All Exams >

CA Foundation >

Accounting for CA Foundation >

All Questions

All questions of Unit 5: Death of a Partner for CA Foundation Exam

A, B and C are partners sharing profits and losses in the ratio 2:2:1. C dies on 31st March 2007. The profits of the financial year ending 31st March 2007 is Rs. 64,000. The share of the deceased partner in the profits will be: - a)Rs. 9,200

- b)Rs. 12,800

- c)Rs. 3,100

- d)Rs. 6,100

Correct answer is option 'B'. Can you explain this answer?

A, B and C are partners sharing profits and losses in the ratio 2:2:1. C dies on 31st March 2007. The profits of the financial year ending 31st March 2007 is Rs. 64,000. The share of the deceased partner in the profits will be:

a)

Rs. 9,200

b)

Rs. 12,800

c)

Rs. 3,100

d)

Rs. 6,100

|

Srestha Shah answered |

Given data:

- A, B and C are partners sharing profits and losses in the ratio 2:2:1.

- C dies on 31st March 2007.

- The profits of the financial year ending 31st March 2007 is Rs. 64,000.

To find: The share of the deceased partner in the profits.

Solution:

Step 1: Calculate the total profit for the year

Total profit = Rs. 64,000

Step 2: Calculate the share of A and B in the profit

Ratio of A and B's share = 2:2 = 4

Total share of A and B = 4+1 = 5

Share of A = (4/5) * Total profit = (4/5) * Rs. 64,000 = Rs. 51,200

Share of B = (4/5) * Total profit = (4/5) * Rs. 64,000 = Rs. 51,200

Step 3: Calculate the share of C in the profit till his death

As C died on 31st March 2007, his share in the profit will be from 1st April 2006 to 31st March 2007.

Let's assume the year's profit is divided equally into 12 months.

So, C's share in the profit for the year = (1/12) * (1/5) * Total profit = (1/60) * Rs. 64,000 = Rs. 1,066.67

Step 4: Calculate the share of C's legal heir in the profit

As C died, his legal heir will get his share in the profit. As per the Indian Partnership Act, 1932, the legal heir of a deceased partner is entitled to the deceased partner's share in the profits from the date of the last agreed balance sheet till the date of the deceased partner's death.

Here, we are not given the date of the last agreed balance sheet. So, we assume that it is 31st March 2006, i.e. one year before the death of C.

So, C's legal heir's share in the profit = (1/12) * (1/5) * Total profit = (1/60) * Rs. 64,000 = Rs. 1,066.67

Step 5: Calculate the total share of C's legal heir in the profit

Total share of C's legal heir = (C's share till death) + (C's legal heir's share) = Rs. 1,066.67 + Rs. 1,066.67 = Rs. 2,133.34

Therefore, the share of the deceased partner in the profits is Rs. 2,133.34, which is option (B).

- A, B and C are partners sharing profits and losses in the ratio 2:2:1.

- C dies on 31st March 2007.

- The profits of the financial year ending 31st March 2007 is Rs. 64,000.

To find: The share of the deceased partner in the profits.

Solution:

Step 1: Calculate the total profit for the year

Total profit = Rs. 64,000

Step 2: Calculate the share of A and B in the profit

Ratio of A and B's share = 2:2 = 4

Total share of A and B = 4+1 = 5

Share of A = (4/5) * Total profit = (4/5) * Rs. 64,000 = Rs. 51,200

Share of B = (4/5) * Total profit = (4/5) * Rs. 64,000 = Rs. 51,200

Step 3: Calculate the share of C in the profit till his death

As C died on 31st March 2007, his share in the profit will be from 1st April 2006 to 31st March 2007.

Let's assume the year's profit is divided equally into 12 months.

So, C's share in the profit for the year = (1/12) * (1/5) * Total profit = (1/60) * Rs. 64,000 = Rs. 1,066.67

Step 4: Calculate the share of C's legal heir in the profit

As C died, his legal heir will get his share in the profit. As per the Indian Partnership Act, 1932, the legal heir of a deceased partner is entitled to the deceased partner's share in the profits from the date of the last agreed balance sheet till the date of the deceased partner's death.

Here, we are not given the date of the last agreed balance sheet. So, we assume that it is 31st March 2006, i.e. one year before the death of C.

So, C's legal heir's share in the profit = (1/12) * (1/5) * Total profit = (1/60) * Rs. 64,000 = Rs. 1,066.67

Step 5: Calculate the total share of C's legal heir in the profit

Total share of C's legal heir = (C's share till death) + (C's legal heir's share) = Rs. 1,066.67 + Rs. 1,066.67 = Rs. 2,133.34

Therefore, the share of the deceased partner in the profits is Rs. 2,133.34, which is option (B).

In the absence of proper agreement, representative of the diseased partner is entitled to the Dead partner’s share in the following items.- a)Profits till date, goodwill, joint life policy, share in revalued assets and liabilities.

- b)Capital, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities

- c)Capital, profits till date, goodwill, interest on capital, share in revalued assets and liabilities

- d)Capital, profits till date, goodwill, joint life policy, share in revalued assets and liabilities

Correct answer is option 'D'. Can you explain this answer?

In the absence of proper agreement, representative of the diseased partner is entitled to the Dead partner’s share in the following items.

a)

Profits till date, goodwill, joint life policy, share in revalued assets and liabilities.

b)

Capital, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities

c)

Capital, profits till date, goodwill, interest on capital, share in revalued assets and liabilities

d)

Capital, profits till date, goodwill, joint life policy, share in revalued assets and liabilities

|

|

Asmit Sharma answered |

Isme smjhna kya hai ???

A, B and C are partners sharing profits and losses in the ratio 9:4:3. They took joint life policy of Rs. 25,000 for A, Rs. 20,000 for B and Rs. 51,000 for C. what is the share of C in the JLP amount?- a)Rs. 18,000

- b)Rs. 25,000

- c)Rs. 51,000

- d)Rs. 20,000

Correct answer is option 'C'. Can you explain this answer?

A, B and C are partners sharing profits and losses in the ratio 9:4:3. They took joint life policy of Rs. 25,000 for A, Rs. 20,000 for B and Rs. 51,000 for C. what is the share of C in the JLP amount?

a)

Rs. 18,000

b)

Rs. 25,000

c)

Rs. 51,000

d)

Rs. 20,000

|

|

Snehal Das answered |

Given, A:B:C = 9:4:3 and the joint life policy amounts are Rs. 25,000, Rs. 20,000 and Rs. 51,000 respectively.

To find the share of C in the JLP amount, we need to calculate the total JLP amount and then find the share of C in it.

Total JLP amount = Rs. 25,000 + Rs. 20,000 + Rs. 51,000 = Rs. 96,000

Now, we need to find the share of each partner in the JLP amount based on their profit sharing ratio.

Share of A = (9/16) x Rs. 96,000 = Rs. 54,000

Share of B = (4/16) x Rs. 96,000 = Rs. 24,000

Share of C = (3/16) x Rs. 96,000 = Rs. 18,000

Therefore, the share of C in the JLP amount is Rs. 18,000. Hence, option C is the correct answer.

To find the share of C in the JLP amount, we need to calculate the total JLP amount and then find the share of C in it.

Total JLP amount = Rs. 25,000 + Rs. 20,000 + Rs. 51,000 = Rs. 96,000

Now, we need to find the share of each partner in the JLP amount based on their profit sharing ratio.

Share of A = (9/16) x Rs. 96,000 = Rs. 54,000

Share of B = (4/16) x Rs. 96,000 = Rs. 24,000

Share of C = (3/16) x Rs. 96,000 = Rs. 18,000

Therefore, the share of C in the JLP amount is Rs. 18,000. Hence, option C is the correct answer.

The balance of joint life policy account as shown in the balance sheet represents: - a)Surrender value of a policy

- b)Annual premium of JLP

- c)Total premium paid by the firm

- d)Amount receivable on the maturity of the policy

Correct answer is option 'A'. Can you explain this answer?

The balance of joint life policy account as shown in the balance sheet represents:

a)

Surrender value of a policy

b)

Annual premium of JLP

c)

Total premium paid by the firm

d)

Amount receivable on the maturity of the policy

|

|

Snehal Das answered |

Balance of joint life policy account represents surrender value of a policy

Explanation:

Joint life policy is an insurance policy that covers the lives of two individuals. The policy pays out on the death of the first person, and then ceases to exist. The balance of joint life policy account as shown in the balance sheet represents the surrender value of a policy.

Surrender value is the amount payable to the policyholder when the policy is surrendered before maturity. Surrendering a policy means terminating the policy prematurely and receiving the cash value of the policy. The surrender value is calculated based on the premiums paid and the duration of the policy.

The balance of joint life policy account represents the amount of money that the insurance company has set aside to pay out the surrender value of the policy. This amount is included in the balance sheet as an asset of the company.

The other options listed in the question, such as annual premium, total premium paid by the firm, and amount receivable on the maturity of the policy, are not relevant to the balance of joint life policy account. The balance of joint life policy account only represents the surrender value of the policy.

In summary, the balance of joint life policy account as shown in the balance sheet represents the amount of money set aside by the insurance company to pay out the surrender value of a joint life policy.

Explanation:

Joint life policy is an insurance policy that covers the lives of two individuals. The policy pays out on the death of the first person, and then ceases to exist. The balance of joint life policy account as shown in the balance sheet represents the surrender value of a policy.

Surrender value is the amount payable to the policyholder when the policy is surrendered before maturity. Surrendering a policy means terminating the policy prematurely and receiving the cash value of the policy. The surrender value is calculated based on the premiums paid and the duration of the policy.

The balance of joint life policy account represents the amount of money that the insurance company has set aside to pay out the surrender value of the policy. This amount is included in the balance sheet as an asset of the company.

The other options listed in the question, such as annual premium, total premium paid by the firm, and amount receivable on the maturity of the policy, are not relevant to the balance of joint life policy account. The balance of joint life policy account only represents the surrender value of the policy.

In summary, the balance of joint life policy account as shown in the balance sheet represents the amount of money set aside by the insurance company to pay out the surrender value of a joint life policy.

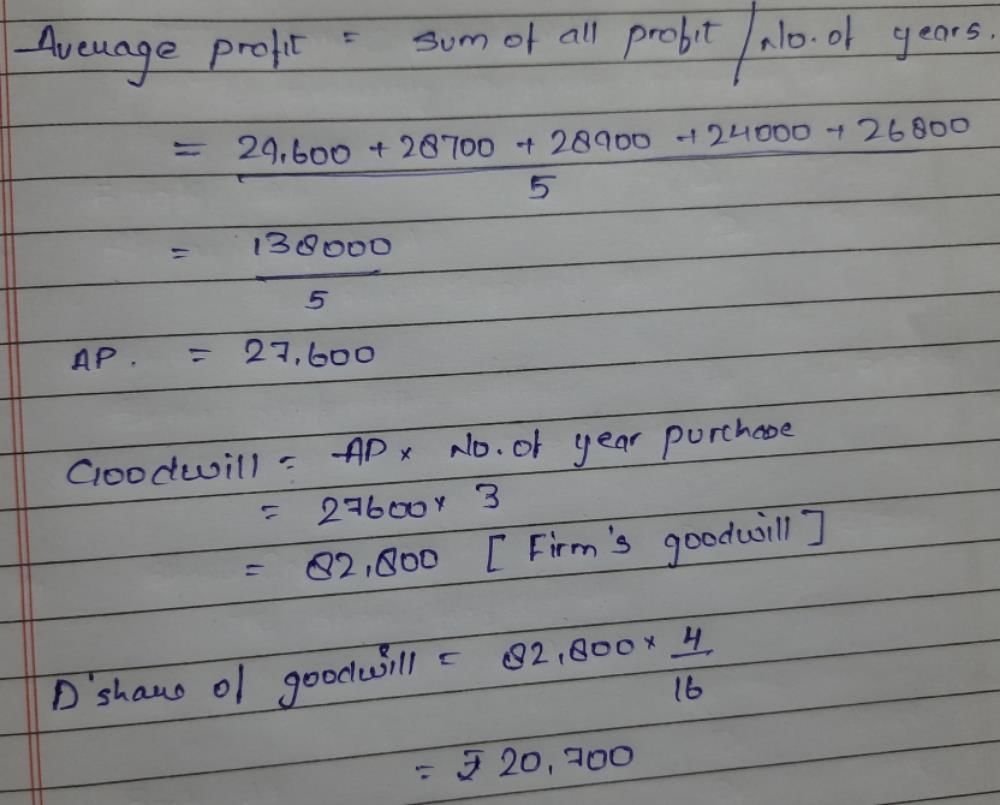

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006. It was decided to value the goodwill on the basis of three year’s purchase of last five years average profits. If the profits are Rs. 29,600; Rs. 28,700; Rs. 28,900; Rs. 24,000 and Rs. 26,800. What will be D’s share of goodwill?- a)Rs. 20,700.

- b)Rs. 27,600.

- c)Rs. 82,800.

- d)Rs. 27,000.

Correct answer is option 'A'. Can you explain this answer?

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006. It was decided to value the goodwill on the basis of three year’s purchase of last five years average profits. If the profits are Rs. 29,600; Rs. 28,700; Rs. 28,900; Rs. 24,000 and Rs. 26,800. What will be D’s share of goodwill?

a)

Rs. 20,700.

b)

Rs. 27,600.

c)

Rs. 82,800.

d)

Rs. 27,000.

|

Shrish Jaiswal answered |

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006. It was decided to value the goodwill on the basis of three year’s purchase of last five years average profits. If the profits are Rs. 29,600; Rs. 28,700; Rs. 28,900; Rs. 24,000 and Rs. 26,800. What will be D’s share of goodwill?- a)Rs. 20,700

- b)Rs. 27,600

- c)Rs. 82,800

- d)Rs. 27,000

Correct answer is option 'A'. Can you explain this answer?

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006. It was decided to value the goodwill on the basis of three year’s purchase of last five years average profits. If the profits are Rs. 29,600; Rs. 28,700; Rs. 28,900; Rs. 24,000 and Rs. 26,800. What will be D’s share of goodwill?

a)

Rs. 20,700

b)

Rs. 27,600

c)

Rs. 82,800

d)

Rs. 27,000

|

Tarun Chaudhary answered |

(29600+28700+28900+24000+26800) /5=27600

goodwill on the basis of 3 year purchase=27600×3=82800.

D's share of goodwill = (82800×4) /16=20700.

goodwill on the basis of 3 year purchase=27600×3=82800.

D's share of goodwill = (82800×4) /16=20700.

On death of a partner, his executor is paid the share of profits of the dying partner for the relevant period. This payment is recorded in Profit & Loss ……… Account.- a)Adjustment.

- b)Appropriation.

- c)Suspense.

- d)Reserve.

Correct answer is option 'C'. Can you explain this answer?

On death of a partner, his executor is paid the share of profits of the dying partner for the relevant period. This payment is recorded in Profit & Loss ……… Account.

a)

Adjustment.

b)

Appropriation.

c)

Suspense.

d)

Reserve.

|

Sounak Jain answered |

On death of a partner, his executor is paid the share of profits of the dying partner for the relevant period. This payment is recorded in Profit & Loss Account.

Explanation:

Explanation:

A, B and C are the partners sharing profits and losses in the ratio 2:1:1. Firm has a joint life policy of Rs. 1,20,000 and in the balance sheet it is appearing at the surrender value i.e. Rs. 20,000. On the death of A, how this JLP will be shared among the partners.- a)50,000:25,000:25,000.

- b)60,000:30,000:30,000.

- c)40,000:35,000:25,000.

- d)Whole of Rs. 1,20,000 will be paid to A.

Correct answer is option 'A'. Can you explain this answer?

A, B and C are the partners sharing profits and losses in the ratio 2:1:1. Firm has a joint life policy of Rs. 1,20,000 and in the balance sheet it is appearing at the surrender value i.e. Rs. 20,000. On the death of A, how this JLP will be shared among the partners.

a)

50,000:25,000:25,000.

b)

60,000:30,000:30,000.

c)

40,000:35,000:25,000.

d)

Whole of Rs. 1,20,000 will be paid to A.

|

|

Mahesh Chakraborty answered |

Calculation of JLP Share on Death of A

Partnership Ratio: 2:1:1

Total Ratio: 4

JLP amount: Rs. 1,20,000

Surrender Value: Rs. 20,000

Step 1: Calculation of JLP Share

Total JLP Share = JLP amount - Surrender Value

Total JLP Share = Rs. 1,20,000 - Rs. 20,000

Total JLP Share = Rs. 1,00,000

A's share = 2/4 x Total JLP Share

A's share = 1/2 x Rs. 1,00,000

A's share = Rs. 50,000

B's share = 1/4 x Total JLP Share

B's share = 1/4 x Rs. 1,00,000

B's share = Rs. 25,000

C's share = 1/4 x Total JLP Share

C's share = 1/4 x Rs. 1,00,000

C's share = Rs. 25,000

Step 2: Sharing of JLP Share on Death of A

A's share will be given to his legal heirs.

Remaining JLP share will be shared among the partners in their profit sharing ratio.

Share of B and C = Total JLP Share - A's share

Share of B and C = Rs. 1,00,000 - Rs. 50,000

Share of B and C = Rs. 50,000

B's share = B's profit sharing ratio x Share of B and C

B's share = 1/4 x Rs. 50,000

B's share = Rs. 12,500

C's share = C's profit sharing ratio x Share of B and C

C's share = 1/4 x Rs. 50,000

C's share = Rs. 12,500

Therefore, the JLP share on death of A will be shared among the partners as follows:

A's legal heirs: Rs. 50,000

B: Rs. 12,500

C: Rs. 12,500

Partnership Ratio: 2:1:1

Total Ratio: 4

JLP amount: Rs. 1,20,000

Surrender Value: Rs. 20,000

Step 1: Calculation of JLP Share

Total JLP Share = JLP amount - Surrender Value

Total JLP Share = Rs. 1,20,000 - Rs. 20,000

Total JLP Share = Rs. 1,00,000

A's share = 2/4 x Total JLP Share

A's share = 1/2 x Rs. 1,00,000

A's share = Rs. 50,000

B's share = 1/4 x Total JLP Share

B's share = 1/4 x Rs. 1,00,000

B's share = Rs. 25,000

C's share = 1/4 x Total JLP Share

C's share = 1/4 x Rs. 1,00,000

C's share = Rs. 25,000

Step 2: Sharing of JLP Share on Death of A

A's share will be given to his legal heirs.

Remaining JLP share will be shared among the partners in their profit sharing ratio.

Share of B and C = Total JLP Share - A's share

Share of B and C = Rs. 1,00,000 - Rs. 50,000

Share of B and C = Rs. 50,000

B's share = B's profit sharing ratio x Share of B and C

B's share = 1/4 x Rs. 50,000

B's share = Rs. 12,500

C's share = C's profit sharing ratio x Share of B and C

C's share = 1/4 x Rs. 50,000

C's share = Rs. 12,500

Therefore, the JLP share on death of A will be shared among the partners as follows:

A's legal heirs: Rs. 50,000

B: Rs. 12,500

C: Rs. 12,500

In the absence of proper agreement, representative of the deseased partner is entitled to the Dead partner’s share in the following items.- a)Profits till date, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

- b)Capital, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

- c)Capital, profits till date, goodwill, interest on capital, share in revalued assets and liabilities.

- d)Capital, profits till date, goodwill, joint life policy, share in revalued assets and liabilities.

Correct answer is option 'D'. Can you explain this answer?

In the absence of proper agreement, representative of the deseased partner is entitled to the Dead partner’s share in the following items.

a)

Profits till date, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

b)

Capital, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

c)

Capital, profits till date, goodwill, interest on capital, share in revalued assets and liabilities.

d)

Capital, profits till date, goodwill, joint life policy, share in revalued assets and liabilities.

|

Sai Kulkarni answered |

Explanation:

The representative of the deceased partner is entitled to the deceased partner's share in the following items:

A: Profits till date, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

B: Capital, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

C: Capital, profits till date, goodwill, interest on capital, share in revalued assets and liabilities.

D: Capital, profits till date, goodwill, joint life policy, share in revalued assets and liabilities.

The correct answer is D because it includes all the entitlements that the representative of the deceased partner is entitled to.

Here is a breakdown of each option:

A:

- Profits till date: The representative is entitled to receive the deceased partner's share of profits earned until the date of death.

- Goodwill: The representative is entitled to the deceased partner's share of goodwill, which is the value of the firm's reputation and customer base.

- Joint life policy: The representative is entitled to the deceased partner's share of any joint life insurance policy taken by the partnership.

- Interest on capital: The representative is entitled to the deceased partner's share of interest earned on their capital investment in the partnership.

- Share in revalued assets and liabilities: The representative is entitled to the deceased partner's share in any revaluation of the partnership's assets and liabilities.

B:

- Capital: The representative is entitled to the deceased partner's share of the capital invested in the partnership.

- Goodwill: Same as option A.

- Joint life policy: Same as option A.

- Interest on capital: Same as option A.

- Share in revalued assets and liabilities: Same as option A.

C:

- Capital: Same as option B.

- Profits till date: Same as option A.

- Goodwill: Same as option A.

- Interest on capital: Same as option A.

- Share in revalued assets and liabilities: Same as option A.

D:

- Capital: Same as option B.

- Profits till date: Same as option A.

- Goodwill: Same as option A.

- Joint life policy: Same as option A.

- Share in revalued assets and liabilities: Same as option A.

Therefore, option D is the correct answer as it includes all the entitlements that the representative of the deceased partner is entitled to.

The representative of the deceased partner is entitled to the deceased partner's share in the following items:

A: Profits till date, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

B: Capital, goodwill, joint life policy, interest on capital, share in revalued assets and liabilities.

C: Capital, profits till date, goodwill, interest on capital, share in revalued assets and liabilities.

D: Capital, profits till date, goodwill, joint life policy, share in revalued assets and liabilities.

The correct answer is D because it includes all the entitlements that the representative of the deceased partner is entitled to.

Here is a breakdown of each option:

A:

- Profits till date: The representative is entitled to receive the deceased partner's share of profits earned until the date of death.

- Goodwill: The representative is entitled to the deceased partner's share of goodwill, which is the value of the firm's reputation and customer base.

- Joint life policy: The representative is entitled to the deceased partner's share of any joint life insurance policy taken by the partnership.

- Interest on capital: The representative is entitled to the deceased partner's share of interest earned on their capital investment in the partnership.

- Share in revalued assets and liabilities: The representative is entitled to the deceased partner's share in any revaluation of the partnership's assets and liabilities.

B:

- Capital: The representative is entitled to the deceased partner's share of the capital invested in the partnership.

- Goodwill: Same as option A.

- Joint life policy: Same as option A.

- Interest on capital: Same as option A.

- Share in revalued assets and liabilities: Same as option A.

C:

- Capital: Same as option B.

- Profits till date: Same as option A.

- Goodwill: Same as option A.

- Interest on capital: Same as option A.

- Share in revalued assets and liabilities: Same as option A.

D:

- Capital: Same as option B.

- Profits till date: Same as option A.

- Goodwill: Same as option A.

- Joint life policy: Same as option A.

- Share in revalued assets and liabilities: Same as option A.

Therefore, option D is the correct answer as it includes all the entitlements that the representative of the deceased partner is entitled to.

A, B, C are partners sharing profits in the ratio 1:1:2. C died on 30th June 2006 and profits for the accounting year ended on 31st December 2006 were Rs. 24,000. How much share in profits will be credited to C’s Account. - a)Rs. 12,000

- b)Rs. 6,000

- c)Rs. 24,000

- d)Rs. 3,000

Correct answer is option 'B'. Can you explain this answer?

A, B, C are partners sharing profits in the ratio 1:1:2. C died on 30th June 2006 and profits for the accounting year ended on 31st December 2006 were Rs. 24,000. How much share in profits will be credited to C’s Account.

a)

Rs. 12,000

b)

Rs. 6,000

c)

Rs. 24,000

d)

Rs. 3,000

|

|

Harshad Kapoor answered |

Since C died on 30th June 2006, he was a partner for the first half of the accounting year (1st January 2006 to 30th June 2006). Therefore, his share in profits for this period will be calculated separately.

Ratio in which profits are shared = 1:1:2

Let the total profit for the year be x.

Profit for the first half of the year (1st January 2006 to 30th June 2006):

Total profit for the year * (1/4) = x * (1/4)

C's share in the first half of the year = (1/4) * (2/4) * x = x/8

Profit for the second half of the year (1st July 2006 to 31st December 2006):

Total profit for the year * (3/4) = x * (3/4)

Since C died on 30th June 2006, he is not entitled to any share in the profit for the second half of the year.

Therefore, C's share in the profits for the whole year = C's share in the first half of the year = x/8

Given that the total profit for the year is Rs. 24,000:

x = Rs. 24,000

C's share in the profits for the whole year = x/8 = 24,000/8 = Rs. 3,000

Therefore, C's share in profits will be credited with Rs. 3,000.

Ratio in which profits are shared = 1:1:2

Let the total profit for the year be x.

Profit for the first half of the year (1st January 2006 to 30th June 2006):

Total profit for the year * (1/4) = x * (1/4)

C's share in the first half of the year = (1/4) * (2/4) * x = x/8

Profit for the second half of the year (1st July 2006 to 31st December 2006):

Total profit for the year * (3/4) = x * (3/4)

Since C died on 30th June 2006, he is not entitled to any share in the profit for the second half of the year.

Therefore, C's share in the profits for the whole year = C's share in the first half of the year = x/8

Given that the total profit for the year is Rs. 24,000:

x = Rs. 24,000

C's share in the profits for the whole year = x/8 = 24,000/8 = Rs. 3,000

Therefore, C's share in profits will be credited with Rs. 3,000.

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006 and profits for the accounting year 2005-2006 were Rs. 24,000. How much share in profits for the period 1st April 2006 to 30th June 2006 will be credited to D’s Account.- a)Rs. 6,000.

- b)Rs. 1,500.

- c)Nil.

- d)Rs. 2,000.

Correct answer is option 'B'. Can you explain this answer?

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006 and profits for the accounting year 2005-2006 were Rs. 24,000. How much share in profits for the period 1st April 2006 to 30th June 2006 will be credited to D’s Account.

a)

Rs. 6,000.

b)

Rs. 1,500.

c)

Nil.

d)

Rs. 2,000.

|

|

Anu Sen answered |

Solution:

Given,

Profit sharing ratio of R, J and D = 7:5:4

Profit for the accounting year 2005-2006 = Rs. 24,000

Profit earned from 1st April 2006 to 30th June 2006 = ?

Since D died on 30th June 2006, his share in the profit earned during this period will be credited to his account.

To calculate D's share in profits for the period 1st April 2006 to 30th June 2006, we need to find out the profit earned during this period.

Calculation:

Let the profit earned from 1st April 2006 to 30th June 2006 be x.

Total profit for the year = Profit for the period 1st April 2006 to 30th June 2006 + Profit for the period 1st July 2005 to 31st March 2006

24000 = x + (x/3) * 9

24000 = x + 3x

24000 = 4x

x = 6000

Therefore, profit earned from 1st April 2006 to 30th June 2006 = Rs. 6000

D's share in the profit earned during this period will be calculated as follows:

D's share = (Profit earned from 1st April 2006 to 30th June 2006 * D's profit sharing ratio)/(Total profit sharing ratio)

D's share = (6000 * 4)/(7+5+4)

D's share = 24000/16

D's share = Rs. 1500

Therefore, option (b) Rs. 1500 is the correct answer.

Given,

Profit sharing ratio of R, J and D = 7:5:4

Profit for the accounting year 2005-2006 = Rs. 24,000

Profit earned from 1st April 2006 to 30th June 2006 = ?

Since D died on 30th June 2006, his share in the profit earned during this period will be credited to his account.

To calculate D's share in profits for the period 1st April 2006 to 30th June 2006, we need to find out the profit earned during this period.

Calculation:

Let the profit earned from 1st April 2006 to 30th June 2006 be x.

Total profit for the year = Profit for the period 1st April 2006 to 30th June 2006 + Profit for the period 1st July 2005 to 31st March 2006

24000 = x + (x/3) * 9

24000 = x + 3x

24000 = 4x

x = 6000

Therefore, profit earned from 1st April 2006 to 30th June 2006 = Rs. 6000

D's share in the profit earned during this period will be calculated as follows:

D's share = (Profit earned from 1st April 2006 to 30th June 2006 * D's profit sharing ratio)/(Total profit sharing ratio)

D's share = (6000 * 4)/(7+5+4)

D's share = 24000/16

D's share = Rs. 1500

Therefore, option (b) Rs. 1500 is the correct answer.

B, C, D are partners sharing profits in the ratio 7:5:4. D died on 30th June 2006 and profits for the year 2005-2006 were Rs. 12,000. How much share in profits for the period 1st April 2006 to 30th June 2006 will be credited to D’s Account?- a)Rs. 3,000

- b)Rs. 750

- c)Nil

- d)Rs. 1,000

Correct answer is option 'B'. Can you explain this answer?

B, C, D are partners sharing profits in the ratio 7:5:4. D died on 30th June 2006 and profits for the year 2005-2006 were Rs. 12,000. How much share in profits for the period 1st April 2006 to 30th June 2006 will be credited to D’s Account?

a)

Rs. 3,000

b)

Rs. 750

c)

Nil

d)

Rs. 1,000

|

|

Akshay Das answered |

Since D died on 30th June 2006, his share in profits will be calculated for the period from 1st April 2006 to 30th June 2006.

First, we need to calculate the total profits for the year 2005-2006. Let's assume that the profits for the year were divided equally among the partners for simplicity. Then, each partner's share of the profits would be:

B's share = (7/16) x Rs. 12,000 = Rs. 5,250

C's share = (5/16) x Rs. 12,000 = Rs. 3,750

D's share = (4/16) x Rs. 12,000 = Rs. 3,000

Now, we need to calculate the profits for the period from 1st April 2006 to 30th June 2006. Let's assume that the profits for this period were also divided equally among the partners. Then, each partner's share of the profits would be:

B's share = (7/12) x (1/4) x profits for the year = (7/12) x (1/4) x Rs. 12,000 = Rs. 1,225

C's share = (5/12) x (1/4) x profits for the year = (5/12) x (1/4) x Rs. 12,000 = Rs. 875

D's share = (4/12) x (1/4) x profits for the year = (1/3) x Rs. 3,000 = Rs. 1,000

Therefore, D's share in profits for the period 1st April 2006 to 30th June 2006 will be Rs. 1,000.

First, we need to calculate the total profits for the year 2005-2006. Let's assume that the profits for the year were divided equally among the partners for simplicity. Then, each partner's share of the profits would be:

B's share = (7/16) x Rs. 12,000 = Rs. 5,250

C's share = (5/16) x Rs. 12,000 = Rs. 3,750

D's share = (4/16) x Rs. 12,000 = Rs. 3,000

Now, we need to calculate the profits for the period from 1st April 2006 to 30th June 2006. Let's assume that the profits for this period were also divided equally among the partners. Then, each partner's share of the profits would be:

B's share = (7/12) x (1/4) x profits for the year = (7/12) x (1/4) x Rs. 12,000 = Rs. 1,225

C's share = (5/12) x (1/4) x profits for the year = (5/12) x (1/4) x Rs. 12,000 = Rs. 875

D's share = (4/12) x (1/4) x profits for the year = (1/3) x Rs. 3,000 = Rs. 1,000

Therefore, D's share in profits for the period 1st April 2006 to 30th June 2006 will be Rs. 1,000.

J, K and L were equal partners in a firm. The firm has taken individual life policy of Rs. 50,000 for each partner. J died on 5th March 2011. The surrender value was Rs. 2,000 for each policy on the date of death of J. The amount payable to J in respective policies would be _______.- a)Rs. 17,000

- b)Rs. 18,000

- c)Rs. 50,000

- d)Rs. 54,000

Correct answer is option 'B'. Can you explain this answer?

J, K and L were equal partners in a firm. The firm has taken individual life policy of Rs. 50,000 for each partner. J died on 5th March 2011. The surrender value was Rs. 2,000 for each policy on the date of death of J. The amount payable to J in respective policies would be _______.

a)

Rs. 17,000

b)

Rs. 18,000

c)

Rs. 50,000

d)

Rs. 54,000

|

|

Ruchi Mishra answered |

Calculation of Surrender Value

The surrender value of each policy is given as Rs. 2,000. Therefore, the total surrender value of all policies is:

3 partners x Rs. 2,000 = Rs. 6,000

Calculation of Amount Payable

Since J died, the amount payable to J in each policy is calculated as follows:

Amount Payable = (Sum Assured + Bonus) - Surrender Value

Here, the sum assured is Rs. 50,000 for each policy, but since no information is given about bonus, it can be assumed that there is no bonus.

Therefore, the amount payable to J in each policy is:

Amount Payable = (Rs. 50,000 + 0) - Rs. 2,000

Amount Payable = Rs. 48,000

As J had a policy with a sum assured of Rs. 50,000, the amount payable to J in his policy would be Rs. 48,000.

Since there are 3 partners and each partner has a policy of Rs. 50,000, the total sum assured is Rs. 1,50,000. Therefore, the total amount payable to J's legal heirs would be:

Amount Payable = Rs. 48,000 x 3 = Rs. 1,44,000

However, since J is no longer a partner, his share in the firm is transferred to his legal heirs. Therefore, the total amount payable to J's legal heirs would be reduced by J's share in the firm.

Assuming that the share of J, K, and L in the firm was equal, the share of J would be 1/3. Therefore, the amount payable to J's legal heirs would be:

Amount Payable = Rs. 1,44,000 - (1/3 x Rs. 1,50,000) = Rs. 1,44,000 - Rs. 50,000 = Rs. 94,000

Therefore, the amount payable to J in respective policies would be Rs. 48,000 and the total amount payable to J's legal heirs would be Rs. 94,000, which is option B.

The surrender value of each policy is given as Rs. 2,000. Therefore, the total surrender value of all policies is:

3 partners x Rs. 2,000 = Rs. 6,000

Calculation of Amount Payable

Since J died, the amount payable to J in each policy is calculated as follows:

Amount Payable = (Sum Assured + Bonus) - Surrender Value

Here, the sum assured is Rs. 50,000 for each policy, but since no information is given about bonus, it can be assumed that there is no bonus.

Therefore, the amount payable to J in each policy is:

Amount Payable = (Rs. 50,000 + 0) - Rs. 2,000

Amount Payable = Rs. 48,000

As J had a policy with a sum assured of Rs. 50,000, the amount payable to J in his policy would be Rs. 48,000.

Since there are 3 partners and each partner has a policy of Rs. 50,000, the total sum assured is Rs. 1,50,000. Therefore, the total amount payable to J's legal heirs would be:

Amount Payable = Rs. 48,000 x 3 = Rs. 1,44,000

However, since J is no longer a partner, his share in the firm is transferred to his legal heirs. Therefore, the total amount payable to J's legal heirs would be reduced by J's share in the firm.

Assuming that the share of J, K, and L in the firm was equal, the share of J would be 1/3. Therefore, the amount payable to J's legal heirs would be:

Amount Payable = Rs. 1,44,000 - (1/3 x Rs. 1,50,000) = Rs. 1,44,000 - Rs. 50,000 = Rs. 94,000

Therefore, the amount payable to J in respective policies would be Rs. 48,000 and the total amount payable to J's legal heirs would be Rs. 94,000, which is option B.

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006 and profits for the accounting year 2005-2006 were Rs. 24,000. How much share in profit for the period 1st April 2006 to 30th June 2006 will be credited to D’s Account - a)Rs. 6,000

- b)Rs. 27,600

- c)Rs. 82,800

- d)Rs. 27,000

Correct answer is option 'B'. Can you explain this answer?

R, J and D are the partners sharing profits in the ratio 7:5:4. D died on 30th June 2006 and profits for the accounting year 2005-2006 were Rs. 24,000. How much share in profit for the period 1st April 2006 to 30th June 2006 will be credited to D’s Account

a)

Rs. 6,000

b)

Rs. 27,600

c)

Rs. 82,800

d)

Rs. 27,000

|

|

Snehal Das answered |

As per the given information, the total profit for the year 2005-2006 was Rs. 24,000, which was earned from 1st April 2005 to 30th June 2006.

Since D died on 30th June 2006, his share in the profit will be calculated only for the period from 1st April 2006 to 30th June 2006.

The total period for the year 2005-2006 is 15 months (1st April 2005 to 30th June 2006).

Therefore, the profit for the period from 1st April 2006 to 30th June 2006 can be calculated as follows:

Profit for the year 2005-2006 = Rs. 24,000

Profit for 3 months (1st April 2006 to 30th June 2006) = (Profit for the year 2005-2006)/15 x 3

= (24000)/15 x 3

= Rs. 4,800

Now, the total profit for the period from 1st April 2006 to 30th June 2006 is Rs. 4,800.

The ratio of profit sharing between R, J and D is 7:5:4.

Therefore, D's share in the profit for the period from 1st April 2006 to 30th June 2006 can be calculated as follows:

D's share = (4/16) x 4800

= Rs. 1,200

Therefore, D's share in profit for the period from 1st April 2006 to 30th June 2006 will be Rs. 1,200.

Since D died on 30th June 2006, his share in the profit will be calculated only for the period from 1st April 2006 to 30th June 2006.

The total period for the year 2005-2006 is 15 months (1st April 2005 to 30th June 2006).

Therefore, the profit for the period from 1st April 2006 to 30th June 2006 can be calculated as follows:

Profit for the year 2005-2006 = Rs. 24,000

Profit for 3 months (1st April 2006 to 30th June 2006) = (Profit for the year 2005-2006)/15 x 3

= (24000)/15 x 3

= Rs. 4,800

Now, the total profit for the period from 1st April 2006 to 30th June 2006 is Rs. 4,800.

The ratio of profit sharing between R, J and D is 7:5:4.

Therefore, D's share in the profit for the period from 1st April 2006 to 30th June 2006 can be calculated as follows:

D's share = (4/16) x 4800

= Rs. 1,200

Therefore, D's share in profit for the period from 1st April 2006 to 30th June 2006 will be Rs. 1,200.

A, B and C are partners sharing profits in the ratio of 3:2:1. They had a Joint Life Policy of Rs. 3,00,000. Surrender value of JLP in Balance Sheet is Rs. 90,000. C dies. What is share of each partner in JLP?- a)Rs. 1,05,000; Rs. 70,000; Rs. 35,000

- b)Rs. 45,000; Rs. 30,000; Rs. 15,000

- c)Rs. 1,50,000; Rs. 1,00,000; Rs. 50,000

- d)Rs. 1,95,000; Rs. 1,30,000; Rs. 65,000

Correct answer is option 'A'. Can you explain this answer?

A, B and C are partners sharing profits in the ratio of 3:2:1. They had a Joint Life Policy of Rs. 3,00,000. Surrender value of JLP in Balance Sheet is Rs. 90,000. C dies. What is share of each partner in JLP?

a)

Rs. 1,05,000; Rs. 70,000; Rs. 35,000

b)

Rs. 45,000; Rs. 30,000; Rs. 15,000

c)

Rs. 1,50,000; Rs. 1,00,000; Rs. 50,000

d)

Rs. 1,95,000; Rs. 1,30,000; Rs. 65,000

|

|

Aarya Sharma answered |

If Joint Life Policy appears in the Balance Sheet at surrender value, then the firm will gain on the death of a partner and partners will get

policy amount - Surrender value i.e., in their profit sharing ratio

Rs. 3,00,000 - Rs. 90,000 = Rs. 2,10,000

Distribution of JLP among the partners is :

A = 2,10,000 * (3/6) = 105000

B = 2,10,000 * (2/6) = 70000

C = 2,10,000 * (1/6) = 35000

policy amount - Surrender value i.e., in their profit sharing ratio

Rs. 3,00,000 - Rs. 90,000 = Rs. 2,10,000

Distribution of JLP among the partners is :

A = 2,10,000 * (3/6) = 105000

B = 2,10,000 * (2/6) = 70000

C = 2,10,000 * (1/6) = 35000

When premium paid on JLP taken up severely for each partner, the amount received on death of a partner would be firm’s profit. It is also necessary to credit Partner’s Capital Account with …………. Of the policy on the lives of the remaining partners- a)Policy Value

- b)Lump-sum Value

- c)Surrender Value

- d)Actual Value

Correct answer is option 'C'. Can you explain this answer?

When premium paid on JLP taken up severely for each partner, the amount received on death of a partner would be firm’s profit. It is also necessary to credit Partner’s Capital Account with …………. Of the policy on the lives of the remaining partners

a)

Policy Value

b)

Lump-sum Value

c)

Surrender Value

d)

Actual Value

|

|

Ruchi Mishra answered |

Understanding Joint Life Policies (JLP) in Partnerships

In a partnership, when a Joint Life Policy (JLP) is taken out for the partners, several accounting considerations arise, particularly in the event of a partner's death.

Importance of JLP Premiums

- Premiums paid on JLP are considered a crucial part of the partnership's financial management.

- Upon the death of a partner, the sum insured from the JLP is received by the firm, which is treated as the firm's profit.

Crediting the Partner’s Capital Account

- It is essential to adjust the capital accounts of the remaining partners when a partner passes away.

- The remaining partners should have their capital accounts credited with the appropriate amount pertaining to the JLP.

Why Surrender Value is the Correct Answer

- The correct answer, "Surrender Value," refers to the amount that the policyholder can receive if the policy is terminated before its maturity.

- This value is significant as it reflects the current worth of the JLP for the remaining partners.

- By crediting the Partner’s Capital Account with the Surrender Value, the financial standing of the partnership remains equitable, recognizing the policy's value while ensuring the remaining partners are compensated fairly.

Conclusion

In summary, when dealing with a JLP in a partnership, it is critical to credit the Partner’s Capital Account with the Surrender Value of the policy on the lives of the remaining partners. This approach ensures that the financial implications of a partner's death are managed effectively within the partnership's accounts.

In a partnership, when a Joint Life Policy (JLP) is taken out for the partners, several accounting considerations arise, particularly in the event of a partner's death.

Importance of JLP Premiums

- Premiums paid on JLP are considered a crucial part of the partnership's financial management.

- Upon the death of a partner, the sum insured from the JLP is received by the firm, which is treated as the firm's profit.

Crediting the Partner’s Capital Account

- It is essential to adjust the capital accounts of the remaining partners when a partner passes away.

- The remaining partners should have their capital accounts credited with the appropriate amount pertaining to the JLP.

Why Surrender Value is the Correct Answer

- The correct answer, "Surrender Value," refers to the amount that the policyholder can receive if the policy is terminated before its maturity.

- This value is significant as it reflects the current worth of the JLP for the remaining partners.

- By crediting the Partner’s Capital Account with the Surrender Value, the financial standing of the partnership remains equitable, recognizing the policy's value while ensuring the remaining partners are compensated fairly.

Conclusion

In summary, when dealing with a JLP in a partnership, it is critical to credit the Partner’s Capital Account with the Surrender Value of the policy on the lives of the remaining partners. This approach ensures that the financial implications of a partner's death are managed effectively within the partnership's accounts.

JLP of the partners is a/ an ___________account:- a)Nominal

- b)Personal

- c)Representative Personal

- d)Assets

Correct answer is option 'D'. Can you explain this answer?

JLP of the partners is a/ an ___________account:

a)

Nominal

b)

Personal

c)

Representative Personal

d)

Assets

|

|

Priya Patel answered |

Joint Life Policy Reserve Account is prepared simultaneously with the JLP Account. While JLP Account is maintained at the surrender value of the joint policy, JLP Reserve Account is shown with the difference amount of the debit balance of the JLP Account and the surrender value. When premium is paid, then it is charged from the Profit and Loss Appropriation Account. At the end of the accounting period, JLP Account is shown on the Assets side, while JLP Reserve Account is shown on the Liabilities side of the firm's Balance Sheet. At the time of maturity of the policy, JLP Reserve Account is closed first and if any credit balance remains in this account, then the same is transferred to the JLP Account. Finally, JLP Account is closed by transferring its balance to the Partners' Capital Accounts (Old Partners in case of admission and All Partners in case of Retirement or Death).

If three partners A, B & C are sharing profits as 5:3:2, then on the death of a partner A, how much B & C will pay to A’s executer on account of goodwill. Goodwill is to be calculated on the basis of 2 years purchase of last 3 years average profits. Profits for last three years are: Rs. 3,29,000; Rs. 3,46,000 and Rs. 4,05,000.- a)Rs. 2,16,000 & Rs. 1,42,000.

- b)Rs. 2,44,000 & Rs. 2,16,000.

- c)Rs. 3,60,000 & Rs. 3,60,000.

- d)Rs. 2,16,000 & Rs. 1,44,000.

Correct answer is option 'D'. Can you explain this answer?

If three partners A, B & C are sharing profits as 5:3:2, then on the death of a partner A, how much B & C will pay to A’s executer on account of goodwill. Goodwill is to be calculated on the basis of 2 years purchase of last 3 years average profits. Profits for last three years are: Rs. 3,29,000; Rs. 3,46,000 and Rs. 4,05,000.

a)

Rs. 2,16,000 & Rs. 1,42,000.

b)

Rs. 2,44,000 & Rs. 2,16,000.

c)

Rs. 3,60,000 & Rs. 3,60,000.

d)

Rs. 2,16,000 & Rs. 1,44,000.

|

|

Ameya Menon answered |

, and C invest $10,000, $15,000, and $20,000 respectively in a business, the total investment in the business would be:

$10,000 + $15,000 + $20,000 = $45,000

To find the percentage of each partner's investment in the total investment, we can divide each partner's investment by the total investment and multiply by 100.

Partner A's percentage of the total investment:

($10,000 / $45,000) x 100 = 22.22%

Partner B's percentage of the total investment:

($15,000 / $45,000) x 100 = 33.33%

Partner C's percentage of the total investment:

($20,000 / $45,000) x 100 = 44.44%

$10,000 + $15,000 + $20,000 = $45,000

To find the percentage of each partner's investment in the total investment, we can divide each partner's investment by the total investment and multiply by 100.

Partner A's percentage of the total investment:

($10,000 / $45,000) x 100 = 22.22%

Partner B's percentage of the total investment:

($15,000 / $45,000) x 100 = 33.33%

Partner C's percentage of the total investment:

($20,000 / $45,000) x 100 = 44.44%

A, B and C are the partners sharing profits and losses in the ratio 2:1:1. Firm has a joint life policy of Rs. 1,20,000 and in the balance sheet it is appearing at the surrender value i.e. Rs. 20,000. On the death of A, how this JLP will be shared among the partners.- a)50,000:25,000:25,000

- b)60,000:30,000:30,000

- c)40,000:35,000:25,000

- d)Whole of Rs. 1,20,000 will be paid to A

Correct answer is option 'A'. Can you explain this answer?

A, B and C are the partners sharing profits and losses in the ratio 2:1:1. Firm has a joint life policy of Rs. 1,20,000 and in the balance sheet it is appearing at the surrender value i.e. Rs. 20,000. On the death of A, how this JLP will be shared among the partners.

a)

50,000:25,000:25,000

b)

60,000:30,000:30,000

c)

40,000:35,000:25,000

d)

Whole of Rs. 1,20,000 will be paid to A

|

|

Anup Karmakar answered |

Easy question , The amount to be distributed among the partner will be 120,000 less 20,000 = 100,000

in the ratio of 2:1:1 Thanks ;)

in the ratio of 2:1:1 Thanks ;)

All of the following except one is the method of recording joint life Policy- a)Premium paid charged to revenue

- b)JLP Account maintained at the surrender value

- c)JLP Account maintained at the surrender value along with the Reserve

- d)Surrender value distributed among the partners in the partners in the profit sharing ratio

Correct answer is option 'D'. Can you explain this answer?

All of the following except one is the method of recording joint life Policy

a)

Premium paid charged to revenue

b)

JLP Account maintained at the surrender value

c)

JLP Account maintained at the surrender value along with the Reserve

d)

Surrender value distributed among the partners in the partners in the profit sharing ratio

|

|

Rutuja Dasgupta answered |

Recording Joint Life Policy:

Methods of Recording:

- Premium paid charged to revenue

- JLP Account maintained at the surrender value

- JLP Account maintained at the surrender value along with the Reserve

Explanation:

When recording a joint life policy, the premium paid can be charged to revenue. This means that the premium paid for the policy is treated as an expense in the income statement.

Another method is to maintain a Joint Life Policy (JLP) account at the surrender value. This allows for the tracking of the policy's value separate from other accounts.

Additionally, the JLP account can be maintained at the surrender value along with a reserve. This reserve can help account for any potential fluctuations in the policy's value over time.

Incorrect Option:

- Surrender value distributed among the partners in the profit sharing ratio

This option is incorrect because the surrender value of a joint life policy is typically not distributed among the partners in a profit-sharing ratio. The surrender value is usually used to determine the value of the policy if it is surrendered before maturity, rather than being distributed among partners.

Methods of Recording:

- Premium paid charged to revenue

- JLP Account maintained at the surrender value

- JLP Account maintained at the surrender value along with the Reserve

Explanation:

When recording a joint life policy, the premium paid can be charged to revenue. This means that the premium paid for the policy is treated as an expense in the income statement.

Another method is to maintain a Joint Life Policy (JLP) account at the surrender value. This allows for the tracking of the policy's value separate from other accounts.

Additionally, the JLP account can be maintained at the surrender value along with a reserve. This reserve can help account for any potential fluctuations in the policy's value over time.

Incorrect Option:

- Surrender value distributed among the partners in the profit sharing ratio

This option is incorrect because the surrender value of a joint life policy is typically not distributed among the partners in a profit-sharing ratio. The surrender value is usually used to determine the value of the policy if it is surrendered before maturity, rather than being distributed among partners.

In case of death of a partner, share of goodwill of deceased partner, will be borne by the remaining partners in:- a)Sacrificing Ratio

- b)Gaining Ratio

- c)Old Profit Sharing Ratio

- d)Net Profit Sharing Ratio

Correct answer is option 'B'. Can you explain this answer?

In case of death of a partner, share of goodwill of deceased partner, will be borne by the remaining partners in:

a)

Sacrificing Ratio

b)

Gaining Ratio

c)

Old Profit Sharing Ratio

d)

Net Profit Sharing Ratio

|

|

Deepika Desai answered |

Explanation:

When a partner dies, his share in the partnership firm is transferred to his legal heirs or nominees. The share of the deceased partner in the firm includes his share in the assets, liabilities, and goodwill of the firm. The share of goodwill of the deceased partner is also distributed among the remaining partners.

The question asks about the share of goodwill of the deceased partner and how it will be borne by the remaining partners. The answer is option 'B', which is the gaining ratio.

Gaining Ratio:

The gaining ratio is the ratio in which the remaining partners acquire the share of the outgoing partner. In case of the death of a partner, the gaining ratio is calculated by adding the share of the deceased partner to the existing profit sharing ratio of the remaining partners. The formula for calculating the gaining ratio is:

Gaining Ratio = New Profit Sharing Ratio - Old Profit Sharing Ratio

The share of goodwill of the deceased partner is distributed among the remaining partners in the gaining ratio. This means that the partners who gain more from the share of the deceased partner will bear a higher share of the goodwill.

Example:

Suppose a partnership firm has three partners A, B, and C with a profit sharing ratio of 3:2:1. If partner A dies and his share is transferred to his legal heirs, then the share of goodwill of partner A will be distributed among partners B and C in the gaining ratio.

Suppose the gaining ratio of B and C is 2:1. This means that B will gain twice the share of C from the share of A. If the share of goodwill of A is Rs. 30,000, then B will bear Rs. 20,000 (2/3 of Rs. 30,000) and C will bear Rs. 10,000 (1/3 of Rs. 30,000) of the share of goodwill of A.

Conclusion:

In case of the death of a partner, the share of goodwill of the deceased partner is distributed among the remaining partners in the gaining ratio. The partners who gain more from the share of the deceased partner will bear a higher share of the goodwill.

When a partner dies, his share in the partnership firm is transferred to his legal heirs or nominees. The share of the deceased partner in the firm includes his share in the assets, liabilities, and goodwill of the firm. The share of goodwill of the deceased partner is also distributed among the remaining partners.

The question asks about the share of goodwill of the deceased partner and how it will be borne by the remaining partners. The answer is option 'B', which is the gaining ratio.

Gaining Ratio:

The gaining ratio is the ratio in which the remaining partners acquire the share of the outgoing partner. In case of the death of a partner, the gaining ratio is calculated by adding the share of the deceased partner to the existing profit sharing ratio of the remaining partners. The formula for calculating the gaining ratio is:

Gaining Ratio = New Profit Sharing Ratio - Old Profit Sharing Ratio

The share of goodwill of the deceased partner is distributed among the remaining partners in the gaining ratio. This means that the partners who gain more from the share of the deceased partner will bear a higher share of the goodwill.

Example:

Suppose a partnership firm has three partners A, B, and C with a profit sharing ratio of 3:2:1. If partner A dies and his share is transferred to his legal heirs, then the share of goodwill of partner A will be distributed among partners B and C in the gaining ratio.

Suppose the gaining ratio of B and C is 2:1. This means that B will gain twice the share of C from the share of A. If the share of goodwill of A is Rs. 30,000, then B will bear Rs. 20,000 (2/3 of Rs. 30,000) and C will bear Rs. 10,000 (1/3 of Rs. 30,000) of the share of goodwill of A.

Conclusion:

In case of the death of a partner, the share of goodwill of the deceased partner is distributed among the remaining partners in the gaining ratio. The partners who gain more from the share of the deceased partner will bear a higher share of the goodwill.

A, B and C takes a Joint Life Policy their profit sharing ratio is 2:2:1. On death of B, A and C decides to share profits equally. They had taken a Joint Life Policy of Rs. 2,50,000 with the surrender value Rs. 50,000. What will be the treatment in the partner’s capital account on receiving the JLP amount if joint life policy is maintained at the surrender value?- a)Rs. 50,000 credited to all the partners in old ratio

- b)Rs. 2,50,000 credited to all the partners in old ratio

- c)Rs 2,00,000 credited to all the partners in old ratio

- d)No treatment is required

Correct answer is option 'C'. Can you explain this answer?

A, B and C takes a Joint Life Policy their profit sharing ratio is 2:2:1. On death of B, A and C decides to share profits equally. They had taken a Joint Life Policy of Rs. 2,50,000 with the surrender value Rs. 50,000. What will be the treatment in the partner’s capital account on receiving the JLP amount if joint life policy is maintained at the surrender value?

a)

Rs. 50,000 credited to all the partners in old ratio

b)

Rs. 2,50,000 credited to all the partners in old ratio

c)

Rs 2,00,000 credited to all the partners in old ratio

d)

No treatment is required

|

|

Tejas Chaudhary answered |

Ship's books on death of B?

The first step is to calculate the surrender value of the policy after the death of B. Since the policy is a joint life policy, it will continue until the death of the last surviving partner. Therefore, the policy has a surrender value of Rs. 50,000 at the time of B's death.

Next, the total amount received from the policy needs to be calculated. The policy has a sum assured of Rs. 2,50,000, and since it was a joint life policy, the full sum assured is payable on the death of the last surviving partner. Since B is the second partner to die, only a part of the sum assured is payable. The amount payable is calculated as follows:

B's share of the sum assured = 2/5 x 2,50,000 = Rs. 1,00,000

The total amount received from the policy is the sum of the surrender value and the amount payable, which is:

Total amount received = Rs. 50,000 + Rs. 1,00,000 = Rs. 1,50,000

The profit on the policy is calculated as the difference between the total amount received and the premium paid. Since the premium paid is not given, it cannot be calculated. However, since the partners had taken the policy for the purpose of sharing profits, it can be assumed that the premium paid is equal to the total amount received. Therefore, the profit on the policy is:

Profit on policy = Rs. 1,50,000 - Rs. 1,50,000 = Rs. 0

Since there is no profit on the policy, there is no need to make any adjustment in the partnership's books on the death of B. The amount received from the policy can be distributed among the partners as follows:

A's share = Rs. 1,50,000/2 = Rs. 75,000

C's share = Rs. 1,50,000/2 = Rs. 75,000

Therefore, A and C will each receive Rs. 75,000 from the policy, and there will be no entry in the partnership's books.

The first step is to calculate the surrender value of the policy after the death of B. Since the policy is a joint life policy, it will continue until the death of the last surviving partner. Therefore, the policy has a surrender value of Rs. 50,000 at the time of B's death.

Next, the total amount received from the policy needs to be calculated. The policy has a sum assured of Rs. 2,50,000, and since it was a joint life policy, the full sum assured is payable on the death of the last surviving partner. Since B is the second partner to die, only a part of the sum assured is payable. The amount payable is calculated as follows:

B's share of the sum assured = 2/5 x 2,50,000 = Rs. 1,00,000

The total amount received from the policy is the sum of the surrender value and the amount payable, which is:

Total amount received = Rs. 50,000 + Rs. 1,00,000 = Rs. 1,50,000

The profit on the policy is calculated as the difference between the total amount received and the premium paid. Since the premium paid is not given, it cannot be calculated. However, since the partners had taken the policy for the purpose of sharing profits, it can be assumed that the premium paid is equal to the total amount received. Therefore, the profit on the policy is:

Profit on policy = Rs. 1,50,000 - Rs. 1,50,000 = Rs. 0

Since there is no profit on the policy, there is no need to make any adjustment in the partnership's books on the death of B. The amount received from the policy can be distributed among the partners as follows:

A's share = Rs. 1,50,000/2 = Rs. 75,000

C's share = Rs. 1,50,000/2 = Rs. 75,000

Therefore, A and C will each receive Rs. 75,000 from the policy, and there will be no entry in the partnership's books.

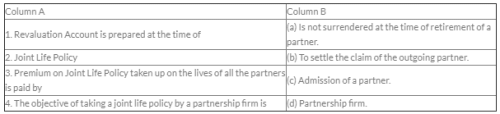

Revaluation account is prepared at the time of- a)Admission of a partner

- b)Retirement of a partner

- c)Death of a partner

- d)All of the above

Correct answer is option 'D'. Can you explain this answer?

Revaluation account is prepared at the time of

a)

Admission of a partner

b)

Retirement of a partner

c)

Death of a partner

d)

All of the above

|

|

Gayatri Khanna answered |

Revaluation Account in Partnership

Revaluation account is a ledger account that is prepared at the time of admission, retirement or death of a partner in a partnership firm. The following are the details:

Admission of a partner

When a new partner is admitted into the partnership firm, the assets and liabilities of the firm are revalued to determine the true and fair value of the business. The revaluation account is prepared to adjust the value of the assets and liabilities of the firm. This account is credited with the increase in the value of the assets and debited with the decrease in the value of the assets. The total of the debit side of the revaluation account represents the decrease in the value of the assets, and the total of the credit side represents the increase in the value of the assets.

Retirement of a partner

When a partner retires from the partnership firm, the assets and liabilities of the firm are revalued to determine the true and fair value of the business. The revaluation account is prepared to adjust the value of the assets and liabilities of the firm. This account is credited with the decrease in the value of the assets and debited with the increase in the value of the assets. The total of the debit side of the revaluation account represents the increase in the value of the assets, and the total of the credit side represents the decrease in the value of the assets.

Death of a partner

When a partner dies, the assets and liabilities of the firm are revalued to determine the true and fair value of the business. The revaluation account is prepared to adjust the value of the assets and liabilities of the firm. This account is credited with the decrease in the value of the assets and debited with the increase in the value of the assets. The total of the debit side of the revaluation account represents the increase in the value of the assets, and the total of the credit side represents the decrease in the value of the assets.

Conclusion

Revaluation account is prepared at the time of admission, retirement or death of a partner in a partnership firm. It is necessary to adjust the value of the assets and liabilities of the firm to determine the true and fair value of the business.

Revaluation account is a ledger account that is prepared at the time of admission, retirement or death of a partner in a partnership firm. The following are the details:

Admission of a partner

When a new partner is admitted into the partnership firm, the assets and liabilities of the firm are revalued to determine the true and fair value of the business. The revaluation account is prepared to adjust the value of the assets and liabilities of the firm. This account is credited with the increase in the value of the assets and debited with the decrease in the value of the assets. The total of the debit side of the revaluation account represents the decrease in the value of the assets, and the total of the credit side represents the increase in the value of the assets.

Retirement of a partner

When a partner retires from the partnership firm, the assets and liabilities of the firm are revalued to determine the true and fair value of the business. The revaluation account is prepared to adjust the value of the assets and liabilities of the firm. This account is credited with the decrease in the value of the assets and debited with the increase in the value of the assets. The total of the debit side of the revaluation account represents the increase in the value of the assets, and the total of the credit side represents the decrease in the value of the assets.

Death of a partner

When a partner dies, the assets and liabilities of the firm are revalued to determine the true and fair value of the business. The revaluation account is prepared to adjust the value of the assets and liabilities of the firm. This account is credited with the decrease in the value of the assets and debited with the increase in the value of the assets. The total of the debit side of the revaluation account represents the increase in the value of the assets, and the total of the credit side represents the decrease in the value of the assets.

Conclusion

Revaluation account is prepared at the time of admission, retirement or death of a partner in a partnership firm. It is necessary to adjust the value of the assets and liabilities of the firm to determine the true and fair value of the business.

On death of a partner, his executor is paid the share of profits of the dying partner for the relevant period. This payment is recorded in Profit & Loss ………..Account- a)Adjustment

- b)Appropriation

- c)Suspense

- d)Reserve

Correct answer is option 'C'. Can you explain this answer?

On death of a partner, his executor is paid the share of profits of the dying partner for the relevant period. This payment is recorded in Profit & Loss ………..Account

a)

Adjustment

b)

Appropriation

c)

Suspense

d)

Reserve

|

|

Sagarika Pillai answered |

Explanation:

Accounting Treatment:

- When a partner dies, his executor is entitled to receive the share of profits of the deceased partner for the relevant period.

- This payment is recorded in the Profit & Loss Account under the Suspense Account.

Suspense Account:

- The Suspense Account is used to temporarily record transactions that cannot be categorized into a specific account.

- In this case, the payment to the executor of the deceased partner's share of profits does not fit into the regular categories of Adjustment, Appropriation, or Reserve, so it is recorded in the Suspense Account.

Finalization of Accounts:

- The entry in the Suspense Account is a temporary measure until the final accounts are prepared and the distribution of profits is finalized.

- Once the final distribution is determined, the amount in the Suspense Account will be transferred to the appropriate account (such as Executor's Account or Partner's Capital Account).

Conclusion:

- In conclusion, the payment to the executor of a deceased partner's share of profits is recorded in the Profit & Loss Account under the Suspense Account until the final distribution is decided.

Accounting Treatment:

- When a partner dies, his executor is entitled to receive the share of profits of the deceased partner for the relevant period.

- This payment is recorded in the Profit & Loss Account under the Suspense Account.

Suspense Account:

- The Suspense Account is used to temporarily record transactions that cannot be categorized into a specific account.

- In this case, the payment to the executor of the deceased partner's share of profits does not fit into the regular categories of Adjustment, Appropriation, or Reserve, so it is recorded in the Suspense Account.

Finalization of Accounts:

- The entry in the Suspense Account is a temporary measure until the final accounts are prepared and the distribution of profits is finalized.

- Once the final distribution is determined, the amount in the Suspense Account will be transferred to the appropriate account (such as Executor's Account or Partner's Capital Account).

Conclusion:

- In conclusion, the payment to the executor of a deceased partner's share of profits is recorded in the Profit & Loss Account under the Suspense Account until the final distribution is decided.

The amount due to the deceased partner is paid to his: - a)Father

- b)Friends

- c)Wife

- d)Executors

Correct answer is option 'D'. Can you explain this answer?

The amount due to the deceased partner is paid to his:

a)

Father

b)

Friends

c)

Wife

d)

Executors

|

|

Vandana Kulkarni answered |

Understanding the Payment to a Deceased Partner's Account

When a partner in a partnership firm passes away, the distribution of their dues is governed by specific legal and financial principles. The correct answer to the question of who receives the amount due to the deceased partner is the executors of the estate. Let's delve into the rationale behind this.

1. Role of Executors

- Executors are individuals appointed to manage the estate of a deceased person.

- They are responsible for settling debts, distributing assets, and ensuring that the deceased's wishes (as expressed in a will, if available) are honored.

2. Legal Framework

- The law dictates that any outstanding dues owed to the deceased partner must be handled by their estate.

- This means that the amount due will not be directly paid to family members or friends but goes through the executors who manage the deceased partner's financial matters.

3. Distribution Process

- Once the executors receive the payment, they will settle any debts of the deceased.

- The remaining amount is then distributed to the rightful heirs or beneficiaries as per the laws of succession or the directions in the will.

4. Implications for Family and Friends

- Family members (e.g., spouse, children) and friends may ultimately benefit from the deceased partner's estate, but they do not receive direct payment from the partnership.

- This ensures that all financial obligations and legal processes are properly adhered to before any distribution to individuals connected to the deceased.

In summary, the amount due to a deceased partner is paid to their executors, who are legally tasked with managing the estate and ensuring proper distribution according to the deceased’s wishes and relevant laws.

When a partner in a partnership firm passes away, the distribution of their dues is governed by specific legal and financial principles. The correct answer to the question of who receives the amount due to the deceased partner is the executors of the estate. Let's delve into the rationale behind this.

1. Role of Executors

- Executors are individuals appointed to manage the estate of a deceased person.

- They are responsible for settling debts, distributing assets, and ensuring that the deceased's wishes (as expressed in a will, if available) are honored.

2. Legal Framework

- The law dictates that any outstanding dues owed to the deceased partner must be handled by their estate.

- This means that the amount due will not be directly paid to family members or friends but goes through the executors who manage the deceased partner's financial matters.

3. Distribution Process

- Once the executors receive the payment, they will settle any debts of the deceased.

- The remaining amount is then distributed to the rightful heirs or beneficiaries as per the laws of succession or the directions in the will.

4. Implications for Family and Friends

- Family members (e.g., spouse, children) and friends may ultimately benefit from the deceased partner's estate, but they do not receive direct payment from the partnership.

- This ensures that all financial obligations and legal processes are properly adhered to before any distribution to individuals connected to the deceased.

In summary, the amount due to a deceased partner is paid to their executors, who are legally tasked with managing the estate and ensuring proper distribution according to the deceased’s wishes and relevant laws.

To provide funds to pay to the retiring partner or to the representatives of a deceased partner, generally partners: - a)Create a Sinking Fund

- b)Create Joint Life Policy

- c)Create Reserve Fund

- d)Create a separate Bank Account

Correct answer is option 'B'. Can you explain this answer?

To provide funds to pay to the retiring partner or to the representatives of a deceased partner, generally partners:

a)

Create a Sinking Fund

b)

Create Joint Life Policy

c)

Create Reserve Fund

d)

Create a separate Bank Account

|

|

Shivam Chawla answered |

Joint Life Policy as a means of providing funds to retiring or deceased partners:

A Joint Life Policy is an insurance policy taken out on the lives of two or more partners, where the sum assured becomes payable on the death of one of the partners. This policy is often used by partnerships as a means of providing funds to pay out a retiring partner or to the representatives of a deceased partner.

Advantages of a Joint Life Policy:

1. Provides funds for payment to retiring or deceased partners: The sum assured under the Joint Life Policy becomes payable on the death of one of the partners. This ensures that there are funds available to pay out the retiring partner or the representatives of a deceased partner.

2. Premiums are tax-deductible: The premiums paid for the Joint Life Policy are tax-deductible expenses for the partnership.

3. Easy to set up: Setting up a Joint Life Policy is a simple process and can be done through an insurance broker.

4. Flexibility: The sum assured and the premium can be adjusted to suit the needs of the partnership.

5. Provides financial security: The Joint Life Policy provides financial security to the partners and their families in the event of the death of one of the partners.

Conclusion:

A Joint Life Policy is an effective means of providing funds to pay out a retiring partner or the representatives of a deceased partner. It provides financial security to the partners and their families and is a tax-deductible expense for the partnership.

A Joint Life Policy is an insurance policy taken out on the lives of two or more partners, where the sum assured becomes payable on the death of one of the partners. This policy is often used by partnerships as a means of providing funds to pay out a retiring partner or to the representatives of a deceased partner.

Advantages of a Joint Life Policy:

1. Provides funds for payment to retiring or deceased partners: The sum assured under the Joint Life Policy becomes payable on the death of one of the partners. This ensures that there are funds available to pay out the retiring partner or the representatives of a deceased partner.

2. Premiums are tax-deductible: The premiums paid for the Joint Life Policy are tax-deductible expenses for the partnership.

3. Easy to set up: Setting up a Joint Life Policy is a simple process and can be done through an insurance broker.

4. Flexibility: The sum assured and the premium can be adjusted to suit the needs of the partnership.

5. Provides financial security: The Joint Life Policy provides financial security to the partners and their families in the event of the death of one of the partners.

Conclusion:

A Joint Life Policy is an effective means of providing funds to pay out a retiring partner or the representatives of a deceased partner. It provides financial security to the partners and their families and is a tax-deductible expense for the partnership.

If Joint Life Policy in the Balance Sheet at surrender value, then the firm will be - a)Lose on the death of the partner

- b)Not get the value of Joint Life policy

- c)Gain on the death of the partner

- d)Continue the Joint Life Policy in the Balance Sheet even after the death of any of the partner

Correct answer is option 'C'. Can you explain this answer?