lakh to ₹6 lakh per annum.

TCS on Liberalised Remittance Scheme (LRS) raised to ₹10 lakh.

Simplified TDS/TCS for goods sales: 0.1% TDS on sales above ₹50 lakh, eliminating double taxation.

Updated Return Filing: Time limit for filing updated returns extended from 2 to 4 years, with additional taxes of 60% (third year) and 70% (fourth year).

2. Goods and Services Tax (GST) Reforms

Rate Rationalization: The 55th GST Council meeting (December 2024) proposed rationalizing rates and expanding Input Service Distributor (ISD) mechanisms for inter-state reverse charge supplies. Specific rate changes (e.g., on essential goods) may not be reflected in older documents.

Compliance Updates:

Mandatory ISD mechanism and Input Management System (IMS) effective April 1, 2025, impacting businesses' IT infrastructure.

Input Tax Credit (ITC) restrictions tightened post-Safari Retreats judgment, limiting credits for immovable property construction unless classified as plant and machinery.

Penalties and Appeals: New penalties under Sections 122B and 148A for track-and-trace violations. Pre-deposit for appeals against penalty-only orders set at 10%.

GST Tribunal: Establishment remains delayed, increasing litigation backlog, a key concern for UPSC's governance questions.

Revenue Trends: GST collections consistently above ₹2 lakh crore monthly in FY 2024-25, reflecting improved compliance and economic activity.

3. Corporate Tax Reforms

Foreign Company Tax Rate: Reduced from 40% to 35% for ordinary and business income from AY 2025-26.

Startup Incentives:

Three-year tax holiday for eligible startups within 10 years of incorporation.

Angel tax (Section 56(2)(viib)) abolished in Budget 2024, boosting startup investments UPSC Relevance: Understand the progressive nature of tax slabs, impact on middle-class consumption, startup ecosystem (removing barriers for startups), and simplification efforts. Questions may focus on tax relief measures or the new Income Tax Bill's implications for compliance.

Loss Carry Forward in Mergers: Losses can be carried forward only for remaining years post-merger, not reset, impacting M&A strategies.

Minimum Alternate Tax (MAT): Remains at 15% for companies not opting for Section 115BAA or 115BAB.

Transfer Pricing: Three-year consistency in transfer pricing for related-party transactions to reduce disputes.

4. Budget 2024 and 2025 Highlights

Budget 2024:

Capital Gains Tax: Unified long-term capital gains tax at 12.5% across asset classes, removing indexation benefits. Short-term gains on certain securities at 20%.

Equalisation Levy: 2% levy on non-resident e-commerce operators abolished from August 1, 2024, aligning with OECD BEPS framework.

Vivad se Vishwas 2.0: Expanded dispute resolution scheme to reduce litigation, covering more cases.

Customs Duty: Reduced on critical minerals and electronics to boost manufacturing under Make in India.

Budget 2025:

No income tax up to ₹12.75 lakh (new regime) to boost middle-class savings.

Senior citizens' TDS threshold for interest income doubled, reducing compliance for Form 15H.

New Income Tax Bill announced for simpler, transparent tax laws.

Focus on AI, startups, and MSMEs for economic growth.

5. Cryptocurrency Taxation

Legal Classification: Virtual Digital Assets (VDAs), including cryptocurrencies and NFTs, classified as "assets" under Income Tax Bill 2025, akin to property or shares. Subject to capital gains tax (short-term or long-term based on holding period).

Tax Rates: 30% tax on VDA income (introduced in 2022) continues, with 1% TDS on transfers. No change in Budget 2025, but stricter compliance proposed.

Regulatory Clarity: Enhanced scrutiny for crypto transactions to curb tax evasion, aligned with FATF guidelines.

6. Green Taxes and Environmental Taxation

Carbon Tax Discussions: No formal carbon tax introduced, but cess on coal and discussions on green taxes align with India's net-zero 2070 goal. Budget 2025 emphasized sustainable development, potentially via environmental levies.

Customs Duty Reductions: Lower duties on renewable energy components to support green energy transition.

Challenges: Balancing environmental goals with industrial growth remains a UPSC focus area.

7. BEPS Pillar Two and Global Taxation

Pillar Two Implementation: India adopted the OECD's 15% global minimum tax for MNCs (revenue > €750 million) from 2024, ensuring tax on profits in low-tax jurisdictions. Domestic law amendments proposed in Budget 2024.

Pillar One: India supports taxing digital giants based on market presence, with Equalisation Levy phased out to align with BEPS.

UN Advocacy: India pushes for equitable international tax frameworks under UN, challenging developed nations' dominance in BEPS.

8. Tax Administration and Compliance

Faceless Assessments: Fully implemented, with Jurisdictional Assessing Officers for specific cases. Faceless appeals expanded to Commissioner (Appeals) level.

Simplified Filing: GST and income tax filing streamlined, reducing compliance time. GST audits still take months, a governance challenge.

Digital Tools: Real-time GSTN analytics and e-invoicing (mandatory for turnover > ₹5 crore) enhance transparency.

9. Fiscal Federalism and Revenue Sharing

16th Finance Commission: Constituted in 2023, its report (due 2025) will guide tax devolution to states from FY 2026-27. Likely to address vertical and horizontal imbalances.

GST Compensation Cess: Extended beyond 2022 to clear dues, with potential restructuring by 2025.

Local Body Taxation: Property tax reforms under AMRUT 2.0 strengthen urban local bodies, a UPSC governance topic.

FAQs on Vivek Singh Summary: India’s Tax System

| 1. What is Goods and Services Tax (GST) in India and how does it work? |  |

| 2. What are the benefits of implementing GST in India? | |

| 3. How does GST impact small businesses in India? | |

| 4. What are the direct tax reforms that have been introduced in India? | |

| 5. How can taxpayers benefit from the digitalization of the tax system in India? | |