APT (Arbitrage Pricing Theory) | Management Optional Notes for UPSC PDF Download

Introduction

- The Arbitrage Pricing Theory (APT) is a framework for pricing assets that posits a relationship between an asset's expected returns and macroeconomic factors influencing its risk. Developed in 1976 by American economist Stephen Ross, the APT offers a multi-factor model for valuing securities based on their expected returns and associated risks.

- The APT aims to identify the fair market value of a security that may be temporarily mispriced due to inefficiencies in market behavior. It acknowledges that markets are not always perfectly efficient, leading to instances where assets are either overvalued or undervalued for a short period.

- However, the theory suggests that market forces will eventually correct these mispricings, restoring prices to their fair values. For arbitrageurs, these temporary mispricings present opportunities for virtually risk-free profits.

- Compared to the Capital Asset Pricing Model (CAPM), the APT offers a more flexible and sophisticated approach to asset pricing. It allows investors and analysts to tailor their analysis to specific market conditions and factors influencing asset prices. Nonetheless, implementing the APT can be challenging, as it requires extensive research to identify and quantify the various macroeconomic factors affecting asset prices.

Assumptions in the Arbitrage Pricing Theory

- The APT operates on a pricing model that considers multiple sources of risk and uncertainty, unlike the CAPM, which focuses solely on market risk. By examining various macroeconomic factors, the APT aims to capture the systematic risk associated with different assets.

- These factors provide investors with risk premiums to consider, as they represent risks that cannot be diversified away. According to the APT, investors will diversify their portfolios while selecting their preferred risk-return profiles based on the premiums associated with different macroeconomic factors.

- Risk-tolerant investors seek to exploit differences between expected and actual returns by engaging in arbitrage strategies, capitalizing on temporary mispricings in the market.

Arbitrage in the APT

- The APT posits a linear relationship governing asset returns, enabling investors to capitalize on deviations from this pattern through arbitrage strategies. Arbitrage involves concurrently buying and selling an asset across different markets to exploit minor pricing differences and secure a risk-free profit.

- However, the concept of arbitrage in the APT diverges from its traditional definition. In this context, arbitrage is not entirely devoid of risk, but it presents a favorable likelihood of success. The essence of the arbitrage pricing theory lies in providing traders with a framework to ascertain the theoretical fair market value of an asset. Armed with this valuation, traders then seek out marginal deviations from the fair market price and execute trades accordingly.

- For instance, if the APT-derived fair market value for stock A stands at $13, but the market momentarily drops its price to $11, a trader would purchase the stock anticipating a swift correction to the $13 level.

Mathematical Formulation of the APT

The Arbitrage Pricing Theory can be expressed as a mathematical model:

Where:

- ER(x) – Expected return on asset

- Rf – Riskless rate of return

- βn (Beta) – The asset’s price sensitivity to factor

- RPn – The risk premium associated with factor

Analyzing historical returns on securities involves employing linear regression analysis to correlate them with macroeconomic factors, thereby estimating beta coefficients for the arbitrage pricing theory formula.

Inputs in the Arbitrage Pricing Theory Formula

- While the Arbitrage Pricing Theory offers greater flexibility than the CAPM, it is also more intricate. The complexity of the arbitrage pricing model stems from the asset's price sensitivity to factor n (βn) and the risk premium associated with factor n (RPn).

- Before determining the beta and risk premium, investors must identify the factors they believe influence the asset's return, a process that can be accomplished through fundamental analysis and multivariate regression. One approach to calculating the factor's beta involves analyzing how it has affected numerous similar assets or indices, deriving an estimate through regression analysis.

- The risk premium can be calculated by equating the historical annualized return of similar assets or indices to the risk-free rate, then adding the product of the factor betas and factor premiums, and solving for the factor premiums.

Example

Let's consider a scenario where:

- You aim to apply the arbitrage pricing theory formula to a diversified portfolio of equities.

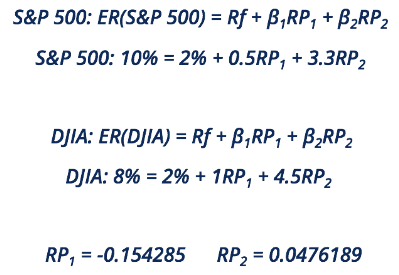

- The risk-free rate of return stands at 2%.

- Two similar assets or indices are the S&P 500 and the Dow Jones Industrial Average (DJIA).

- Two factors under consideration are inflation and gross domestic product (GDP).

- The betas of inflation and GDP for the S&P 500 are 0.5 and 3.3, respectively*.

- The betas of inflation and GDP for the DJIA are 1 and 4.5, respectively*.

- The expected return for the S&P 500 is 10%, and for the DJIA, it is 8%*.

- *Note: The betas and expected returns provided are for illustrative purposes only.

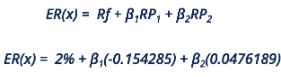

After determining the risk premiums, the results for our well-diversified portfolio would be as follows:

To calculate the expected arbitrage pricing theory return, plug in the regression results of how the betas have affected many similar assets/indices.

FAQs on APT (Arbitrage Pricing Theory) - Management Optional Notes for UPSC

| 1. What is the Arbitrage Pricing Theory (APT)? |  |

| 2. What are the assumptions in the Arbitrage Pricing Theory (APT)? | |

| 3. How is the Arbitrage Pricing Theory (APT) mathematically formulated? | |

| 4. What are some limitations of the Arbitrage Pricing Theory (APT)? | |

| 5. How does the Arbitrage Pricing Theory (APT) differ from the Capital Asset Pricing Model (CAPM)? | |

ppt

,shortcuts and tricks

,study material

,practice quizzes

,past year papers

,APT (Arbitrage Pricing Theory) | Management Optional Notes for UPSC

,Sample Paper

,Viva Questions

,MCQs

,Important questions

,video lectures

,Extra Questions

,Semester Notes

,mock tests for examination

,Free

,Objective type Questions

,Summary

,APT (Arbitrage Pricing Theory) | Management Optional Notes for UPSC

,APT (Arbitrage Pricing Theory) | Management Optional Notes for UPSC

,Exam

,Previous Year Questions with Solutions

;

APT (Arbitrage Pricing Theory) Free PDF Download

Importance of APT (Arbitrage Pricing Theory)

APT (Arbitrage Pricing Theory) Notes

APT (Arbitrage Pricing Theory) UPSC Questions

Study APT (Arbitrage Pricing Theory) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!