Financial Statements of a Company (Part - 2) | Accountancy Class 12 - Commerce PDF Download

Page No. 1.69

Question:26

Prepare Balance Sheet of VT Ltd. as at 31st March 2019, from the following information as per Schedule III, Part I of the Companies Act, 2013:

Solution:

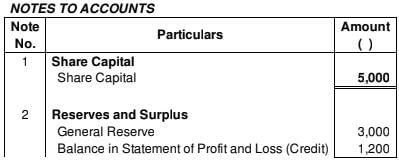

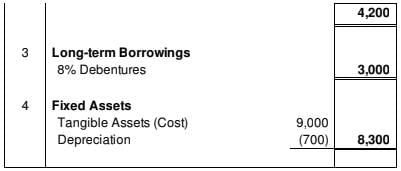

Question:27

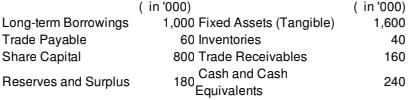

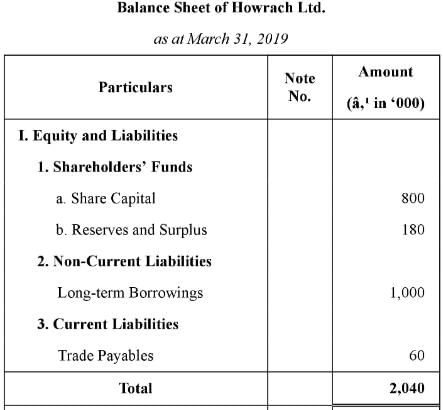

From the following information extracted from the books of Howrach Ltd., prepare Balance Sheet of the company as at 31st March, 2019 as per Schedule III of the Companies Act, 2013:

Solution:

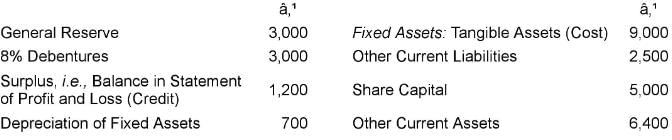

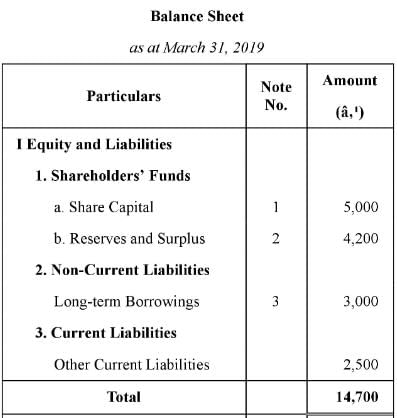

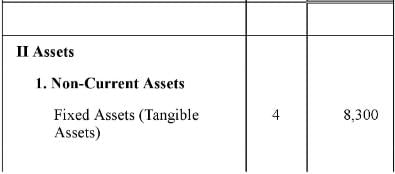

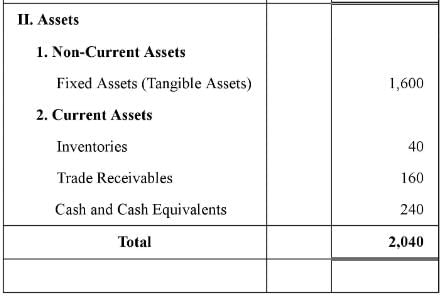

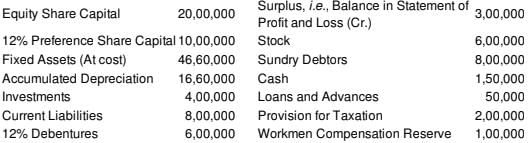

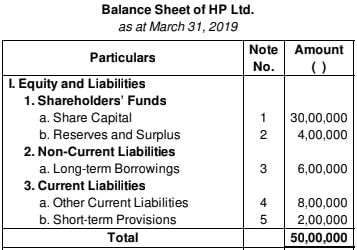

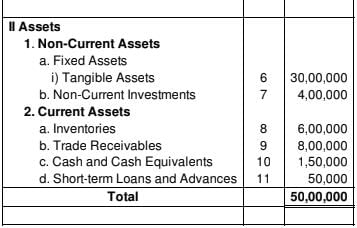

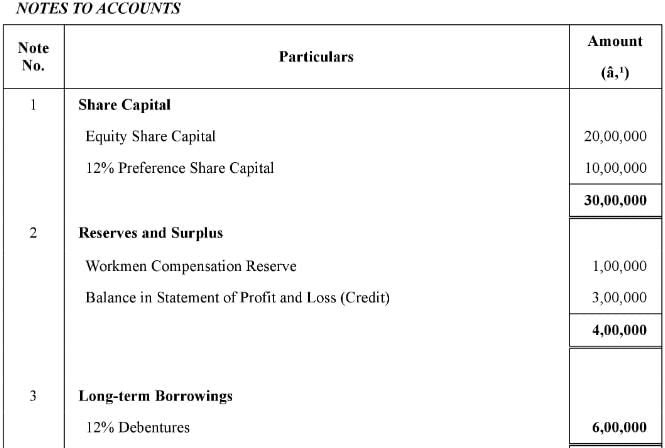

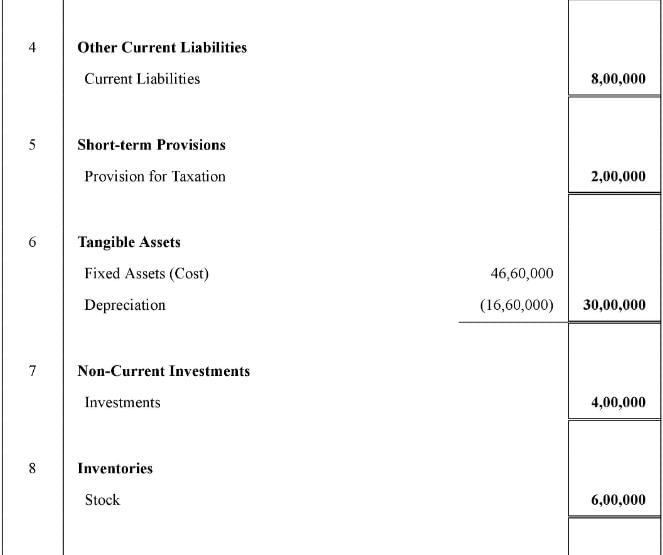

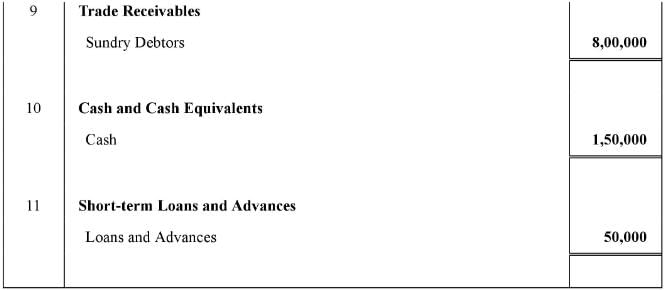

Question:28

Prepare Balance Sheet of HP Ltd. as at 31st March, 2019 from the following information:

Solution:

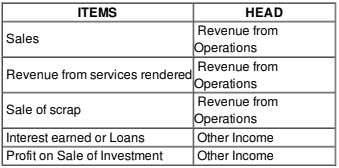

Question:29

Under which head following revenue items of a non-financial company will be classified or shown:

(i) Sales; (ii) Revenue from Services Rendered; (iii) Sale of Scrap; (iv) Interest Earned on Loans; and (v) Gain (profit) on Sale of Investments?

Solution:

Page No. 1.70

Question:30

Under which head following revenue items of a financial company will be classified or shown:

(i) Gain (Profit) on Sale of Building; (ii) Revenue from Project Consultancy Rendered; (iii) Sale of Scrap; (iv) Interest earned on Loans; and (v) Gain (Profit) on sale of Investments?

Solution:

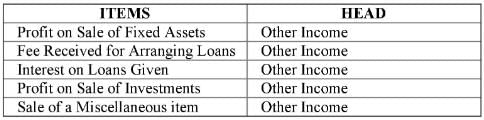

Question:31

Under which head following revenue items of non-financial company will be classified or shown:

(i) Gain (Profit) on Sale of Fixed Asset; (ii) Fee Received for Arranging Loans; (iii) Interest on Loans Given; (iv) Gain (Profit) on Sale of Investments and (v) Sale of Miscellaneous Items?

Solution:

Question:32

Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials 5,00,000; Purchase of Materials 25,00,000; and Closing Inventory of Materials 4,00,000.

Solution:

Cost of Materials Consumed = Opening Inventory of Materials + Purchase of Materials

- Closing Inventory of Materials

= 5,00,000 + 25,00,000 - 4,00,000 = 26,00,000

∴ Cost of Materials Consumed is Rs 26,00,000

Question:33

Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials 2,50,000; Finished Goods 1,00,000; Closing Inventory of Materials 2,25,000; Finished Goods 75,000; Raw Material purchased during the year 15,00,000.

Solution.

Cost of Materials Consumed = Opening Inventory of Materials + Purchase of Materials

- Closing Inventory of Materials

= 2,50,000 + 15,00,000 - 2,25,000 = 15,25,000

∴ Cost of Materials Consumed is 15,25,000

Note: Opening Inventory of Finished Goods and Closing Inventory of Finished Goods will not be considered as these are shown under Change in Inventory of Finished Goods.

Question:34

Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials 3,50,000; Finished Goods 75,000; Stock-in-Trade 2,00,000; Closing Inventory of:

Materials 3,25,000; Finished Goods 85,000; Stock-in-Trade 1,50,000; Purchases during the year: Raw Material 17,50,000; Stock-in-Trade 9,00,000.

Solution:

Cost of Materials Consumed = Opening Inventory of Materials + Purchase of Materials

- Closing Inventory of Materials

= 3,50,000 + 17,50,000 - 3,25,000 = 17,75,000

∴ Cost of Materials Consumed is 17,75,000

Note: Opening Inventory of Finished Goods and Closing Inventory of Finished Goods will not be considered as these are shown under Change in Inventory of Finished Goods. Also, Opening, Closing and Purchases of Stock-in-Trade are not considered as they are not part of cost of materials consumed.

Question:35

From the following information, calculate Change in Inventory of Finished Goods: Opening Inventory and Closing Inventory of Finished Goods 2,00,000 and 1,75,000 respectively.

Solution:

Rs 25,000 will be shown in the Statement of Profit and Loss against Change in Inventories of Finished Goods.

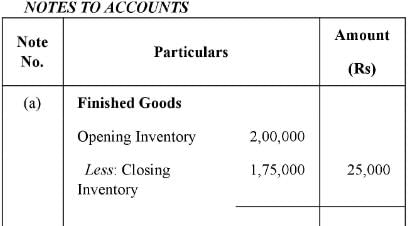

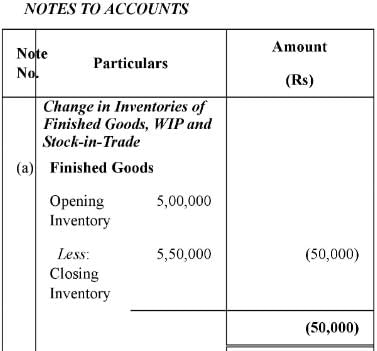

Question:36

From the following information, calculate Change in Inventory of Finished Goods: Opening Inventory and Closing Inventory of Finished Goods 2,50,000 and 2,00,000 respectively.

Solution:

Rs 50,000 will be shown in the Statement of Profit and Loss against Change in Inventories of Finished Goods.

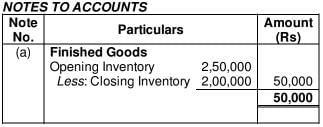

Question:37

From the following information, calculate Change in Inventory of Work-in-Progress: Opening and Closing Work-in-Progress 1,00,000 and 1,15,000 respectively.

Solution:

(Rs 15,000) will be shown in the Statement of Profit and Loss against Change in Inventories of Work-in-Progress.

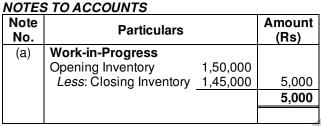

Question:38

From the following information, calculate Change in Inventory of Work-in-Progress: Opening and Closing Work-in-Progress 1,50,000 and 1,45,000 respectively.

Solution:

Rs 5,000 will be shown in the Statement of Profit and Loss against Change in Inventories of Work-in-Progress.

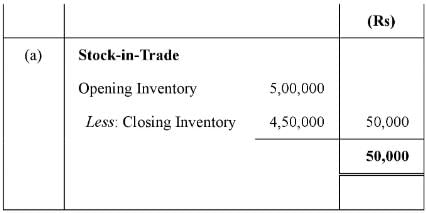

Question:39

From the following information, calculate Change in Inventory of Stock-in-Trade: Opening and Closing Stock-in-Trade 5,00,000 and 4,50,000 respectively.

Solution:

Rs 50,000 will be shown in the Statement of Profit and Loss against Change in Inventories of Stock-in-Trade.

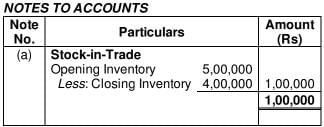

Question:40

From the following information, calculate Change in Inventory of Stock-in-Trade: Opening and Closing Stock-in-Trade 5,00,000 and 4,00,000 respectively.

Solution:

Rs 1,00,000 will be shown in the Statement of Profit and Loss against Change in Inventories of Stock-in-Trade.

Page No. 1.71

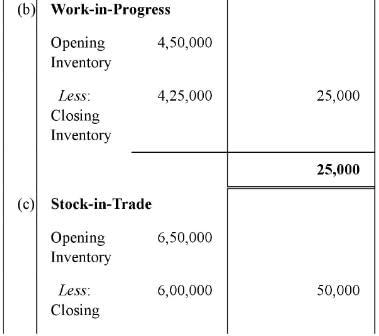

Question:41

From the following information of Hospitality Ltd. for the year ended 31st March, 2018, calculate amount that will be shown in the Note to Accounts on Changes in inventiories of Finished Goods, WIP and stock-in-Trade:

Solution:

Rs 25,000 will be shown in the Statement of Profit and Loss against the Change in Inventories of Finished Goods, Work-in-Progress and Stock-in-Trade.

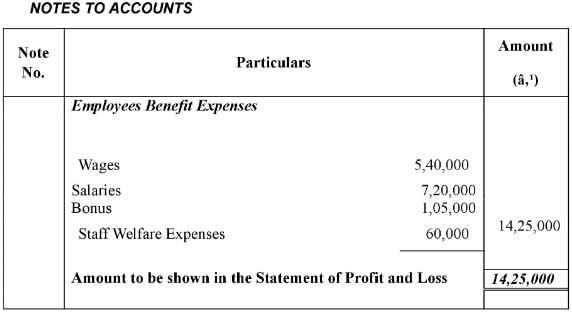

Question:42

From the following information compute the amount to be shown in Note to Accounts on Employees Benefit Expenses: Wages 5,40,000; Salaries 7,20,000; bonus 1,05,000; Staff Welfare Expenses 60,000 and Business Promotion Expenses 50,000.

Solution:

*Amount spent on promotion of business is not included in Employees Benefit Expenses.

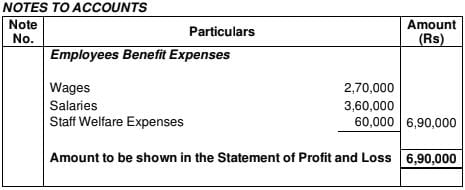

Question:43

From the following information, prepare Note to Accounts on Employees Benefit Expenses: Wages 2,70,000; Salaries 3,60,000; Staff Welfare Expenses 60,000; Printing and Stationery Expenses 20,000 and Business Promotion Expenses 50,000.

Solution:

*Amount spent on promotion of business and printing & Stationary expenses are not included in Employees Benefit Expenses.

Question:44

Out of the Following, identify the items that are shown in the Note to Accounts on Finance Costs:

(i) Interest paid on Borrowing from prince Finance Ltd.;

(ii) Interest paid on Term Loan to Bank;

(iii) Interest paid on Public Deposits;

(iv) Loss on Issue of Debentures Written off; and

(v) Bank Charges.

Solution:

Items that will be shown in the Notes to Accounts on Finance Costs are:

i. Interest paid on Borrowings from Prince Finance Ltd.;

ii. Interest paid on Term Loan to Bank;

iii. Interest paid on Public Deposits;

iv. Loss on Issue of Debentures written off.

The Bank charges are not shown under Finance Costs but under ‘Other Expenses’, as they are expenses for the services availed from the bank.

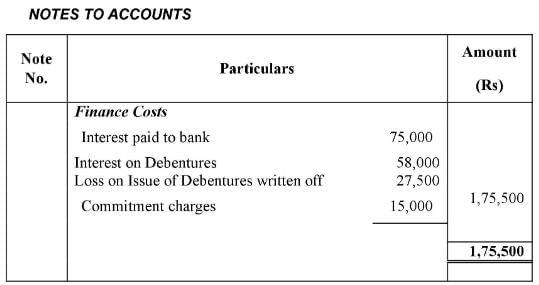

Question:45

From the following information, prepare Note to Accounts on Finance Costs: Interest paid to Bank 75,000; Interest on Debentures 58,000; Loss on issue of Debentures written off 27,500; and Commitment Charges 15,000.

Solution:

Question:46

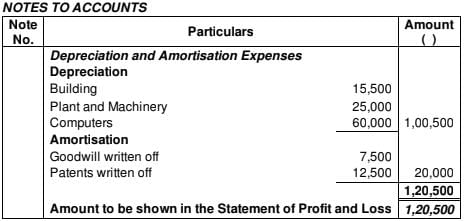

From the following information of Best Marketing Ltd. for the year ended 31st March, 2019 prepare Note to Accounts on Depreciation and Amortisation Expenses: Depreciation on: Building 15,500; Plant and Machinery 25,000; Computers 60,000; Goodwill written off 7,500; Patents written off 12,500.

Solution:

Question:47

Identify which of the following items will be shown in the Note to Accounts on Other Expenses? (i) Salaries; (ii) Postage Expenses; (iii) Telephone and Internet Expenses; (iv) Rent for warehouse; (v) Carriage Inwards; (vi) Depreciation on computers; (vii) Computer Software amortised; (viii) Computer Hiring Charges; (ix) Audit fee; (x) Bonus.

Solution:

Items that will be shown in the Notes to Accounts on ‘other expenses’ are

(ii) Postage Expenses;

(iii)Telephone and Internet Expenses;

(iv) Rent for warehouse;

(v) Carriage Inwards;

(viii) Computer Hiring charges;

(ix) Audit fee

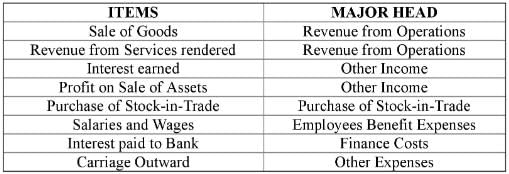

Question:48

Under which line item (major head) of the Statement of Profit and Loss of non-financial company will the following be shown:

(i) Sale of Goods; (ii) Revenue from Services Rendered; (iii) Interest Earned; (iv) Gain (Profit) on Sale of Assets; (v) Purchases of Stock-in-Trade; (vi) Salaries and Wages; (vii) Interest paid to Bank; (viii) Carriage Outward?

Solution:

Question:49

Under which line item (major head) of the Statement of Profit and Loss of a financial company will the following be shown:

(i) Interest on Loans Given: (ii) Gain (Profit) on Sale of Securities; (iii) Loss on Sale of Fixed Assets; (iv) Interest paid on Deposits; (v) Depreciation on Computers; (vi) Goodwill Written off; (vii) Commission paid for Deposit Mobilisation; and (viii) Repairs Expenses?

Solution:

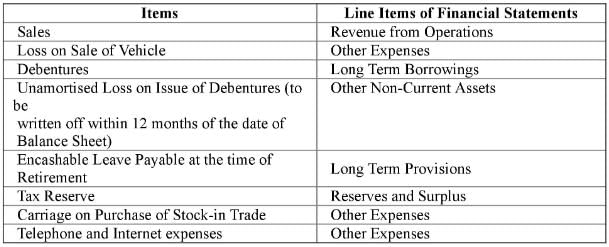

Question:50

Under which line item of the financial statements following items will be shown:

(i) Sales; (ii) Loss on Sale of Vehicle; (iii) Debentures; (iv) Unamortised Loss on Issue of Debentures (to be written off within 12 months of the date of Balance Sheet); (v) Encashable Leave Payable at the Time of Retirement; (vi) Tax Reserve; (vii) Carriage on Purchases of Stock-in-Trade; and (viii) Telephone and Internet Expenses?

Solution:

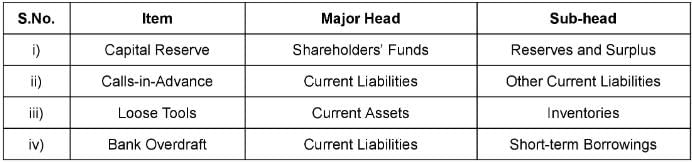

Question:51

State under which major headings and sub-headings the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act, 2013:

(i) Capital Reserve;

(ii) Calls-in-Advance;

(iii) Loose Tools; and

(iv) Bank overdraft.

Solution:

|

42 videos|199 docs|43 tests

|

FAQs on Financial Statements of a Company (Part - 2) - Accountancy Class 12 - Commerce

| 1. What are the key financial statements of a company? |  |

| 2. What information does the income statement provide? | |

| 3. How does the balance sheet reflect a company's financial position? | |

| 4. What is the purpose of the cash flow statement? | |

| 5. Why are financial statements important for investors and stakeholders? | |

Financial Statements of a Company (Part - 2) | Accountancy Class 12 - Commerce

,Sample Paper

,Viva Questions

,Semester Notes

,MCQs

,Extra Questions

,Financial Statements of a Company (Part - 2) | Accountancy Class 12 - Commerce

,Previous Year Questions with Solutions

,mock tests for examination

,practice quizzes

,Objective type Questions

,Important questions

,past year papers

,Exam

,ppt

,Free

,Summary

,shortcuts and tricks

,Financial Statements of a Company (Part - 2) | Accountancy Class 12 - Commerce

,study material

,video lectures

;

Financial Statements of a Company (Part - 2) Free PDF Download

Importance of Financial Statements of a Company (Part - 2)

Financial Statements of a Company (Part - 2) Notes

Financial Statements of a Company (Part - 2) Commerce Questions

Study Financial Statements of a Company (Part - 2) on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!