GMAT Exam > GMAT Questions > A firm’s default risk, the measurement ...

Start Learning for Free

A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.

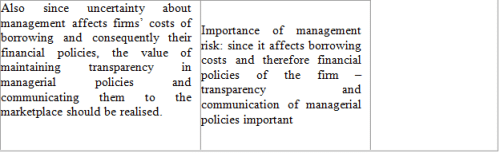

Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.

Which of the following statements would the author most likely agree with?

- a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.

- b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.

- c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.

- d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.

- e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.

Correct answer is option 'B'. Can you explain this answer?

| FREE This question is part of | Download PDF Attempt this Test |

Verified Answer

A firm’s default risk, the measurement of the chances of the eve...

Passage Analysis

Summary and Main Point

This is an Inference question. Four out of the five given answer choices will not follow from what is stated in the passage; these answer choices are INCORRECT. Select the answer choice that is bolstered by specific facts mentioned in the passage.

Answer Choices

A

Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.

Incorrect: Partial Scope

Although the author does state that uncertainty about a new CFO could affect a firm’s default risk and cost of borrowing, there is no information given to compare this effect with the impact resulting from uncertainty about a new CEO’s ability.

B

The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.

Correct

This information can be deduced on the basis of the following information:

In particular, when the new CEO is not considered an “heir apparent” prior to getting the position… the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions.

C

Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.

Incorrect: Out Of Scope

The author neither states nor suggests the cause and effect relationship stated in this choice.

D

As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.

Incorrect: Out Of Scope

Although it is given that the uncertainty decreases with the passage of time, the passage gives us no information to support that it decreases “considerably”.

E

By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.

Incorrect: Out Of Scope

There is no given information to deduce anything about a firm’s success in negotiating its term.

|

Explore Courses for GMAT exam

|

|

Similar GMAT Doubts

Top Courses for GMATView all

A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer?

Question Description

A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? for GMAT 2024 is part of GMAT preparation. The Question and answers have been prepared according to the GMAT exam syllabus. Information about A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? covers all topics & solutions for GMAT 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer?.

A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? for GMAT 2024 is part of GMAT preparation. The Question and answers have been prepared according to the GMAT exam syllabus. Information about A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? covers all topics & solutions for GMAT 2024 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer?.

Solutions for A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? in English & in Hindi are available as part of our courses for GMAT.

Download more important topics, notes, lectures and mock test series for GMAT Exam by signing up for free.

Here you can find the meaning of A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? defined & explained in the simplest way possible. Besides giving the explanation of

A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer?, a detailed solution for A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? has been provided alongside types of A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? theory, EduRev gives you an

ample number of questions to practice A firm’s default risk, the measurement of the chances of the event in which the company will be unable to make the required payments on its debt obligations, reflects not only the likelihood that the firm will have bad luck but also the risk that the firm’s managerial decisions will lead the firm to default. Such management risk occurs because the impact of management on the firm’s value is uncertain, and this uncertainty affects the market’s perception of a firm’s risk. Uncertainty about management is likely to be the highest when there is a new management team and should decrease over time as management’s ability becomes known more precisely. In particular, when the new CEO is not considered an “heir apparent” prior to getting the position, or when he comes from outside of the company, or when the new CEO is younger, the market is expected to perceive relatively high uncertainty about the CEO’s ability or future actions. Accordingly, it comes as no surprise that the CDS spread, a measure of a firm’s expected default risk, is about 35 basis points higher when a new CEO takes office than three years into his tenure. The CEO, however, is not the only member of the management team who is relevant for decision making in the firm. Chief Financial Officers (CFOs) have a large role in financial decision-making, so uncertainty about new CFOs could also affect the firm’s default risk and cost of borrowing.Now, a central feature of financial markets is that the interest rate a firm pays on debt increases with an increase in the market’s perception of the firm’s risk. This risk occurs because of factors that affect the value of the firm’s underlying assets and because of uncertainty about how these assets will be managed. The literature on debt pricing typically does not distinguish between these types of underlying risks. However, all risks, including those generated by uncertainty about management, affect the likelihood of default. Consequently, a rational market should incorporate managerial-generated uncertainty into its assessment of a firm’s risk when pricing its securities. Also since uncertainty about management affects firms’ costs of borrowing and consequently their financial policies, the value of maintaining transparency in managerial policies and communicating them to the marketplace should be realised.Which of the following statements would the author most likely agree with?a)Even though uncertainty about a new CEO’s ability has more impact on a firm’s default risk, uncertainty about a new CFO could affect the rate at which the firm is lent money and its default risk.b)The uncertainty about a new CEO is likely to be comparably lower when an expected candidate takes over the position vis-à-vis an unexpected one.c)Because the literature on debt pricing normally does not differentiate between the types of risks, sometimes the default risk is not calculated thoroughly.d)As the tenure of a new CEO progresses, the uncertainty regarding his ability decreases considerably.e)By maintaining transparency in managerial policies, a firm can successfully negotiate its terms in the market.Correct answer is option 'B'. Can you explain this answer? tests, examples and also practice GMAT tests.

|

|

Explore Courses for GMAT exam

|

|

Suggested Free Tests

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup