Cheat Sheet: Comptroller and Auditor General of India

Introduction

This chapter explains the role of the Comptroller and Auditor General (CAG) of India, a constitutional body under Article 148, described by Dr. B.R. Ambedkar as one of the most important officers in the Constitution. It covers the CAG's appointment, independence, duties, powers, role in auditing corporations, criticisms, and challenges, emphasizing its critical function in ensuring financial accountability and integrity in India's democratic system.

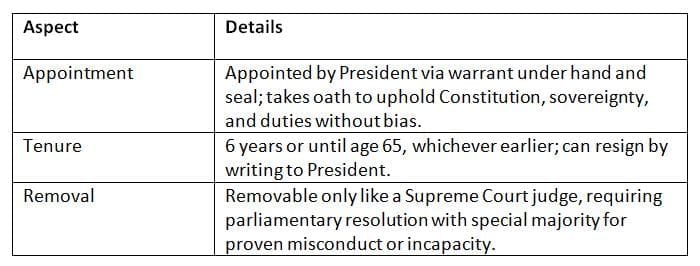

Appointment and Term of the Comptroller and Auditor General

The CAG is appointed by the President with a fixed term and strict removal process to ensure independence in overseeing public financial management. Key Points: The CAG's appointment and tenure ensure a stable, independent role, safeguarded by a rigorous removal process.

Key Points: The CAG's appointment and tenure ensure a stable, independent role, safeguarded by a rigorous removal process.

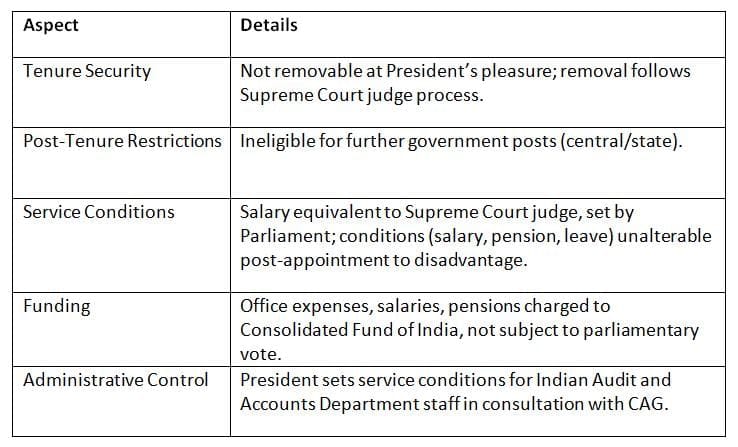

Independence of the Comptroller and Auditor General

The Constitution provides multiple measures to protect the CAG's independence, ensuring impartial oversight of public finances. Key Points: Constitutional safeguards ensure the CAG operates independently, free from executive influence, with secure funding and tenure.

Key Points: Constitutional safeguards ensure the CAG operates independently, free from executive influence, with secure funding and tenure.

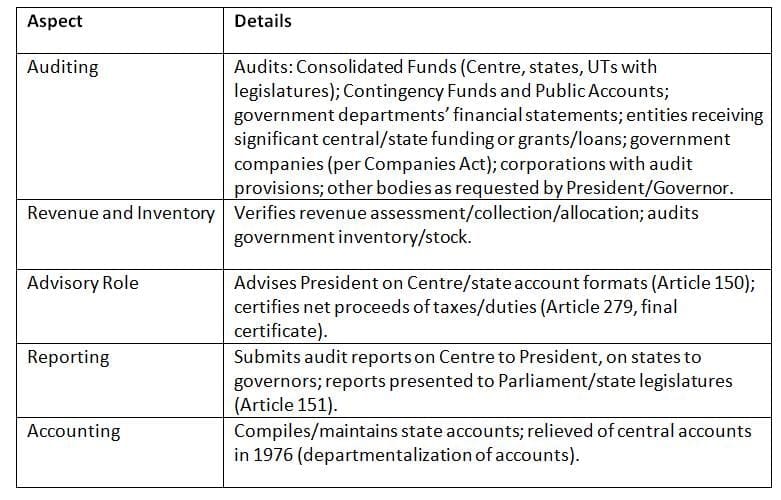

Duties and Powers of the Comptroller and Auditor General

The CAG's duties and powers, defined under Article 149 and the CAG's (Duties, Powers and Conditions of Service) Act, 1971, focus on auditing public finances and advising on accounting practices.

Key Points: The CAG's comprehensive auditing and advisory roles ensure financial transparency and compliance across government levels.

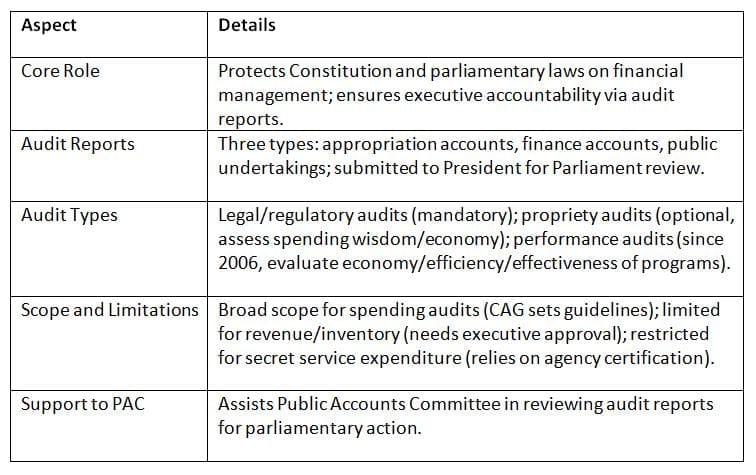

Role of the Comptroller and Auditor General

The CAG upholds constitutional and parliamentary financial laws, holding the executive accountable through detailed audit reports and supporting parliamentary oversight.

Key Points: The CAG's role ensures financial accountability through diverse audits, supporting democratic oversight, with performance audits enhancing program evaluation.

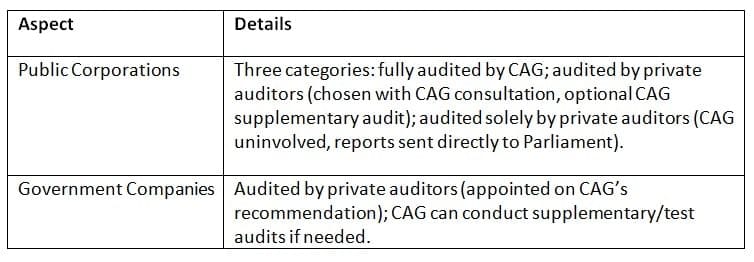

CAG and Corporations

The CAG's auditing role for public corporations and government companies is limited, with varying levels of involvement based on entity type.

Key Points: The CAG's limited role in corporate audits reflects a balance between public and private auditing, with flexibility for supplementary oversight.

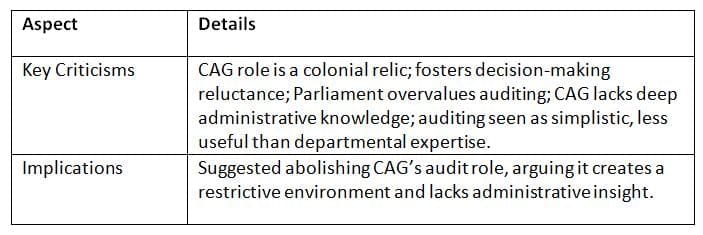

Appleby's Criticism

Paul H. Appleby's reports criticized the CAG's role, questioning its relevance and impact on administration.

Key Points: Appleby's critique viewed the CAG's role as outdated and overly restrictive, challenging its administrative significance.

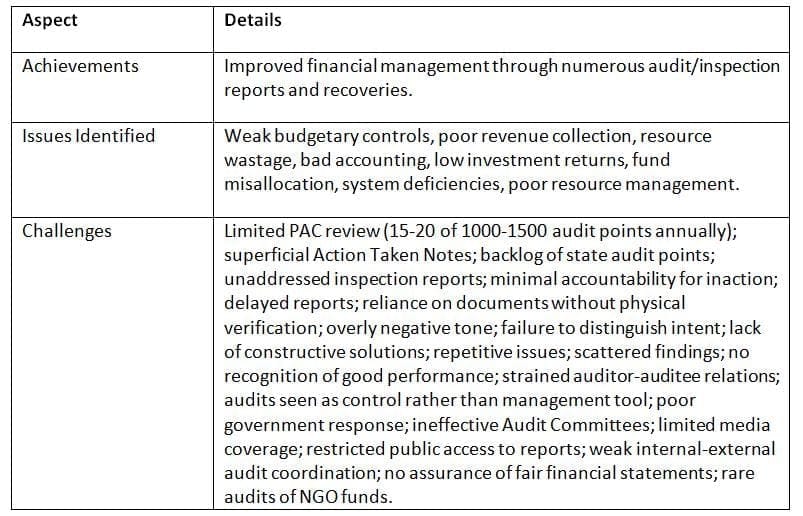

Challenges Faced by the CAG

The Second Administrative Reforms Commission (2005-2009) highlighted challenges limiting the CAG's audit effectiveness, despite its contributions to financial management.

Key Points: While the CAG improves financial management, its impact is limited by procedural, accountability, and perception challenges.

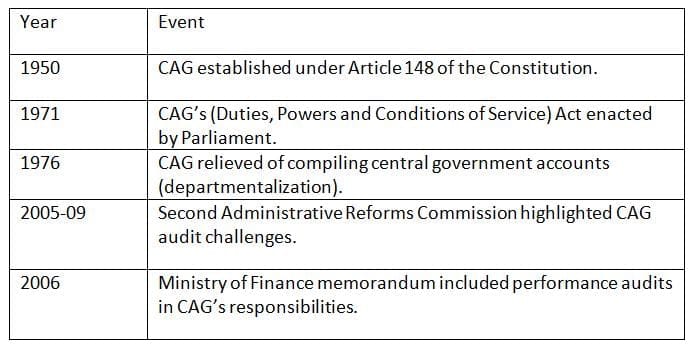

Chronology for Quick Revision

Conclusion

This chapter underscores the Comptroller and Auditor General's pivotal role as a constitutional guardian of India's public finances, as envisioned by Dr. B.R. Ambedkar. Established under Article 148, the CAG ensures financial accountability through audits, reporting, and advisory functions, supported by strong independence measures. Despite limitations in corporate audits, criticisms from Appleby, and challenges like delayed reports and poor government response, the CAG remains essential for democratic integrity. Addressing procedural and accountability issues can enhance its effectiveness, ensuring robust oversight of India's financial system and reinforcing public trust in governance.

FAQs on Cheat Sheet: Comptroller and Auditor General of India

| 1. What is the role of the Comptroller and Auditor General (CAG) in India? |  |

| 2. What are the key duties and powers of the Comptroller and Auditor General? | |

| 3. How does the independence of the Comptroller and Auditor General ensure effective auditing? | |

| 4. Can the Comptroller and Auditor General audit private corporations? | |

| 5. What is the term of office for the Comptroller and Auditor General of India? | |