PIB Summary- 30th June, 2021 | PIB (Press Information Bureau) Summary - UPSC PDF Download

Goods and Services Tax (GST)

Context: GST completed four years of implementation.

Goods & Services Tax (GST) - One Nation One Tax

Why was GST in News?

- GST (one hundred and twenty-second-122 constitutional amendment) bill has finally, been passed in the Lok Sabha and the Rajya Sabha.

- It heralds the first significant step towards the indirect tax reform in India in the last thirty years

What is GST?

- It is a tax levied when a consumer buys a good or service. It is meant to be a single, comprehensive tax that will subsume all the other smaller indirect taxes on consumption like service tax, etc.

- It is a single tax on the supply of goods and services, right from the manufacturer to the end consumer

- This is how it is done in most developed countries. More than 160 countries have implemented this system of taxation.

- GST does not tax or get into specific commodities.

Mechanism of GST:

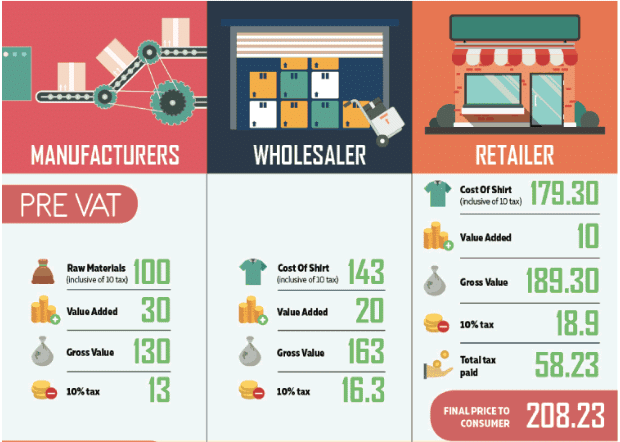

Stage 1:-

- Let’s consider a manufacturer of gears.

- Let’s say he buys raw material worth Rs 100, a sum that includes a tax of Rs 10.

- With the raw materials, he manufactures a gear

- In the process of creating the gear, the manufacturer adds value to the materials he started out with.

- Let us take this value added by him to be Rs 30.

- The gross value of his good would, then, be Rs 100 + 30, or Rs 130.

- At a tax rate of 10%, the tax on output (the gear) will then be Rs 13.

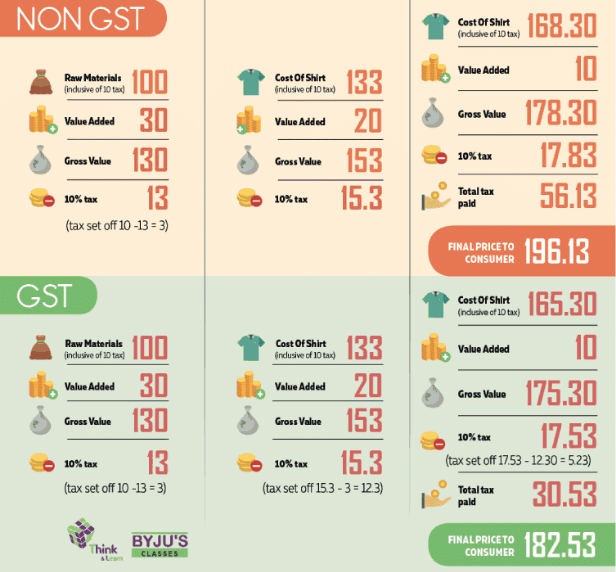

- But under GST, he can set off this tax (Rs 13) against the tax he has already paid on raw material/inputs (Rs 10). This setoff is also called as input credit. This forms the crux of GST.

- Therefore, the effective GST incidence on the manufacturer is only Rs 3 (13 – 10).

What is Input Credit (set off)?

- “Input Tax Credit” is an aggregate total amount of tax paid by a registered dealer on the total purchases made by him within the State from other dealers.

-Salient features of Input tax credit:

- It can be adjusted against the tax payable by the purchasing dealer on his sales.

- It is available for the purchase of goods made within the state by a registered dealer from another registered dealer.

- It is allowed for both manufacturers and traders

- Even for stock transfer/consignment transfer/branch transfer of goods out of the State, input tax paid in excess of 2% will be eligible for a tax credit

- In the case of common goods used for taxable goods and tax-free goods, ITC is allowed proportionately to the extent the purchases are used for the purpose of taxable goods.

- Thus, credit relating to the goods used in the manufacture of exempted goods has to be reversed.

-Stage 2:- The next stage is that of the good passing from the manufacturer to the wholesaler.

- The wholesaler purchases it for Rs 130, and adds on value (which is basically his ‘margin’) of, say, Rs 20.

- The gross value of the good he sells would then be Rs 130 + 20 — or a total of Rs 150.

- A 10% tax on this amount will be Rs 15.

- Under GST, he can set off the tax on his output (Rs 15) against the tax on his purchased good from the manufacturer (Rs 13).

- Thus, the effective GST incidence on the wholesaler is only Rs 2 (15 – 13).

-Stage 3:-

- In the final stage, a retailer buys the gear from the wholesaler.

- To his purchase price of Rs 150, he adds value, or margin, of, say, Rs 10.

- The gross value of what he sells, therefore, goes up to Rs 150 + 10, or Rs 160.

- The tax on this, at 10%, will be Rs 16.

- But by setting off this tax (Rs 16) against the tax on his purchase from the wholesaler (Rs 15), the retailer brings down the effective GST incidence on himself to Re 1 (16 –15).

- Thus, the total GST on the entire value chain from the raw material/input suppliers (who cannot claim any tax credit since they haven’t purchased anything themselves) through the manufacturer, wholesaler and retailer are Rs 10 + 3 +2 + 1, or Rs 16.

- Credits of input taxes paid at each stage will be available in the subsequent stage of value addition, which makes GST essentially a tax only on value addition at each stage.

- The final consumer will thus bear only the GST charged by the last dealer in the supply chain, with set-off benefits at all the previous stages.

Brief chronology of the evolution of taxation regime in India:

- GST was first recommended by the Kelkar committee task force.

- A brief chronology outlining the major milestones on the proposal for introduction of GST in India is as follows:

YEAR 1986:

- Jha Committee first introduced value-added taxation in India.

- This was called as MODVAT (modified VAT).

- The foremost objective of MODVAT was:

(i) Removal of cascading burden,

(ii) Rationalization and,

(iii) Avoiding double taxation. - It was renamed as CENVAT later. However, CENVAT was VAT levied on central excise duties only.

- State-level VAT/sales tax and interstate tax were not altered.

Salient Features of VAT and CENVAT

- VAT reduces tax erosion because a seller pays VAT on his sales but gets a refund of VAT paid by him on previous purchase (Input Credit).

- A retailer pays VAT but is refunded (through the mechanism of (input credit) VAT paid by him on goods purchased by him from the wholesale dealer.

- He cannot claim a refund unless he shows a receipt.

- CENVAT applies only to the manufacturing stage and does extend down to the distribution stage until the retail sale of goods.

- CENVAT mechanism extends for set-off credit only amongst central excise duty and services tax into a level of production.

- CENVAT does not extend to value addition by the distribution trade below stages of manufacturing.

- Manufacturers cannot claim set-off against other central taxes and duties like additional excise duties surcharges.

- Based on the recommendations of Asim Das Gupta committee, State level VAT was introduced.

- This replaced sales tax, turnover tax, and surcharge on sales tax at state level.

EVOLUTION OF GST

- In 2003, the Kelkar Task Force on indirect tax had suggested a comprehensive Goods and Services Tax (GST) subsuming central, state taxes, and interstate taxation based on VAT principle.

- A proposal to introduce a National level Goods and Services Tax (GST) by April 1, 2010 was first mooted in the Budget Speech for the financial year 2006-07.

- Since GST involves reform/ restructuring of not only indirect taxes levied by the Centre but also the States, an Empowered Committee of State Finance Ministers (EC) was constituted for designing a road map for the same.

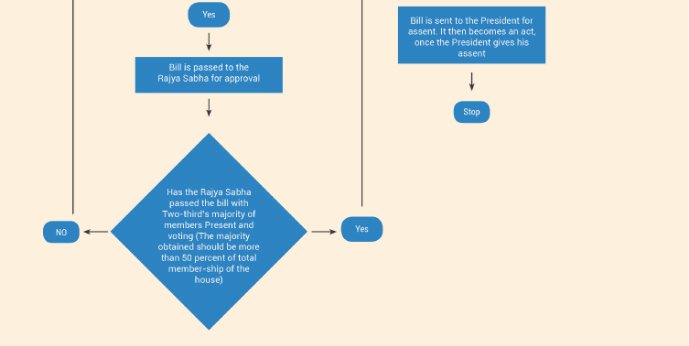

- The first attempt to pass GST was made in 2011 by introducing the Constitution (115th Amendment) Bill in the Lok Sabha, which lapsed due to dissolution of 15th Lok Sabha.

- The Bill was again introduced as 122nd constitution amendment bill and now stands passed by both Lok Sabha and Rajya Sabha.

- Today it stands passed by both the Houses of Parliament, pending approval from more than 50 per cent of the states.

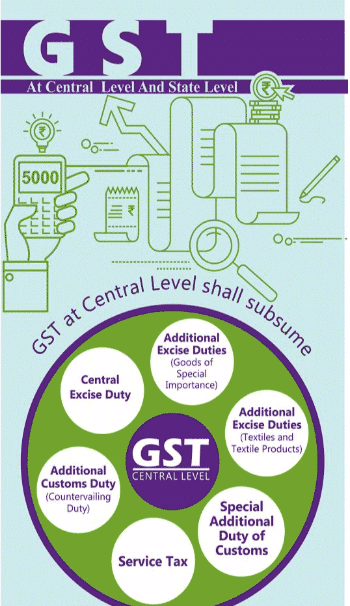

Current Indirect Taxation Structure that GST will Subsume:

Table representing taxation under different regimes

SHORTCOMINGS IN THE PRESENT TAX STRUCTURE AND NEED FOR GST Tax Cascading:

- The most significant contributing factor to tax cascading is the partial coverage by Central and State taxes.

- The exempt sectors are not allowed to claim any credit for the Cenvat or the Service Tax paid on their inputs.

Levy of Excise Duty on manufacturing point:

- The CENVAT is levied on goods manufactured or produced in India. Limiting the tax to the point of manufacturing is a severe impediment to an efficient and neutral application of tax. Taxable event at manufacturing point itself forms a narrow base.

- For example, valuation as per excise valuation rules of a product, whose consumer price is Rs. 100/-, is, say, Rs. 70/-. In such a case, excise duty as per the present provisions is payable only on Rs.70/-, and not on Rs.100/-.

Complexity in determining the nature of transaction:

- Goods and services are currently taxed separately.

- Inability of States to levy tax on services With no powers to levy tax on incomes or the fastest growing components of consumer expenditures, the States have to rely almost exclusively on compliance improvements or rate increases for any buoyancy in their own-source revenues

- VAT applies at manufacturing stage (CENVAT) as well as Sales stage (State level VAT). Therefore, there is a duality of taxation

- Input credit set-off is not available against different taxes. For eg: set off not available for CENVAT against state VAT

- Different tax rates are levied across different states. Hence, it can sometimes increase the cost of production and lead to uncompetitive prices.

- The intrastate transaction gets input credit set off but not inters state transaction. Therefore, a retailer or whole sole merchant is subject to the duality of taxes

- Likewise, as CENVAT, State VAT covers only sales. Sellers can claim credit only against VAT paid on previous purchase.

- Centre cannot impose taxes on goods beyond manufacturing (excise) or primary import (customs) stage. Centre only can tax services. State has no powers to tax services. State has exclusive domain of taxes on consumption.

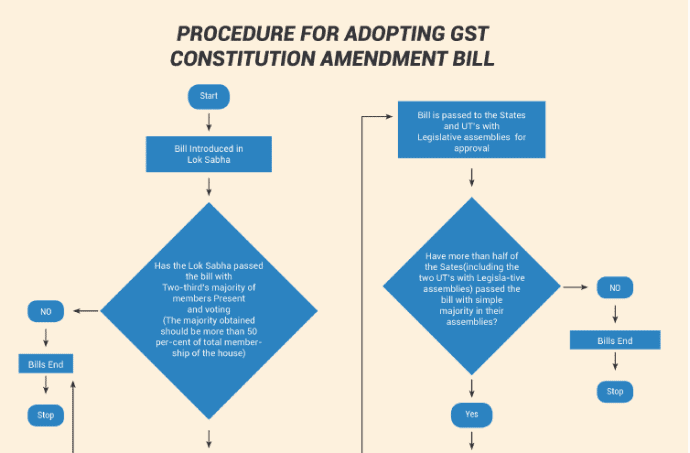

Procedure for adopting GST Constitution Amendment bill

- After Passing of GST bill, the States and the union Government have to adopt model GST Laws

- Expected roll out of GST is 1st April 2017

- Salient features of the GST Bill:

- No differentiation between good and services tax. One rate for both goods and services

- Simultaneous power upon Parliament and the State Legislatures to make laws governing goods and services tax;

- Tax will be levied on every supply of goods and services.

- Subsumes most of the Indirect taxes at state and central level (barring few exceptions listed below)

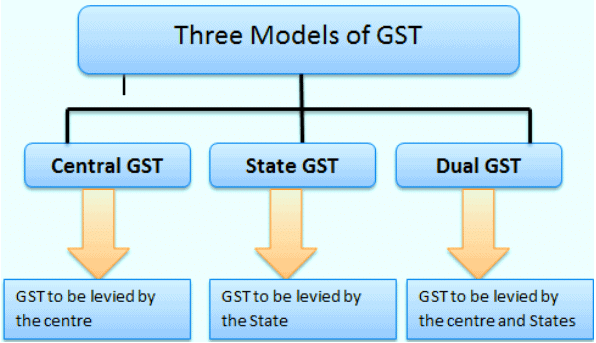

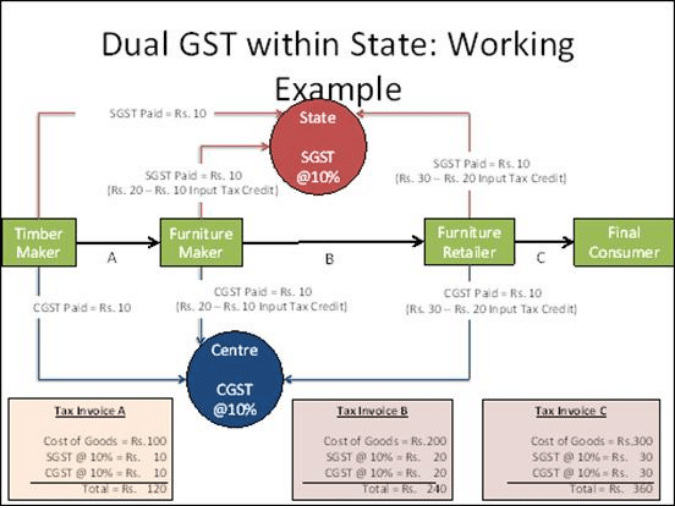

- Keeping in mind the federal structure of India, there will be two major components of GST – Central GST (CGST) and State GST (SGST). Both Centre and States will simultaneously levy GST across the value chain.

- Centre would levy and collect Central Goods and Services Tax (CGST), and States would levy and collect the State Goods and Services Tax (SGST) on all transactions within a State.

- The Central GST and the State GST would be levied simultaneously on every transaction of supply of goods and services except on exempted goods and services, goods which are outside the purview of GST and the transactions which are below the prescribed threshold limits. Further, both would be levied on the same price or value unlike State VAT which is levied on the value of the goods inclusive of Central Excise.

- Cross utilization of credit of CGST between goods and services would be allowed. Similarly, the facility of cross utilization of credit will be available in case of SGST.

- However, the cross utilization of CGST and SGST would not be allowed except in the case of inter-State supply of goods and services under the IGST model which is explained below

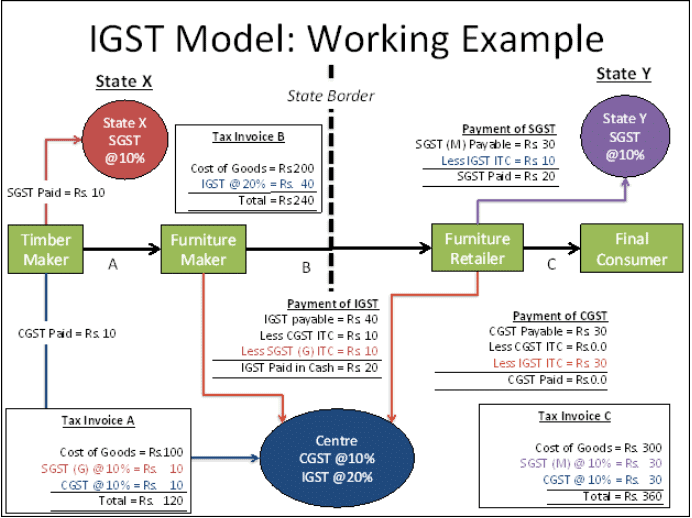

- In case of inter-State transactions, the Centre would levy and collect the Integrated Goods and Services Tax (IGST) on all inter-State supplies of goods and services under Article 269A (1) of the Constitution.

- The IGST would roughly be equal to CGST plus SGST. The IGST mechanism has been designed to ensure seamless flow of input tax credit from one State to another.

- The inter-State seller would pay IGST on the sale of his goods to the Central Government after adjusting credit of IGST, CGST and SGST on his purchases (in that order).

- The exporting State will transfer to the Centre the credit of SGST used in payment of IGST.

- The dealer who imports would claim credit of IGST while discharging his output tax liability (both CGST and SGST) in his own State.

- The Centre will transfer to the importing State the credit of IGST used in payment of SGST. Since GST is a destination-based tax, all SGST on the final product will ordinarily accrue to the consuming State.

- Producing versus consuming states.

(i) Major manufacturing states like Gujarat and Maharashtra will lose a substantial amount of tax revenue, earlier accruing from interstate taxes (like Central sales tax), due to implementation of a destination based GST.

(ii) Such states will be completely compensated (100% of the losses) for the loss of revenue up to 5 years.

(iii) 1% additional tax for Integrated Goods and service tax (IGST) tax for 2 years was proposed However this provision was deleted in the amended bill passed in Rajya Sabha.

(iv) Similarly, the demand for constitutional cap on the rate of GST has also been done away with.

(v) The input tax credit of CGST would be available for discharging the CGST liability on the output at each stage.

(vi) Similarly, the credit of SGST paid on inputs would be allowed for paying the SGST on output.

(vii) No cross utilization of credit would be permitted.

(viii) Centre & State to have concurrent powers to make laws on goods and services. Only centre can levy IGST (Intersect Supply of Goods and Services) and imports.

(ix) Law made by parliament in relation to GST will not override state laws on GST.

(x) Input tax credit set off will be accessible across Intra and Inter-state transactions as GST will be one single tax at central and state level.

(xi) The Central GST and the State GST would be levied simultaneously on every transaction of supply of goods and services except on exempted goods and services, goods which are outside the purview of GST and the transactions which are below the prescribed threshold limits.

(xii) Further, both would be levied on the same price or value unlike State VAT which is levied on the value of the goods inclusive of Central Excise

(xiii) Alcohol for human consumption has been exempted from purview of GST.

Taxing the imports under GST:

- The Additional Duty of Excise or CVD and the Special Additional Duty or SAD presently being levied on imports will be subsumed under GST.

- IGST will be levied on all imports into the territory of India.

- Unlike in the present regime, the States where imported goods are consumed will now gain their share from this IGST paid on imported goods.

- Major features of the proposed registration procedures under GST:

- Existing dealers: Existing VAT/Central excise/Service Tax payers will not have to apply afresh for registration under GST.

- New dealers: Single application to be filed online for registration under GST.

- The registration number will be PAN based and will serve the purpose for Centre and State.

- Unified application to both tax authorities.

- Each dealer to be given unique ID GSTIN.

- Deemed approval within three days.

- Post registration verification in risk based cases only.

Major features of the proposed returns filing procedures under GST:

- Common return would serve the purpose of both Centre and State Government.

- There are eight forms provided for in the GST business processes for filing for returns. Most of the average tax payers would be using only four forms for filing their returns.

- These are:

(i) Return for supplies

(ii) Return for purchases

(iii) Monthly returns and

(iv) Annual return - Small taxpayers: Small taxpayers who have opted composition scheme shall have to file return on quarterly basis.

- Filing of returns shall be completely online. All taxes can also be paid online.

Major features of the proposed payment procedures under GST:

- Electronic payment process- no generation of paper at any stage

- Single point interface for challan generation- GSTN

- Ease of payment – payment can be made through online banking, Credit Card/Debit Card, NEFT/RTGS and through cheque/cash at the bank

- Common challan form with auto-population features

- Use of single challan and single payment instrument

- Common set of authorized banks

- Common Accounting Codes

THE GST COUNCIL:

- The Federalism debate:

- The most discussed consequence of the passage of GST bill is the fiscal federalism.

- The

proponents of the GST bill are positive about the centre-state relations in this context of passage of the GST bill.

- It actually accelerates the reconfiguration of centre-state fiscal relations already underway.

- The experts argue that, States would become key stakeholders in the national economy, which was quite rare in the present scheme of things.

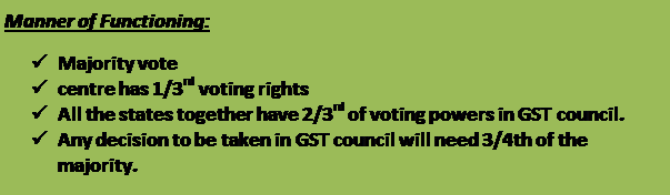

- An important feature of the new tax framework is the creation of the GST Council. The way it has been designed, the Union government has only one-third say in decisions taken by the GST Council, while the rest is accounted for by the states; and all decisions have to be carried by a three-fourth majority.

- Hence, this clearly indicates that centre and states need to co-operate with each other to ensure a smooth functioning of the tax administration. This, clearly is a double whammy for the states, which have their fiscal autonomy enhanced due to the increase in untied funds from net indivisible pool of taxes ( from 32 percent to 42 percent), as a result of the 14th Finance Commission.

- However, the opponents of the GST argue that, the voting pattern in GST council is not completely based on economics. The purpose of the GST Bill is to concentrate on manufacturing and achieve excellence so that the same product is not manufactured locally with sub-optimal efficiency in every state for tax reasons.

- That being the case, it is natural there are going to be only a few manufacturing states while the rest will be consuming states.

- To have a council where the manufacturing state has one vote whereas all other states, likely consumers, also have a vote each is unfair.

- Of course consumers will vote in their own interests.

- “Make in India” Programme is focused for strengthening and protecting the domestic industry from foreign import. Likewise, state governments have to protect local industry and employment. For this objective lesser sales tax and other incentives is needed for helping local producers. But the right of state governments for variable taxation will end with the introduction of GST regime.

- Further, economists argue that taxation powers are not only a measure of resource mobilisation. It could be used as a tool to control and restrict the consumption of some goods for social good.

- (For example, Tobacco products generally attracts huge tax rate as a measure to control the consumption on health grounds. Here tobacco producing States argue for lesser taxes for maximum sales and the Consumer States will demand for a leverage for fixing higher taxes.)

- Health concerns ratify the higher rate of tax on tobacco. Now, this can be a tricky situation for the centre as to whose interests it should protect.

- Likewise, if a state government needs an additional resource mobilisation for facing a natural calamity, it cannot decide for any special levy.

- Swachh bharat and other Central schemes can only be decided and used by the Central Government.

- The GST will take away the rights of states to decide taxes according to their socio-economic situations. The situation in Kerala is quite different than the situation in Tamil Nadu or Assam or Bihar or West Bengal. Each state has its own socio-economic-political reasons to decide the type of tax to be levied.

- Therefore, the experts argue that the veto power given to centre in the GST council is undemocratic. They opine for a more flexible weights based voting pattern and reduction in the weightage of the centre’s vote.

- Hence, there has to be more consensus on the structure, pattern and working of the GST council.

- The term ‘Cooperative Federalism’, sums up the ideology that would successfully define this evolution: Together they stand and divided they will fail.

- In this, the recommendations of FFC, GST and other policies on the anvil are only stepping stones. Evolving institutions such as the GST Council and the revived Inter-State Council will be critical in overseeing this transition with minimal hindrances; state chief ministers are already equal partners in the governing council of NITI (National Institution for Transforming India) Aayog, which has replaced the Planning Commission.

Advantages of GST For business and industry

- Easy compliance:

- A robust and comprehensive IT system would be the backbone of the GST regime in India. Therefore, all tax payer services such as registrations, returns, payments, etc. would be available to the taxpayers online, which would make compliance easy and transparent.

- Uniformity of tax rates and structures:

- Indirect tax rates and structures would be uniform across the country, thereby increasing certainty and ease of doing business. In other words, GST would make doing business in the country tax neutral, irrespective of the choice of place of doing business.

- Removal of cascading:

- A system of seamless tax-credits throughout the value-chain, and across boundaries of States, would ensure that there is minimal cascading of taxes. This would reduce hidden costs of doing business.

- Improved competitiveness:

- Reduction in transaction costs of doing business would eventually lead to an improved competitiveness for the trade and industry.

- Gain to manufacturers and exporters:

- The subsuming of major Central and State taxes in GST, complete and comprehensive set-off of input goods and services and phasing out of Central Sales Tax (CST) would reduce the cost of locally manufactured goods and services.

- This will increase the competitiveness of Indian goods and services in the international market and give boost to Indian exports. The uniformity in tax rates and procedures across the country will also go a long way in reducing the compliance cost.

- Further, due abolition of multiple taxation, the warehousing practices adopted by large industrial houses are expected to come down. This would boost ancillary units, especially in manufacturing, as the large industrial houses will freely contract out the fabrication to vendors due to reduction in operational cost as a result of GST.

- This will provide the adequate thrust and driving force for the success of Make in India and Skill India.

For Central and State Governments

- Simple and easy to administer:

- Multiple indirect taxes at the Central and State levels are being replaced by GST. Backed with a robust end-to-end IT system, GST would be simpler and easier to administer than all other indirect taxes of the Centre and State levied so far.

- Better controls on leakage:

- GST will result in better tax compliance due to a robust IT infrastructure. Due to the seamless transfer of input tax credit from one stage to another in the chain of value addition, there is an in-built mechanism in the design of GST that would incentivize tax compliance by traders.

- Higher revenue efficiency:

- GST is expected to decrease the cost of collection of tax revenues of the Government, and will therefore, lead to higher revenue efficiency.

For the consumer

- Single and transparent tax proportionate to the value of goods and services:

- Due to multiple indirect taxes being levied by the Centre and State, with incomplete or no input tax credits available at progressive stages of value addition, the cost of most goods and services in the country today are laden with many hidden taxes. Under GST, there would be only one tax from the manufacturer to the consumer, leading to transparency of taxes paid to the final consumer.

Relief in overall tax burden:

- Because of efficiency gains and prevention of leakages, the overall tax burden on most commodities will come down, which will benefit consumers.

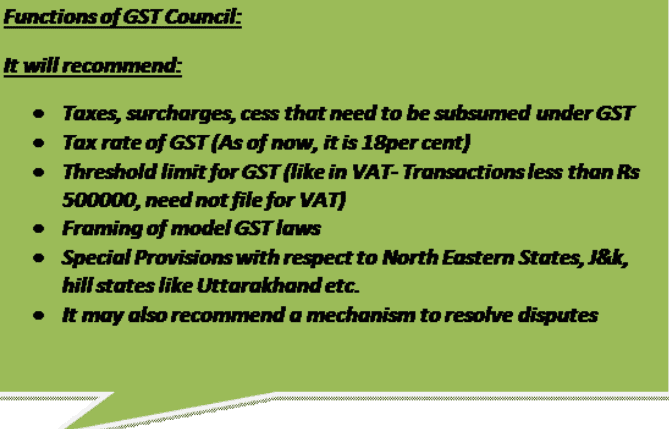

GST rate:

- Although a GST council is expected to work towards fixing a GST rate, it will be quite challenging to reach a consensus on the uniform rate of taxation. The challenge is further compounded by the lack of precedent on this front earlier.

- Producing and consuming states might have different viewpoints regarding rate of taxation.

(For example producing states like Gujarat and Maharashtra might want low taxation on manufacturing of cotton textiles related goods, and consumption states like Haryana, Uttar Pradesh might want high rate of taxation on retail sales of these goods leading to conflict).

Compensation to States:

- The revenue foregone by the states as a result of transition to GST will be compensated by the Union government. However, there is no fixed formula or method on reaching an exact figure.

- The negotiations may have political overtones and could be a challenging task for the union government.

- Accounting Systems:

- The cadre of Chartered accountants, Tax consultants, Tax bureaucracy and the like need to be trained on a new accounting system. This will require a lot of technological and institutional capacity building

- The retailers, whole sale merchants, small general store owners and the various stakeholders also need to transit towards a new system of accounting. This system may pose significant challenges specifically to small traders as they generally are not used to a robust account keeping system.

- Other challenges:

- Cess ( education, Krishi Kalyan, Swatch Bharat) and surcharges charged by centre are currently not part of GST. States might have an issue over this.

- Further, GST will not apply to Petroleum crude, High speed diesel, Motor spirit (petrol), Natural gas, Aviation turbine fuel. These have a very high inter-connectivity with both manufacturing and service costs which might hinder seamless application of GST across sectors.

- Approach to the Civil Services Examination: In mains focus will be on effect of GST on Indian economy, federal structure (centre-state relations) and analysis of the new Indirect taxation structure.

- GS Paper II:

- Indian Constitutional amendments

- Functions and responsibilities of the Union and the States, issues and challenges pertaining to the federal structure, devolution of powers and finances up to local levels and challenges therein.

- Parliament and State Legislatures – structure, functioning, conduct of business, powers & privileges and issues arising out of these.

- GS Paper III:

- Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment.

- Government Budgeting.

MoU approved by the Cabinet

Context:- The Union Cabinet approved the following MoUs between India and various countries.

India and Nepal:-

- Memorandum of Understanding (MoU) signed between the Indian Council of Medical Research (ICMR), India and the Nepal Health Research Council (NHRC), Nepal.

- The objectives of this MoU are collaboration on joint research activities of mutual interest such as cross-border health issues, Ayurveda/traditional medicine and medicinal plants, climate change and health, non-communicable diseases, mental health, population-based cancer registry, tropical diseases (vector-borne diseases such as dengue, chikungunya, malaria, JE, etc.), influenza, clinical trial registry, health research ethics, capacity building through exchange of knowledge, skills tools and fellows and collaboration for adoption of tools, guidelines, protocols and best practices related to health research.

India and Myanmar

- Memorandum of Understanding signed between the Indian Council of Medical Research (ICMR), India and the Department of Medical Research (DMR), Ministry of Health and Sports of Myanmar.

- Objectives of the MoU:

(i) Elimination of infectious diseases

(ii) Development of network platform of emerging and viral infections

(iii) Training/capacity building in research methodology management, clinical trials, ethics, etc.

(iv) Harmonization of regulatory mechanism

India and The Gambia

- MoU signed between the Department of Administrative Reforms and Public Grievances, Ministry of Personnel, Public Grievances and Pensions, GOI and the Public Service Commission, Office of the President, Republic of The Gambia.

- The MoU is on Refurbishing Personnel Administration and Governance Reforms.

- The areas of cooperation includes improving performance management system in the government, implementation of contributory pension scheme, e-recruitment in government, among others.

Atmanirbhar Bharat Rojgar Yojana (ABRY)

Context:- Cabinet approved the extension of last date of Registration under Aatmanirbhar Bharat Rojgar Yojana (ABRY) from 30th June 2021 to 31st March 2022.

Details:-

- ABRY was announced as one of the measures under Aatmanirbhar Bharat 3.0 package to boost the economy and increase employment generation in the formal sector during the post-Covid recovery phase.

- Under ABRY, the Government of India is crediting for a period of two years both the employees’ and employers’ share (24% of wages) or only the employees’ share (12% of wages), depending on the strength of EPFO registered establishments.

Context:- The Union Cabinet has given its approval for Atmanirbhar Bharat Rojgar Yojana (ABRY) to boost employment in formal sector and incentivize creation of new employment opportunities during the Covid recovery phase under Atmanirbhar Bharat Package 3.0.

About the Atmanirbhar Bharat Rojgar Yojana (ABRY):

- Government of India will provide subsidy for two years in respect of new employees engaged on or after 1st October, 2020 and up to 30th June, 2021.

- Government of India will pay both 12% employees’ contribution and 12% employers’ contribution i.e. 24% of wages towards EPF in respect of new employees in establishments employing upto 1000 employees for two years

- Government of India will pay only employees’ share of EPF contribution i.e. 12% of wages in respect of new employees in establishments employing more than 1000 employee for two years.

- An employee drawing monthly wage of less than Rs. 15000/- who was not working in any establishment registered with the Employees’ Provident Fund Organisation (EPFO) before 1st October, 2020 and did not have a Universal Account Number or EPF Member account number prior to 1st October 2020 will be eligible for the benefit.

- Any EPF member possessing Universal Account Number (UAN) drawing monthly wage of less than Rs 15000 who made exit from employment during Covid pandemic from March 1, 2020, to September 30, 2020, and did not join employment in any EPF covered establishment up to September 30 will also be eligible to avail benefit.

Bharat Net Project

Context:- Revised implementation strategy of Bharat Net Project.

Details:-

- The Cabinet accorded approval for the revised implementation strategy of Bharat Net through Public Private Partnership mode in 16 States of the country.

- The program will be extended to all inhabited villages beyond Gram Panchayats (GPs).

- The revised strategy also includes the creation, upgradation, operation, maintenance and utilization of Bharat Net by the concessionaire who will be selected by a competitive international bidding process.

- For the other states/UTs of the country, the Cabinet has given in-principle approval for covering all inhabited villages. The modalities for the same will be worked out separately by the Dept of Telecommunications.

Benefits:

- Proliferation of broadband in rural areas will bridge the rural-urban divide of digital access and accelerate the achievement of Digital India.

- The penetration and proliferation of broadband is also expected to increase direct and indirect employment and income generation.

- The States where the PPP Model is envisaged will facilitate free Right of Way.

- The Private Sector Partner is also expected to bring an equity investment and raise resources towards capital expenditure and for operation and maintenance of the network.

Advantages offered by the Bharat Net PPP Model:

- Use of innovative technology by the Private Sector Provider for the consumers

- High quality of service and service level to consumers

- Faster deployment of network and quick connectivity to consumers

- Competitive tariffs for services

- Variety of services on high-speed broadband including Over the top (OTT) services and multi-media services as part of packages offered to consumers

- Access to all online services

Loan Guarantee Scheme for Covid Affected Sectors (LGSCAS)

Context:- Cabinet approved Loan Guarantee Scheme for Covid Affected Sectors (LGSCAS).

About Loan Guarantee Scheme for Covid Affected Sectors (LGSCAS):

- This scheme enables funding to the tune of Rs. 50,000 crore to provide financial guarantee cover for brownfield expansion and greenfield projects related to health/medical infrastructure.

- The Scheme would be applicable to all eligible loans sanctioned up to 31.03.2022, or till an amount of Rs. 50,000 crore is sanctioned, whichever is earlier.

- The move comes in the wake of disruptions caused by the second wave of the pandemic which overwhelmed India’s healthcare system.

- According to the government statement, the scheme is a specific response to the extraordinary situation faced by the country due to inadequate health infrastructure during the pandemic’s second wave. - The approved scheme is expected to help the country in shoring up its much-needed healthcare infrastructure along with creating more employment opportunities.

- The main objective of LGSCAS is to partially mitigate credit risk (primarily construction risk) and facilitate bank credit at lower rates of interest.

- It aims at upscaling medical infrastructure in India, especially targeting the underserved areas.

What the scheme offers:

- LGSCAS would provide a guarantee of 50 percent for brownfield projects and 75 per cent to greenfield projects for loans sanctioned up to Rs.100 crore, set up at urban or rural locations other than 8 Metropolitan Tier 1 cities (Class X cities).

- For aspirational districts, the guarantee cover for both brownfield expansion and greenfield projects shall be 75%.

Additional Information:

The Cabinet also approved the enhancement of the corpus of the Emergency Credit Line Guarantee Scheme (ECLGS).

Emergency Credit Line Guarantee Scheme (ECLGS)

The Union Cabinet, led by Prime Minister Narendra Modi, approved the Emergency Credit Line Guarantee Scheme (ECLGS). The scheme was launched as a part of the Atma Nirbhar Bharat package for the Micro, Small, and Medium Enterprises (MSME) borrowers to mitigate the distress caused by the COVID-19 pandemic.

- Why is ECLGS in the news?

For UPSC Prelims 2021, candidates should know that the scope of ECLGS has been expanded by the Finance Ministry. The scheme was initially announced in May 2020 and then over a period of time, the Finance Ministry has expanded the scope of the ECLGS. Recently (May 2021), ECLGS 4.0 has been introduced which provides 100 percent guarantee cover to loans up to Rs.2 crore to hospitals/nursing homes/clinics/medical colleges for setting up on-site oxygen generation plants, interest rate capped at 7.5%.

- Emergency Credit Line Guarantee Scheme:-

In this article, we shall discuss the Emergency Credit Line Guarantee Scheme along with its expansion. Also, discussed are the objectives and significance of the scheme, and the important organizations involved in its functioning.

This topic is also important for candidates preparing for the upcoming IAS Exam, especially for the GS-II and III papers under the Government policies, growth, and development part.

Emergency Credit Line Guarantee Scheme – Key Points

- The Union Cabinet approved the Emergency Credit Line Guarantee Scheme in May 2020 and allowed additional funding of up to Rs.3 lakh crores to different sectors, especially Micro, Small, and Medium Enterprises (MSME) and MUDRA borrowers.

- The scheme is a part of the AtmaNirbhar Bharat Abhiyan which was launched by Prime Minister Narendra Modi to make India a self-dependent country.

- Under the ECLGS, all loans sanctioned under the Guaranteed Emergency Credit Line (GECL) facility will be provided with additional credit. However, there are two specifications:

(i) The scheme would be applicable for loans sanctioned from the date of announcement of the scheme to October 31, 2020, [Now September 3, 2021] OR

(ii) Guarantees for an amount of Rs.3 lakh crore are issued (whichever happens first)

(iii) Disbursement is permitted up to December 31, 2021. - UPSC aspirants can also get the List of Government Schemes in India at the linked article and learn more about the various schemes launched in the interest of the citizens of the country.

Objectives of Emergency Credit Line Guarantee Scheme (ECLGS)

While the country was fighting the COVID-19 pandemic, major losses were faced by the MSMEs in the manufacturing and other sectors. To overcome this loss, the Government introduced the Emergency Credit Line Guarantee Scheme.

Discussed below are the major objectives of ECLGS:

- As per this scheme, 100% guarantee coverage is to be provided by National Credit Guarantee Trustee Company Limited (NCGTC) to the Member Lending Institutions (MLI), Banks, Financial Institutions, and Non-Banking Financial Companies (NBFC)

- It would increase access to, and enable the availability of additional funding facilities to MSME and MUDRA borrowers

- The Scheme aims at mitigating the economic distress faced by MSMEs by providing them additional funding in the form of a fully guaranteed emergency credit line

- It shall also provide credit to the sector at a low cost, thereby enabling the small sector businesses to meet their operational liabilities and restart their manufacturing and work

Once the proper functioning of the MSMEs in India starts off normally, it will benefit India economically and socially. This is one of the major reasons why the Government introduced this scheme during the unprecedented situation of a pandemic.

Who is eligible under the ECLG Scheme?

As per the latest eligibility criteria with the launch of the expanded Emergency Credit Line Guarantee Scheme, the following criteria had to be met to be applicable for a loan under the scheme:

- Enterprises with a turnover of up to Rs. 250 crores (FY 2019-20) with outstanding loans up to Rs. 50 crores, as of February 29, 2020

- GECL credit provided will be up to 20% of the borrower’s total outstanding credit as of February 29, 2020.

- The maximum amount of loan that can be availed under the scheme is Rs. 5 crore

Tenure & Interest Rates under ECLGS

- The loan tenure is for 4 years and the moratorium period of 1 year on the principal amount is also applicable [Now the loan tenure is 5 years]

- Interest rates under ECLGS have also been capped:

(i) 9.25% for Banks and Financial Institutions

(ii) 14% for Non-Banking Financial Companies - The National Credit Guarantee Trustee Company Ltd (NCGTC) is not allowed to charge any Guarantee Fee from the Member Lending Institutions that are included under this scheme

ECLGS 4.0 – Expansion of the Scheme

On 31st May 2021, the Indian government notified the expansion of the ECLGS. Under the version of ECLGS 4.0:

- 100 percent guarantee cover is being provided to hospitals/nursing homes/clinics/medical colleges for loans of up to Rs 2 crores at an interest rate of 7.5 percent. It is given for setting up on-site oxygen generation plants.

- The eligible borrowers who earlier had a loan tenure of four years can now avail of a loan tenure of five years.

- Additional ECLGS assistance of up to 10% of the outstanding as of February 29, 2020, to borrowers covered under ECLGS 1.0

- The Rs. 500 crore loan ceiling under ECLGS 3.0 is being discontinued.

- The maximum additional ECLGS assistance to each borrower is being limited to 40% or Rs.200 crore, whichever is lower.

- Civil aviation sector is an eligible borrower under ECLGS 3.0.

- About ECLGS 2.0

The scheme was announced in November 2020 as a part of the Atma Nirbhar Bharat 3.0 package. This is the revised scheme where the credit limits have been increased and the sectors involved have also been expanded.

Some key points that need to be noted with respect to ECLGS 2.0 have been discussed below:

- The Emergency Credit Line Guarantee Scheme has been expanded to 27 new sectors, including the health sector

- These 27 sectors have been identified by the Kamath Committee for one time debt restructuring. Power, construction, textiles, real estate, tourism are few among the many sectors identified

- Individual beneficiaries for both, professional and self-employed people have also been included in the scheme

- The credit limit has been revised to Rs.250 crores with outstanding loans up to Rs. 50 crore, as of February 29, 2020

- There also has been an expansion in the limit of loan which can be sanctioned. The maximum amount which can be availed under ECLGS 2.0 is Rs. 10 crore

- The tenor has been upgraded to 5 years with a 1-year moratorium on repayment of principal

About National Credit Guarantee Trustee Company Limited

- NCGTC or the National Credit Guarantee Trustee Company Limited was registered under the Companies Act, 1956 in 2014

- It is a wholly-owned company of the Government of India

- It was established by the Department of Financial Services, Ministry of Finance

- The main role of the Organisation is to design credit guarantee programs, to share the risk of lending among the lenders, and facilitate financial access to a prospective borrower

Conclusively, to revise the economy of the country which faced major disturbances due to the COVID lockdown, the Government of India decided to take charge of making the country self-dependent. And, the Emergency Credit Line Guarantee Scheme is one of those initiatives.

AIM-iLEAP Program

Context:

AIM-iLEAP, the first fintech cohort of the Atal Innovation Mission (AIM) concluded.

About AIM iLEAP:

- This is a program under the Atal Innovation Mission to provide AIM-backed start-ups with the much needed access to industry, markets and investors.

- The fintech cohort was done through a series of thematic virtual demo days organised by AIM in partnership with Startup Réseau and Visa as part of AIM-iLEAP (Innovative leadership for entrepreneurial agility and profitability) initiative.

- The objective of the AIM-iLEAP program is to invite technology start-ups across a broad range of functions and have them present their solutions to the corporate leadership and innovation team for enabling market access and industry partnerships.

- The Fintech cohort consisted of start-ups from a wide range of areas such as payments, international money transfers, personal finance, consumer banking, insurance, neo bank, etc.

- In the bootcamp they got an opportunity to fine-tune their pitches, work on their GTM strategy, understand more about the fintech ecosystem, ask questions to sectoral experts and so on.

- The program was attended by fintech giants such as Visa, Paytm, etc.

- As per the AIM’s mission, AIM-iLEAP bootcamp and demo day is the first among the many initiatives to push startups in the country.

- Future cohorts shall be focussed on different sectors such as Agri-tech, Defence Tech, Smart Mobility, AI and so on.

Black Carbon (BC)

Context:

Study says black carbon could lead to premature mortality.About the Study:

- Scientists from Department of Science & Technology-Mahamana Centre of Excellence in Climate Change Research (MCECCR) at Banaras Hindu University.

- The study was supported by the Climate Change programme of the Department of Science and Technology (DST).

- They utilized daily all-cause mortality and ambient air quality from 2009 to 2016 to clearly establish a significant impact of Black Carbon aerosols, NO2 and, PM2.5 exposure on mortality.

Results:

- Black Carbon has a significant adverse effect on human health and leads to premature mortality.

- The inclusion of co-pollutants (NO2 and PM 2.5) in the multi-pollutant model increased the individual mortality risks for BC aerosols.

- The effect of pollutants was more prominent for males, age group 5-44 years and, in winter.

- They found that the adverse effect of air pollutants was not limited to current day of exposure but can extend as high as up to 5 days (Lag effect).

- They further showed that mortality rises linearly with an increase in air pollutant level and shows adverse impact at higher levels.

Significance of the study:

- The Indo-Gangetic plain is exposed to black carbon with serious implications on regional climate and human health.

- Most of the pollutants-based epidemiological studies relate exposure to particulate mass concentration (PM 10 and/-or PM 2.5) that invariably generalize all particulates with equal toxicity without distinguishing individuals by its source and composition.

- Importantly, the health effects in terms of mortality due to BC aerosol exposure have never been evaluated in India.

Benefits of the study:

- The study could help in the estimation of the future burden of mortality associated with air pollutants more accurately.

- This will help government and policymakers for better planning to mitigate the adversities associated with changing climate and air pollution on health.

Revamped Distribution Sector Scheme

Context:

Cabinet approved the Revamped Distribution Sector Scheme.

About the Revamped Distribution Sector Scheme:

- It is a reforms-based and results-linked scheme to improve the operational efficiencies and financial sustainability of all DISCOMs/Power Departments excluding Private Sector DISCOMs.

- The scheme envisages the provision of conditional financial assistance to DISCOMs for strengthening supply infrastructure.

- The assistance will be based on meeting pre-qualifying criteria as well as upon the achievement of basic minimum benchmarks by the DISCOM. These will be evaluated on the basis of agreed evaluation framework tied to financial improvements.

- Each state would have its own action plan for implementation of the scheme rather than a ‘one-size-fits-all’ approach.

- The scheme proposes to subsume the ongoing schemes of IPDS, DDUGJY along with PMDP-2015 for the Union Territories of Jammu & Kashmir and Ladakh.

- The scheme would be available till 2025-26.

- Nodal agencies for the scheme’s implementation are REC Limited and Power Finance Corporation (PFC).

- The scheme has a major focus on improving electricity supply for the farmers and for providing daytime electricity to them through solarization of agricultural feeders.

- Objectives of the scheme:

(i) Reduction of AT&C losses to pan-India levels of 12-15% by 2024-25

(ii) Reduction of ACS-ARR gap to zero by 2024-25

(iii) Developing institutional capabilities for modern DISCOMs

(iv) Improvement in the quality, reliability, and affordability of power supply to consumers through a financially sustainable and operationally efficient distribution sector.

|

4.75/5 Rating |

|

Dec 22, 2024 Last updated |

|

Explore Courses for UPSC exam

|

|

practice quizzes

,Objective type Questions

,past year papers

,mock tests for examination

,shortcuts and tricks

,video lectures

,ppt

,2021 | PIB (Press Information Bureau) Summary - UPSC

,Sample Paper

,Viva Questions

,PIB Summary- 30th June

,Previous Year Questions with Solutions

,Summary

,PIB Summary- 30th June

,MCQs

,Exam

,study material

,Important questions

,2021 | PIB (Press Information Bureau) Summary - UPSC

,2021 | PIB (Press Information Bureau) Summary - UPSC

,Semester Notes

,Extra Questions

,PIB Summary- 30th June

,Free

;

PIB Summary- 30th June, 2021 Free PDF Download

Importance of PIB Summary- 30th June, 2021

PIB Summary- 30th June, 2021 Notes

PIB Summary- 30th June, 2021 UPSC Questions

Study PIB Summary- 30th June, 2021 on the App

|

© EduRev

|

Education Revolution

|

|