Complete Chapter - Money and Credit, Class 10 SST PDF Download

MONEY AND CREDIT

Medium of Exchange:

Barter System: Before the advent of money, people used to follow the barter system of exchange. Suppose somebody has surplus vegetables and he needs wheat in lieu of that then he could find a person who has surplus wheat and needs vegetables.

Double Coincidence of wants:- The major feature or rather drawback of the barter system was the coincidence of wants. It used to be difficult to find a person who can fulfill the coincidence of wants. Moreover, it was impractical and difficult to carry heavy goods for barter. This restricted the economic activity.

Money

In the historical period coins of precious metals started getting used as medium of exchange and this was the birth of money. As precious metals were difficult to procure so slowly paper money or currency notes began to replace them. Now the government or government authorized body in a country issues currency notes for circulation.

In India, the Reserve Bank of India issues currency notes. On the currency note you can observe the statement promising a particular amount to be paid to the bearer of the currency note.

Money removed the coincidence of wants factor and smoothened exchange facilitating economic activity.

Other Forms of Money

Deposits with Banks:- The other form in which people hold money is as deposits with banks. At a point of time, people need only some currency for their day-to-day needs. Banks accept the deposits and also pay an interest rate on the deposits. In this way people’s money is safe with the banks and it earns an interest. People also have the provision to withdraw the money as and when they require. Since the deposits in the bank accounts can be withdrawn on demand, these deposits are called demand deposits.

The facility of cheques against demand deposits makes it possible to directly settle payments without the use of cash. Since demand deposits are accepted widely as a means of payment, along with currency, they constitute money in the modern economy.

Credit:- Banks keep only a small proportion of their deposits as cash with themselves. For example, banks in India these days hold about 15 per cent of their deposits as cash. This is kept as provision to pay the depositors who might come to withdraw money from the bank on any given day. Since, on any particular day, only some of its many depositors come to withdraw cash, the bank is able to manage with this cash. Banks use the major portion of the deposits to extend loans. There is a huge demand for loans for various economic activities.

Banks make use of the deposits to meet the loan requirements of the people. In this way, banks mediate between those who have surplus funds (the depositors) and those who are in need of these funds (the borrowers). Banks charge a higher interest rate on loans than what they offer on deposits. The difference between what is charged from borrowers and what is paid to depositors is their main source of income.

A large number of transactions in our day-to-day activities involve credit in some form or the other. Credit (loan) refers to an agreement in which the lender supplies the borrower with money, goods or services in return for the promise of future payment.

TERMS OF CREDIT-

Every loan agreement specifies an interest rate which the borrower must pay to the lender along with the In rural areas, the main demand for credit is for crop production. Crop production involves considerable costs on seeds, fertilisers, pesticides, water, electricity, repair of equipment, etc. There is a minimum stretch of three to four months between the time when the farmers buy these inputs and when they sell the crop. Farmers usually take crop loans at the beginning of the season and repay the loan after harvest. Repayment of the loan is crucially dependent on the income from farming.

Collateral: Collateral is an asset that the borrower owns (such as land, building, vehicle, livestocks, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid. If the borrower fails to repay the loan, the lender has the right to sell the asset or collateral to obtain payment. Property such as land titles, deposits with banks, livestock are some common examples of collateral used for borrowing.

Terms of Credit:- Interest rate, collateral and documentation requirement, and the mode of repayment together comprise what is called the terms of credit. The terms of credit vary substantially from one credit arrangement to another. They may vary depending on the nature of the lender and the borrower.

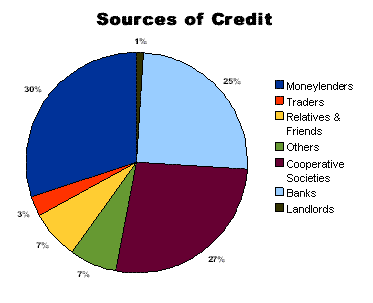

Sources of Credit

Formal Sector:- The formal Sector comprises of banks and cooperative societies.

Informal Sector:- The informal sector consists of money lenders and friends and relatives, merchants and landlords.

The following diagram shows share of different sources of credit in rural households in India in 2003.

The RBI sees that the banks give loans not just to profit-making businesses and traders but also to small cultivators, small scale industries, to small borrowers etc. Periodically, banks have to submit information to the RBI on how much they are lending, to whom, at what interest rate, etc.

There is no organisation which supervises the credit activities of lenders in the informal sector. Compared to the formal lenders, most of the informal lenders charge a much higher interest on loans. Thus, the cost to the borrower of informal loans is much higher. Higher cost of borrowing means a larger part of the earnings of the borrowers is used to repay the loan. In certain cases, the high interest rate of borrowing can mean that the amount to be repaid is greater than the income of the borrower. This could lead to increasing debt and debt trap. Also, people who might wish to start an enterprise by borrowing may not do so because of the high cost of borrowing.

For these reasons, banks and cooperative societies need to lend more. This would lead to higher incomes and many people could then borrow cheaply for a variety of needs. They could grow crops, do business, set up small-scale industries etc. They could set up new industries or trade in goods.

Self Help Groups

In recent years, people have tried out some newer ways of providing loans to the poor. The idea is to organise rural poor, in particular women, into small Self Help Groups (SHGs) and pool (collect) their savings. A typical SHG has 15-20 members, usually belonging to one neighbourhood, who meet and save regularly. Saving per member varies from Rs 25 to Rs 100 or more, depending on the ability of the people to save. Members can take small loans from the group itself to meet their needs. The group charges interest on these loans but this is still less than what the moneylender charges. After a year or two, if the group is regular in savings, it becomes eligible for availing loan from the bank. Loan is sanctioned in the name of the group and is meant to create self employment opportunities for the members.

Most of the important decisions regarding the savings and loan activities are taken by the group members. The group decides as regards the loans to be granted — the purpose, amount, interest to be charged, repayment schedule etc. Also, it is the group which is responsible for the repayment of the loan. Any case of non repayment of loan by any one member is followed up seriously by other members in the group. Because of this feature, banks are willing to lend to the poor women when organised in SHGs, even though they have no collateral as such.

Thus, the SHGs help borrowers overcome the problem of lack of collateral. They can get timely loans for a variety of purposes and at a reasonable interest rate. Moreover, SHGs are the building blocks of organisation of the rural poor. Not only does it help women to become financially self-reliant, the regular meetings of the group provide a platform to discuss and act on a variety of social issues such as health, nutrition, domestic violence, etc.

FAQs on Complete Chapter - Money and Credit, Class 10 SST

| 1. What is the meaning of money and credit? |  |

| 2. How does money solve the problem of double coincidence of wants? | |

| 3. What are the different types of credit? | |

| 4. What are the advantages and disadvantages of credit? | |

| 5. How does credit contribute to economic growth? | |

video lectures

,past year papers

,Class 10 SST

,Complete Chapter - Money and Credit

,Free

,Complete Chapter - Money and Credit

,ppt

,Exam

,MCQs

,Complete Chapter - Money and Credit

,Semester Notes

,mock tests for examination

,study material

,Class 10 SST

,Summary

,Previous Year Questions with Solutions

,Important questions

,Objective type Questions

,Viva Questions

,Sample Paper

,practice quizzes

,Class 10 SST

,shortcuts and tricks

,Extra Questions

;

Complete Chapter - Money and Credit, Class 10 SST Free PDF Download

Importance of Complete Chapter - Money and Credit, Class 10 SST

Complete Chapter - Money and Credit, Class 10 SST Notes

Complete Chapter - Money and Credit, Class 10 SST Class 10 Questions

Study Complete Chapter - Money and Credit, Class 10 SST on the App

|

© EduRev

|

Education Revolution

|

|