CAPM (Capital Asset Pricing Model) - 1 | Management Optional Notes for UPSC PDF Download

| Table of contents |

|

| Introduction |

|

| Passive and Active Management in Investment |

|

| The Capital Market Line (CML) |

|

| Leveraged Portfolios |

|

| Types of Risk |

|

Introduction

- To identify the optimal portfolio from a range of risky portfolios for an investor using the Capital Asset Pricing Model (CAPM), it is crucial to grasp the calculation of portfolio risk and return, as well as the role of correlation in diversifying portfolio risk, as discussed in Unit 10. This unit delves into the concept of the Capital Market Line, a specialized instance of the Capital Allocation Line. Understanding the CAPM model requires a clear comprehension of the differentiation between systematic and non-systematic risk, and why compensation is provided for undertaking systematic risk but not for non-systematic risk. Finally, the unit provides a detailed examination of CAPM, a straightforward model utilized for forecasting asset returns solely based on systematic risk.

- Our discussion begins with an exploration of the Capital Market Line and Capital Allocation Line. The unit introduces leveraged portfolios and delves into risk pricing in terms of systematic and non-systematic risk, emphasizing the decomposition of total risk into its constituent components. Subsequently, the Capital Asset Pricing Model is introduced to estimate the required return of equity or a portfolio, elucidating the relationship between CAPM and the Security Market Line. Additionally, we will explore the assumptions underlying CAPM, its practical applications, and its limitations.

Passive and Active Management in Investment

- An informationally efficient market is one that fully incorporates all publicly available information into its prices. In such markets, prices serve as unbiased estimates of all future discounted cash flows, meaning investors cannot expect to earn returns greater than the required rate of return for a given asset. Consequently, active asset management strategies aiming to outperform the market are futile, and the precision of an investor's cash flow and rate of return estimates becomes inconsequential.

- In an informationally efficient market, the optimal strategy is to base decisions on market-set prices, making investing in the market portfolio the simplest and most convenient approach. These portfolios, known as passive portfolios, or index funds, are constructed to replicate the performance of market indices such as the S&P 500 Index or the Nikkei 300. As they rely solely on market prices and capitalizations, they are cost-effective alternatives, requiring no technical analysis expertise for valuing securities. Passive investors typically engage in fundamental analysis for evaluating investment portfolios.

- In contrast, active investors possess greater confidence in their ability to estimate cash flows, growth rates, and discount rates, allowing them to form independent valuations of assets rather than relying solely on market valuations. Based on these valuations, assets are categorized as undervalued, fairly valued, or overvalued, with undervalued securities being overweighted in an actively managed portfolio compared to their weight in the benchmark index.

- Additionally, if short selling is permitted for a security, its weight may be zero or negative in the portfolio, leading to certain assets being underweighted relative to the benchmark index. Short selling, involving borrowing securities from a lender, selling them, and repurchasing them at a lower price in the future, is an active investment strategy. Open-ended mutual funds and hedge funds often employ active investment management techniques to evaluate investments and enhance investor returns.

The Capital Market Line (CML)

- In Unit 10, we examined the construction of a Capital Allocation Line (CAL) using various combinations of a risk-free asset and a risky portfolio with different weightings for each asset. In this section, we delve into a specific case of the CAL known as the Capital Market Line (CML), which arises when a risk-free asset is paired with the market portfolio to form an optimal risky portfolio for the investor.

- The risk-free asset (Rf) typically represents a debt security devoid of any risks such as default risk, inflation risk, liquidity risk, or interest rate risk. For instance, government-issued Treasury bills are often utilized as a benchmark to gauge the risk-free return, Rf. Now, let's shift our focus to the other crucial component of the CML: the market portfolio. For instance, the S&P 500 index may serve as a proxy for the market portfolio to estimate the expected return on the risky portfolio, denoted as the expected market return, E(Rm).

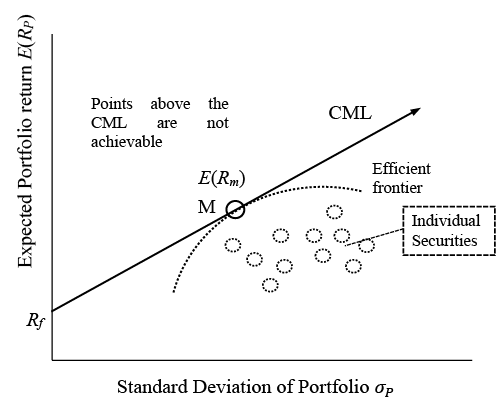

- The Capital Market Line is plotted with the standard deviation (σp), representing total risk, on the x-axis, and the expected return of the market portfolio, E(Rp), on the y-axis. Markowitz's efficient frontier plays a pivotal role in selecting the market portfolio for an investor. The point at which the line from the risk-free asset intersects the Markowitz efficient frontier determines the market portfolio. Graphically, points within the interior of the Markowitz efficient frontier are deemed inefficient, while points above the CML are unattainable for an investor given the available resources. Portfolios lying below the CML are considered inefficient because they either offer the same level of return with higher risk or lower returns with the same level of risk.

- The optimal combination of risky assets, as determined by the point of tangency between the CML and the Markowitz efficient frontier, represents the optimal risky portfolio, commonly known as the market portfolio. This combination is determined based on market prices and capitalizations, culminating in an optimal allocation of risky assets.

Figure 1: Capital Market Line

- The intercept of the CML on the y-axis is the risk-free return (Rf) and the slope is positive based on the risk and returns relationship which is considered positive. Higher risk gives higher returns. The expected market return through which CML passes is represented by E(Rm). Under the capital market theory, we know that an investor will not be able to achieve any point above the CML as it is not achievable and any point below the CML because the points on the CML are dominated by the points below the CML. They are considered inferior to any point on the CML.

- The risk and return of the portfolio on the CML can be estimated by using the return and risk formulas for a two-asset portfolio: 𝑅𝑝 = wA𝑟A + wB 𝑟B

- Where 𝑟A an𝑑 𝑟B is the return of Asset A and Asset B respectively and weight wA and wB of Asset A and Asset B respectively in the portfolio. The standard deviation of the two asset portfolios is written as:

- Correlation between the two returns (pAB) and the standard deviations of the two assets namely, σA and σB. In case an asset is a risk-free asset and the other asset is risky, the portfolio of these two assets with a portfolio expected return, Rp, risk-free return, rf, and risky asset return, E(ri), can be constructed as follows:

Rp = wArf + wBE(rj)Equation (1) - The sum of the weight of a risk-free asset and the weight of the risky asset is 1. So, wB = 1-wA.

- Because the risk-free asset has no risk, that is, σf = 0, the first and third terms in the formula for variance are zero.

- By taking the square root of both sides, the standard deviation for a portfolio of a risk-free asset and risky asset is given by:

The observations from the above formula are:

The observations from the above formula are:

- The CML has a positive slope because as the market’s risk of the risky portfolio increases, the market return will also increase. Certainly, the market return is larger than the risk-free return. As the amount of the total investment in the market assets increases, both standard deviation (risk) and expected return will also increase.

Leveraged Portfolios

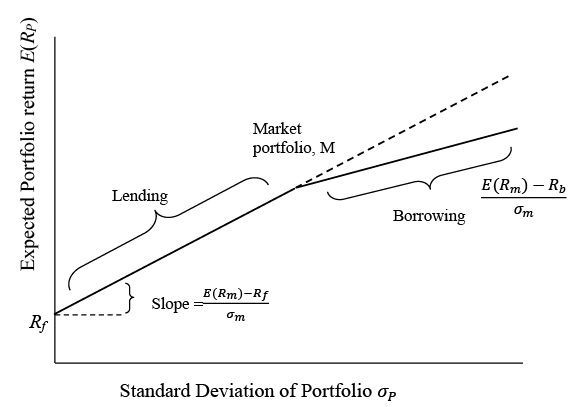

- Figure 2 depicts portfolios with varying levels of investment, ranging from 0 percent to 100 percent in the market asset, with the remainder allocated to risk-free assets such as T-bills. The line connecting the risk-free asset (Rf) and the market portfolio (M) illustrates these portfolios along with their corresponding investment levels. At the risk-free point (Rf), an investor allocates all their wealth into risk-free securities, earning a risk-free rate on their investment. Thus, from Rf to point M, there is no risk involved when investing all wealth in risk-free securities. Portfolios between Rf and M, where a combination of the risk-free asset and the market portfolio can be achieved, are termed "lending" portfolios. At point M, the investor holds the market portfolio without lending any money at the risk-free rate.

- Assuming different lending and borrowing rates, with the borrowing rate (Rb) being higher than the lending rate (Rf), investors can lend at Rf, a rate lower than the borrowing rate Rb. Consequently, the slope of the Capital Market Line (CML) will vary due to these different rates, resulting in a non-linear line. The slope to the left of M will be steeper than that to the right of M. This distinction arises because points between Rf and M utilize the lending rate, while those to the right of M use the borrowing rate. Symbolically, the slopes on both sides are as follows:

Figure 2: Leveraged Portfolios on CML

The equations for the two lines are given below. To the left of M, when the weight of the risk-free asset is zero or positive:

When negative or zero investment occurs in the risk-free assets i.e., to the right of M, the weight of the market portfolio is positive or higher:

The distinction between the two equations lies in the utilization of borrowing and lending interest rates. A risk-averse investor might opt for a leveraged portfolio, enabling the augmentation of risk by borrowing or investing more than 100 percent in the passive portfolio. Consequently, all passive portfolios will reside on the kinked CML, offering a selection of leveraged portfolios. Regardless of whether the investment in the risk-free asset is positive (lending), zero (neither lending nor borrowing), or negative (borrowing), passive portfolios can be selected from the kinked CML in all the aforementioned scenarios.

Types of Risk

- Risk plays a crucial role in portfolio construction, and while correlation and standard deviation are essential metrics for measuring overall risk, diversification can help mitigate the risk associated with assets that have less than perfect correlation. This results in the individual asset's risk being greater than its risk within a diversified portfolio. So far, we have broadly discussed risk within a portfolio, but now we will delve into the types of risk, which vary depending on the situation, and determine which types of risk can be diversified.

Total portfolio risk can be broken down into two main categories: systematic and non-systematic risks.

1. Non-systematic Risk

- Non-systematic risk, a component of total risk, is specific to a particular industry and impacts only those assets associated with that industry or class. This type of risk, also known as company-specific, industry-specific, diversifiable, or idiosyncratic risk, is localized and does not affect assets outside of its respective asset class. For instance, events such as an airline crash will primarily affect securities in the airline industry, while the failure of a drug trial will impact assets in the pharmaceutical industry. Consequently, events within a specific industry directly influence companies and possibly entire industries within that sector, without affecting unrelated securities.

- To mitigate non-systematic risk, investors can diversify their portfolios by purchasing securities from different industries, ensuring that events in one industry do not significantly impact others. Through diversification, investors can create portfolios with assets that have low correlation, effectively reducing overall portfolio risk. It is important to note that investors are not compensated with higher returns for bearing non-systematic risk, as this type of risk can be mitigated through portfolio diversification.

2. Systematic Risk

- Systematic Risk, also known as non-diversifiable or market risk, constitutes the portion of total risk that cannot be mitigated through diversification. These risks affect the entire market or economy, resulting in widespread impact across all assets and industries. For instance, events like the COVID-19 pandemic have demonstrated how such risks can affect virtually all sectors simultaneously. Similarly, economic slowdowns can have broad-reaching effects on financial markets and securities across industries.

- Unlike non-systematic risk, systematic risks cannot be diversified away, regardless of their intensity. Investors are required to bear these risks, and higher levels of systematic risk are typically compensated with higher returns. Factors such as changes in interest rates, inflation rates, economic cycles, political instability, and natural disasters influence systematic risk, and their effects are inherent in the overall market.

- While systematic risk cannot be avoided, its impact can be amplified or diminished. Leveraging or including poorly correlated securities in a portfolio can magnify or mitigate the effects of systematic risk, respectively. The total risk of a portfolio is the sum of systematic risk and non-systematic risk, with systematic risk being compensated through returns.

- In an efficient market, no additional reward is earned for bearing non-systematic risk, as it can be diversified away. Therefore, investors must diversify their portfolios across different industries, countries, and asset classes to offset low returns in one area with higher returns in another, ultimately reducing overall portfolio risk.

- However, investors must demand compensation for bearing systematic risk, as it cannot be diversified. Therefore, investments must offer returns commensurate with the level of systematic risk involved. Systematic risk is priced into returns, while there are no additional returns for bearing non-systematic or diversifiable risk. Hence, risk-averse investors should hold well-diversified portfolios to minimize exposure to non-diversifiable risk.

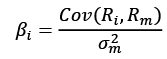

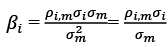

- Before delving into the Capital Asset Pricing Model (CAPM), let's consider the Single-Index Model, which revolves around a single factor: beta. Beta measures an asset's sensitivity to overall market movements and is calculated as the covariance of the asset's return with the market return, divided by the variance of the market return.

- Asset Beta is the product of the correlation between the asset and the market, standard deviation and the standard deviation of the asset divided by the variance of return from the market.

- In other words, Beta is also defined as the product of the correlation between an asset and the market and the standard deviation of the asset divided by the standard deviations of return from the market.

- The aforementioned statements illustrate that beta serves as a measure of an asset's systematic risk, which remains unaffected by diversification. Beta is computed using the historical returns of both the asset and the market to determine the necessary variances and correlations. The sign of beta indicates the direction of movement between the asset's returns and those of the market. A positive beta suggests that the asset's returns align with the overall market trend, while a negative beta indicates an inverse relationship.

- In simpler terms, a positive beta implies that the asset's returns move in tandem with the market, whereas a negative beta suggests that the asset's returns move counter to the market trend. For a risk-free asset, there is no systematic risk present, resulting in a beta value of zero. Additionally, the covariance between the risk-free asset and other assets is also zero, signifying that the asset's returns do not correlate with market trends.

FAQs on CAPM (Capital Asset Pricing Model) - 1 - Management Optional Notes for UPSC

| 1. What is the difference between passive and active management in investment? |  |

| 2. What is the Capital Market Line (CML)? | |

| 3. What are leveraged portfolios? | |

| 4. What are the types of risk in investment? | |

| 5. What is the Capital Asset Pricing Model (CAPM)? | |

practice quizzes

,CAPM (Capital Asset Pricing Model) - 1 | Management Optional Notes for UPSC

,video lectures

,mock tests for examination

,ppt

,Exam

,Previous Year Questions with Solutions

,MCQs

,shortcuts and tricks

,Objective type Questions

,Sample Paper

,Semester Notes

,CAPM (Capital Asset Pricing Model) - 1 | Management Optional Notes for UPSC

,past year papers

,Summary

,Extra Questions

,Viva Questions

,Important questions

,Free

,CAPM (Capital Asset Pricing Model) - 1 | Management Optional Notes for UPSC

,study material

;

CAPM (Capital Asset Pricing Model) - 1 Free PDF Download

Importance of CAPM (Capital Asset Pricing Model) - 1

CAPM (Capital Asset Pricing Model) - 1 Notes

CAPM (Capital Asset Pricing Model) - 1 UPSC Questions

Study CAPM (Capital Asset Pricing Model) - 1 on the App

|

© EduRev

|

Education Revolution

|

|