Fund Flow Analysis | Management Optional Notes for UPSC PDF Download

| Table of contents |

|

| Fund Flow Analysis |

|

| Sources of Funds |

|

| Uses (Applications) of Funds |

|

| Preparation of Fund Flow Statement |

|

Fund Flow Analysis

- A review of the fluctuations in current assets and current liabilities, i.e., working capital, provides insights into the changes in working capital. Beyond understanding the increase or decrease in working capital, there is a need to identify where the augmented working capital has been allocated or from where funds have been redirected in the case of a decrease.

- While the profit and loss account offers some insights into operational results and their impact on funds, a comprehensive understanding requires integrating the information from both the profit and loss account and the balance sheet. This integration is achieved through the preparation of a statement that outlines the changes in the financial position, commonly known as the fund flow statement or statement of sources and application of funds.

- The fund flow statement elucidates the pathways through which funds move within the organization. It delineates the sources from which funds were procured and the purposes for which they were utilized.

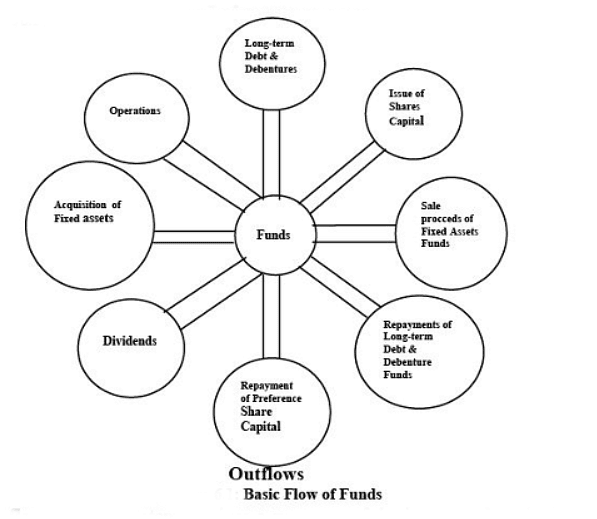

- The fund flow statement typically consists of two main sections: sources of funds (or inflows) and uses of funds (or outflows) during a specific period. The section outlining the sources of funds provides a summary of transactions that collectively contributed to the increase in working capital. Conversely, the uses of funds section encompasses transactions that led to a reduction in working capital. The fundamental structure of these flows is illustrated in Figure below.

- The funds flow statement provides a concise overview of the consequences of different managerial choices. It serves as a reflection of financing strategies, investment decisions, acquisition and disposal of fixed assets, profit distribution policies, and the overall effectiveness of operations.

Sources of Funds

- We've observed that working capital is essential for funding the part of current assets not covered by current liabilities. Additionally, we noted that the investments represented by current assets are converted into cash during the operating cycle, implying a need for financing for one such cycle. Typically, every unit of investment in working capital is converted into cash at the end of the cycle, with added value in terms of profits.

- In the search for sources of working capital, one of the most crucial sources is "internal generation." The concept of internal sources presupposes the existence of something "external."

Internal Sources

- Excess Working Capital: Assessing the need for working capital involves evaluating whether existing working capital is sufficient. Excess working capital, if available, serves as an internal source.

- Sale of Non-Current Assets: Disposing of non-current assets that are no longer useful can generate additional working capital. However, this is not a regular and ongoing source of funds.

- Profits from Operations: Every profitable sale brings funds exceeding the expenditures on the goods sold. However, when measuring profits, revenue is matched against all expenses, whether or not they involve the use of funds in the current period. To assess the actual funds generated from current operations, adjustments need to be made, such as adding back items like depreciation.

Funds From Operations

- Referring to Illustration 1, the profit and loss account of TIL indicates that operations have contributed a gross addition of Rs. 360 million to funds during the period. These funds represent the proceeds from the sale of goods and services by the company, along with other incomes.

- It's understood that a portion of these funds is allocated for covering input costs such as materials, personnel, and other operational expenses. Additionally, there is a need to fulfill interest commitments and cover the costs associated with the depreciation of machinery and equipment. Notably, the expenditure on machinery and equipment (Depreciation) is an item that does not require the use of funds in the current period.

Illustration 1:

Thus, funds provided from operations are in fact the revenues earned from operations (as also non-operating incomes) less all immediate costs of goods sold requiring use of funds. In other words, it is net income or profit after taxes plus all the non-fund expenses, such as depreciation and amortisation and adjusted for non-operating incomes and expenses.

The following statement would show funds from operations of TIL as follows:

External Sources

External sources of funds refer to resources obtained from outside the organization to enhance the availability of funds for various purposes, as will be discussed later. Typically, there are only two methods for accomplishing this:

- By contributing or securing additional capital.

- Through increased long-term borrowing.

It's important to note that short-term creditors are not considered a source of funds in this context. As we've defined funds as "current assets less current liabilities," working capital denotes a long-term investment in current assets, meaning short-term borrowing does not contribute to an increase in working capital.

The sources of funds, as usually presented in the fund flow statement, are enumerated below:

Uses (Applications) of Funds

A business typically requires additional funds for two primary purposes:

- Financing Additional Fixed Assets: The necessity for having sufficient fixed facilities to conduct business is evident. The investments made in the shop, furniture, and fixtures establish the facilities needed for business operations. These fixed assets determine the business's production capacity and service provision capabilities. Business expansion beyond a certain capacity is restricted by the facilities created through fixed assets. In manufacturing, it could be plant capacity, for a transport company, it might be the tonnage of vehicles, ships, or wagons, and for businesses like show business and airlines, it could be seating capacity. Any increase in such capacity demands additional investment in fixed assets, typically assessed based on its potential to reduce current costs or increase current output.

- Financing Additional Working Capital: Additional working capital is essential to fund the heightened inventory holding, extended credit to customers, and increased cash holding requirements. It's important to note that part of this working capital requirement is often financed by current creditors.

In scenarios where a firm invests in a new shop or expands an existing one, additional funds are needed for both investing in fixed assets and sustaining an elevated level of current assets. Notably, when additional investments are made in non-current assets, the funds (working capital) available need to be utilized unless specific arrangements are made for their financing. Conversely, the sale of non-current assets provides funds or generates sources of funds.

- The common applications of funds are summarized as follows:

- Acquisition of new non-current assets (fixed assets).

- Replacement of non-current debt (loans).

- Payment of dividends.

- Increase in the balance of working capital (current assets - current liabilities).

In the event of unsuccessful trading or business operations, funds may be used rather than provided. The uses of funds, typically outlined in the fund flow statement, are enumerated below.

Preparation of Fund Flow Statement

To create a comprehensive Fund Flow Statement, we will further elaborate on Illustration 6.2. Utilizing information derived from a comparative balance sheet and profit and loss account, we can extract most of the essential details needed for the fund flow statement. As we've learned, changes in net-working capital result from alterations in non-working capital items, evident in the summarized balance sheet of TIL (Table 6.2).

In the specified period from January 1 to December 31, 2004, the net working capital increased by Rs. 27 million. This implies that the working capital from non-current sources should surpass non-current uses by Rs. 27 million.

The summarized balance sheet illustrates the net change in each account without distinguishing between increases and decreases. For instance, the value of furniture and fixtures has shown a net increase of Rs. 5.90 million, indicating an application of funds. In reality, this account served as both a source and an application of funds. The purchase of new furniture and fixtures amounted to Rs. 7.90 million (a use of funds), while the sale of existing furniture and fixtures, originally costing Rs. 2 million with accumulated depreciation of Rs. 1 million, acted as a source of funds. Despite being a dual-role account, the net result leaned toward a 'use of funds' due to the larger magnitude of the purchase transaction compared to the sale. Notes:

Notes:

- Furniture and fixtures costing Rs. 2 million with an accumulated depreciation of Rs. 1 million is sold for cash at Rs. 2 million.

- Dividend paid during the year amounted to Rs. 2.25 million.

If we are to construct a statement showing sources and uses of funds during the year, we need additional information. Some of this additional information is available from the profit and loss account and the appropriation of net income. Some other information like sales proceeds of assets will have to be obtained from the other records of the company.

* Net income has been obtained by deducting the previous year’s balance of Reserves and Surplus from the current year’s balance i.e. 97.69 minus 62.69 = 35 million. To this, the proposed dividend for the current year of Rs. 2.25 million has been added (as it must have been taken into account while determining the net income to be transferred to Reserves and Surplus).

FAQs on Fund Flow Analysis - Management Optional Notes for UPSC

| 1. What is fund flow analysis? |  |

| 2. What are the sources of funds in fund flow analysis? | |

| 3. What are the uses or applications of funds in fund flow analysis? | |

| 4. How is a fund flow statement prepared? | |

| 5. How can fund flow analysis be beneficial for organizations? | |

|

Dec 05, 2024 Last updated |

|

Explore Courses for UPSC exam

|

|

Fund Flow Analysis | Management Optional Notes for UPSC

,Viva Questions

,study material

,ppt

,Objective type Questions

,Extra Questions

,Semester Notes

,MCQs

,Free

,Sample Paper

,video lectures

,Fund Flow Analysis | Management Optional Notes for UPSC

,Summary

,Fund Flow Analysis | Management Optional Notes for UPSC

,mock tests for examination

,Previous Year Questions with Solutions

,past year papers

,Important questions

,practice quizzes

,shortcuts and tricks

,Exam

;

Fund Flow Analysis Free PDF Download

Importance of Fund Flow Analysis

Fund Flow Analysis Notes

Fund Flow Analysis UPSC Questions

Study Fund Flow Analysis on the App

|

© EduRev

|

Education Revolution

|

Follow Us

|