Recent Reforms in the Financial Sector | Management Optional Notes for UPSC PDF Download

Introduction

- The evolution of India's banking sector has been profoundly shaped by a series of pivotal reforms and legislative actions aimed at aligning the industry with global standards. These initiatives encompass a broad spectrum of measures, including liberalization, deregulation, privatization, and advancements in technology. Reforms introduced by the Narasimham Committee in the 1990s, such as strengthened capital adequacy norms and risk-based supervision, have played a central role in reshaping the banking landscape. Moreover, the adoption of Basel Norms has fortified the resilience of the banking system and enhanced risk management practices, ensuring greater stability and efficiency within the sector.

- The integration of technology-driven solutions like core banking systems, electronic fund transfers, and digital payment platforms has been pivotal in fostering financial inclusion and streamlining banking processes. Initiatives such as the Pradhan Mantri Jan Dhan Yojana and the implementation of the Insolvency and Bankruptcy Code have further contributed to broadening access to financial services and addressing non-performing assets, thereby reinforcing the solidity of the banking sector. Collectively, these reforms have nurtured a more competitive, transparent, and customer-centric banking landscape, making significant contributions to India's economic advancement and financial resilience.

Banking Legislation and Reform Measures

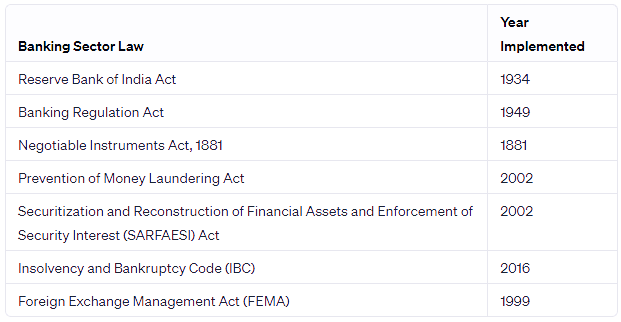

- Reserve Bank of India Act, 1934: The RBI Act establishes the Reserve Bank of India (RBI) as the central banking institution of India. It delineates the objectives and functions of the RBI, including the regulation of monetary policy, issuance and management of currency, oversight of the banking system, and administration of foreign exchange reserves. The act confers upon the RBI the authority to issue directives and guidelines to banks and financial institutions.

- Banking Regulation Act, 1949: A significant piece of legislation, the Banking Regulation Act governs and supervises the banking sector in India. It authorizes the Reserve Bank of India (RBI) to regulate banks and their operations. The act outlines the powers and functions of the RBI, procedures for bank licensing, stipulations regarding capital requirements, and regulations concerning the management and governance of banks. Additionally, it establishes the Deposit Insurance and Credit Guarantee Corporation (DICGC) to insure bank deposits.

- Negotiable Instruments Act, 1881: The Negotiable Instruments Act provides a legal framework for negotiable instruments such as promissory notes, bills of exchange, and cheques. It prescribes rules governing their transferability, rights, and liabilities of parties involved, as well as procedures for their discharge and enforcement. This act holds particular significance for the banking sector, given the widespread use of cheques as a mode of payment and settlement.

- Prevention of Money Laundering Act, 2002: Enacted to combat money laundering and the financing of terrorism, the Prevention of Money Laundering Act (PMLA) establishes the Financial Intelligence Unit (FIU) as the central agency responsible for receiving, analyzing, and disseminating information regarding suspicious transactions. The act imposes obligations on banks and financial institutions to maintain records, report transactions, and verify customer identities.

- Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002: The SARFAESI Act provides a legal framework for the securitization and reconstruction of financial assets, as well as the enforcement of security interests. It empowers banks to take possession of and sell assets of defaulting borrowers to recover outstanding dues without the need for court intervention. This act grants banks the authority to issue notices, take possession of secured assets, and enforce security interests.

- Insolvency and Bankruptcy Code (IBC), 2016: The IBC is comprehensive legislation addressing insolvency and bankruptcy proceedings for individuals, partnership firms, and corporate entities. It aims to facilitate a time-bound and efficient resolution process for stressed assets. The IBC establishes the Insolvency and Bankruptcy Board of India (IBBI) to regulate insolvency professionals and entities involved in insolvency proceedings.

- Foreign Exchange Management Act (FEMA), 1999: FEMA is a pivotal act governing foreign exchange transactions, external trade, and payments in India. Replacing the Foreign Exchange Regulation Act (FERA), FEMA empowers the RBI to regulate and control foreign exchange transactions, capital flows, and external borrowings. It also regulates foreign direct investment (FDI) and overseas direct investment (ODI) in India.

Reforming the Banking Sector in India

Reforming the banking sector in India involves a comprehensive set of measures and initiatives implemented by the government and regulatory bodies to strengthen and improve the functioning of the country's banking industry. These reforms are geared towards promoting transparency, efficiency, and stability in the sector, while also facilitating financial inclusion and ensuring sufficient credit availability for economic development. Several key components characterize the banking sector reforms in India, each contributing to the sector's progress and resilience.

- Liberalization: The reforms began in the 1990s with the liberalization of the Indian economy, which included reducing government intervention and opening up the sector to private and foreign banks. This step aimed to foster competition and diversity in the banking sector.

- Capital Adequacy: Adopting Basel norms, particularly Basel I, II, and III, aimed to strengthen banks' capital adequacy. These norms mandated that banks maintain a minimum level of capital to absorb potential losses and maintain financial stability.

- Asset Quality: Addressing non-performing assets (NPAs) or bad loans was a crucial aspect of the reforms. The introduction of the Insolvency and Bankruptcy Code (IBC) expedited the resolution of stressed assets and improved recovery mechanisms.

- Governance and Risk Management: Reforms focused on enhancing corporate governance practices in banks, emphasizing transparency, accountability, and effective risk management. The establishment of the Banking Codes and Standards Board of India (BCSBI) reinforced customer protection.

- Financial Inclusion: Initiatives such as the Pradhan Mantri Jan Dhan Yojana (PMJDY) aimed to achieve financial inclusion by providing banking services to unbanked segments of society. The promotion of technology-driven solutions, including mobile banking and digital payments, further expanded financial access.

- Regulatory Framework: The Reserve Bank of India (RBI) played a crucial role in implementing banking sector reforms, introducing various regulations and guidelines to strengthen prudential norms, risk management practices, and bank supervision.

- Merger and Consolidation: Encouraging the merger and consolidation of public sector banks was another significant aspect of the reforms. This strategy aimed to create stronger and more efficient banks, enhancing operational efficiency, reducing costs, and meeting capital requirements more effectively.

- Financial Technology (FinTech) and Innovation: The reforms also emphasized the adoption of financial technology and digital innovation. This included developing payment systems, supporting fintech startups, and establishing regulatory sandboxes to encourage experimentation and foster innovation.

List of important Banking Sector Acts and Year

The banking acts and reforms have been instrumental in shaping a resilient and dynamic banking sector in India, fostering economic growth and financial stability in the country.

Reformulation of Banking Sector Since 1991

- India has undergone significant overhauls in its banking sector, driven by a series of comprehensive reforms initiated since 1991. Recognizing the imperative to modernize the banking system, align it with global standards, and foster financial stability and inclusivity, the country embarked on a journey of transformation. Various committees were convened to propose measures and advocate reforms aimed at fortifying the efficiency and transparency of the banking sector.

- These reformative endeavors have been instrumental in reshaping India’s banking landscape, marking the onset of a new era characterized by growth and advancement. Below is a synopsis of key banking sector reforms undertaken since 1991:

Banking Sector Reforms Since 1991 in Detail

India's banking sector reforms have been pivotal in reshaping the industry and aligning it with global standards. These reforms have embraced various measures, including liberalization, deregulation, privatization, and technological advancements, with the overarching aim of bolstering efficiency, transparency, and stability while fostering financial inclusion. Over the years, numerous committees were constituted to propose measures and advocate reforms to fortify the banking sector.

Let's delve into the significant committees and their key recommendations:

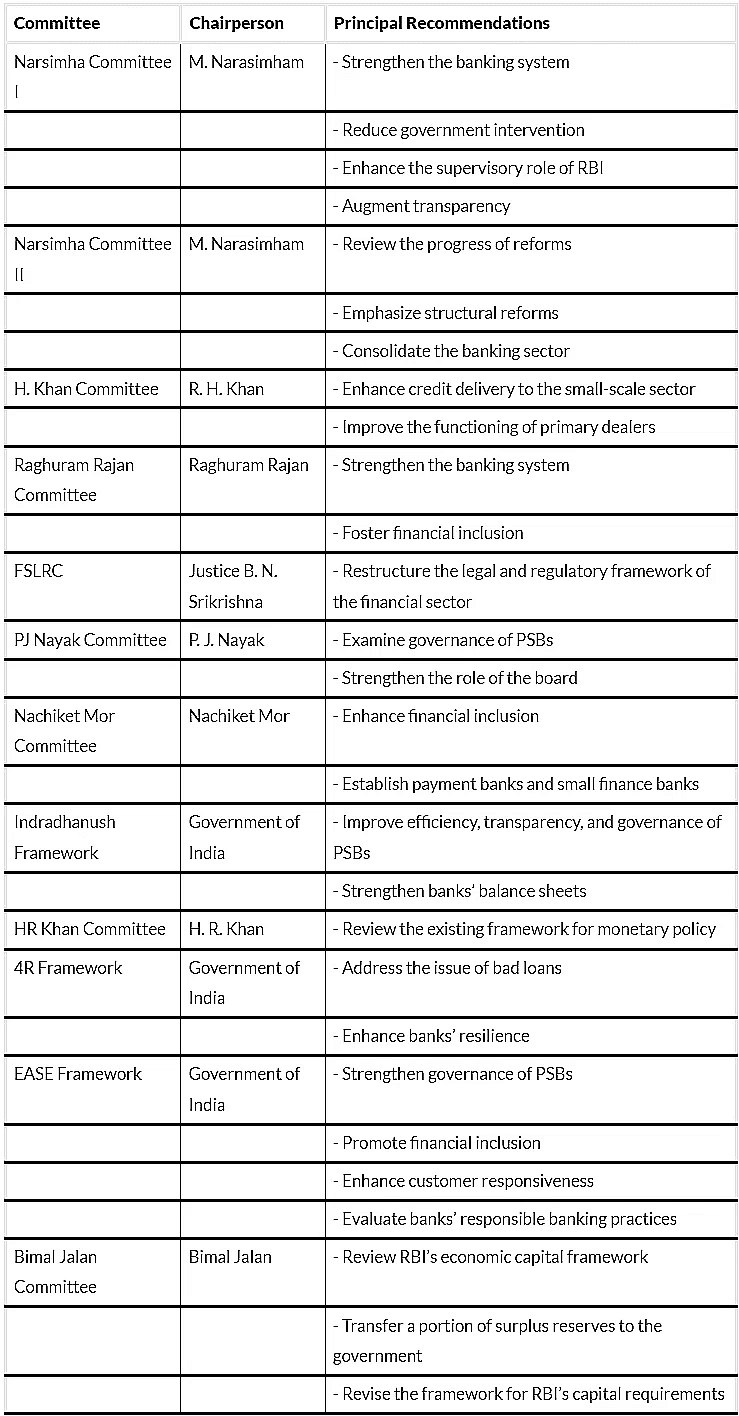

- Narsimham Committee I (1991): Chaired by M. Narasimham, former RBI Governor, this committee advocated strengthening the banking system. Recommendations included reducing government intervention, augmenting RBI's supervisory role, enhancing transparency, and revising liquidity norms. Additionally, it underscored the need for recapitalizing weak banks and enforcing prudential norms.

- R. H. Khan Committee (1997): Under the leadership of R. H. Khan, former Deputy Governor of RBI, this committee scrutinized the financial system's efficacy for the small-scale sector and primary dealers. It proposed measures to enhance credit delivery to the small-scale sector and refine primary dealers' operations.

- Narsimham Committee II (1998): Building on the earlier reforms, this committee emphasized structural changes, banking sector consolidation, and robust regulatory frameworks. Recommendations included reducing government ownership in PSBs, enhancing corporate governance, and adopting international accounting standards.

- Raghuram Rajan Committee (2008): Led by Raghuram Rajan, former IMF Chief Economist, this committee aimed to fortify the banking system, advance financial inclusion, and promote stability.

- Financial Sector Legislative Reforms Commission (FSLRC) (2011): Under Justice B. N. Srikrishna's leadership, FSLRC endeavored to revamp India's financial sector's legal and regulatory framework, aiming to consolidate and streamline laws governing banking, insurance, securities, and pensions.

- PJ Nayak Committee (2014): Headed by P. J. Nayak, this committee examined PSB governance, recommending reforms to fortify governance structures, empower bank management, and mitigate government interference.

- Nachiket Mor Committee (2014): Chaired by Nachiket Mor, this committee proposed comprehensive financial services for small businesses and low-income households, advocating for the establishment of payment banks, small finance banks, and universal electronic bank accounts.

- Indradhanush Framework (2015): Introduced by the Government of India, the Indradhanush framework aimed to revitalize PSBs, focusing on appointment procedures, Bank Board Bureau (BBB), capitalization, stress resolution, empowerment, accountability, and governance reforms.

- HR Khan Committee (2015): Led by H. R. Khan, this committee scrutinized India's monetary policy framework, making recommendations on inflation targeting, policy transmission, and decision-making processes.

- 4R Framework (2017): Part of the government's strategy to address mounting bad loans, the 4R framework aimed to recognize stressed assets, recapitalize banks, resolve stressed assets, and undertake structural reforms to enhance governance, risk management, and operational efficiency.

These reform initiatives collectively propelled India's banking sector towards greater resilience, efficiency, and inclusivity, laying a robust foundation for sustained growth and development.

Regulators

- The Finance Ministry constantly formulated major strategies in the field of financial sector of the country. The Government acknowledged the important role of regulators. The Reserve Bank of India (RBI) has become more independent.

- Securities and Exchange Board of India (SEBI) and the Insurance Regulatory and Development Authority (IRDA) became important institutions. Some opinions are also there that there should be a super-regulator for the financial services sector instead of multiplicity of regulators.

Forex Market Reform

- Forex market reform took place in 1993 and the successive adoption of current account convertibility were the acmes of the forex reforms introduced in the Indian market. Under these reforms, authorised dealers of foreign exchange as well as banks have been given greater sovereignty to perform in activities and numerous operations.

- Additionally, the entry of new companies have been allowed in the market. The capital account has become effectively adaptable for non-residents but still has some reservations for residents.

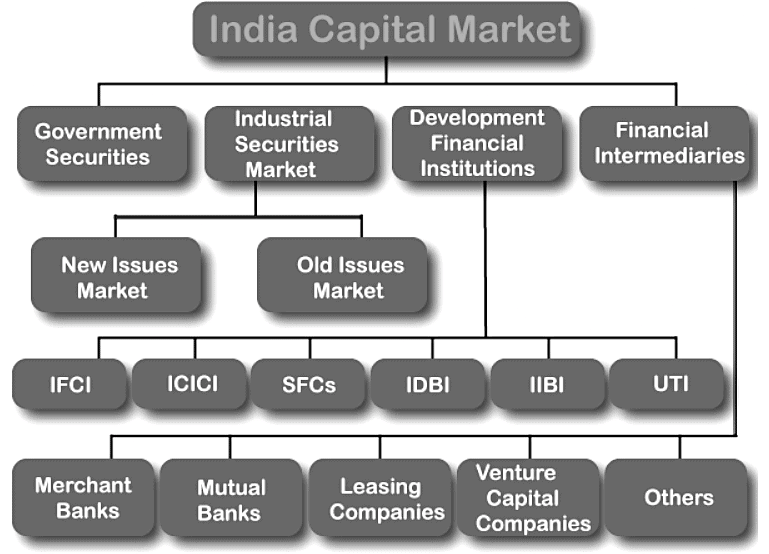

Capital Market Reform

- Capital market is defined as a financial market that works as a channel for demand and supply of debt and equity capital. It channels the money provided by savers and depository institutions (banks, credit unions, insurance companies, etc.) to borrowers and investees through a variety of financial instruments (bonds, notes, shares) called securities.

- A capital market is not a compact unit, but a highly decentralized system made up of three major parts that include stock market, bond market, and money market. It also works as an exchange for trading existing claims on capital in the form of shares. The Capital Market deals in the long-term capital Securities such as Equity or Debt offered by the private business companies and also governmental undertakings of India.

Structure of the capital market of India

- Within the realm of financial sector reforms, enhancing the capital market stands out as a crucial focus area, running parallel to the reforms in banking. Despite the Bombay Stock Exchange (BSE) boasting a century-long history of operation in India's capital markets, activity remained relatively subdued until the 1980s. However, there was a significant surge in capital market activity during that decade, with the market capitalization of BSE-listed companies soaring from 5% of GDP in 1980 to 13% by 1990. Subsequently, substantial reforms have been witnessed in the Indian capital market, particularly in the 1990s and beyond, propelling it towards further growth.

- Recognizing this pivotal juncture, both the Government of India and the Securities and Exchange Board of India (SEBI) undertook numerous measures to enhance the functioning of Indian stock exchanges, fostering progress and dynamism. Established in 1988 and accorded legal status in 1992, SEBI was tasked with regulating commercial banks, overseeing mutual fund operations, promoting stock exchange activities, and regulating new issue activities of companies. Its primary objective was to safeguard investors' interests in the securities market and related matters.

- SEBI's core functions encompassed controlling stock market activities, regulating self-regulatory organizations, combating fraudulent practices, enhancing investor awareness, preventing insider trading, and regulating significant share acquisitions and company takeovers. Despite these efforts, the stock market remained archaic and inadequately regulated. The cumbersome process of obtaining government approval for accessing the capital market and setting issue prices persisted, hindering market efficiency.

- The reform trajectory commenced in 1992, inspired by recommendations from the Narasimham Committee, aimed at dismantling direct government control in favor of a transparent, disclosure-based regulatory framework overseen by an independent regulator. The elevation of SEBI from a non-statutory body to a full-fledged capital market regulator with statutory powers in 1992 marked a significant milestone. This transition abolished the need for prior government permission and approval of issue pricing, granting companies the freedom to access markets and price issues independently, subject only to SEBI's prescribed disclosure norms.

Opening the Capital Market to Foreign Investors

A significant policy shift occurred in 1993, marked by the decision to open the capital market to foreign institutional investors (FIIs) and authorize Indian companies to raise capital abroad through the issuance of equity in the form of global depository receipts (GDRs).

Modernization of Trading and Settlement Systems

- In the realm of trading methods, substantial advancements were made to replace antiquated practices. The establishment of the National Stock Exchange (NSE) in 1994 heralded a new era as an automated electronic exchange. This innovation empowered brokers across 220 cities nationwide to connect with NSE computers via VSATs, enabling unified exchange with automatic matching of buy and sell orders based on price time priority, thereby ensuring maximum transparency for investors. The advent of electronic trading by the NSE spurred competitive pressures, compelling the Bombay Stock Exchange (BSE) to also adopt electronic trading in 1995.

- Meanwhile, the settlement system, characterized by physical delivery of share certificates to buyers and subsequent manual recording of ownership changes by company registrars, posed inefficiencies and significant risks for investors. The first step towards paperless trading commenced with legislative changes allowing dematerialization of share certificates and settlement via electronic transfer of ownership within a depository. This transformative move led to the establishment of the National Securities Depository Ltd (NSDL) in 1996, laying the groundwork for a more efficient and secure trading environment.

Futures Trading

- Presently, a notable gap in India's capital market lies in the absence of future markets. The establishment of a robust market in index futures would facilitate effective risk management and enhance market liquidity.

- A decision to introduce futures trading has been made, and the necessary legislative changes required for its implementation have been submitted to parliament.

Challenges in the Capital Market

- Despite numerous reforms in the regulatory framework and trading and settlement systems, the performance of the capital market in the post-reform era has faced significant criticism. Investors, particularly small investors who entered the market during the initial phases of liberalization, have not realized the expected value from their investments. It is perceived that several unscrupulous companies exploited the lack of government control over issue prices to raise capital at inflated prices, to the detriment of inexperienced investors. This situation involved merchant bankers and underwriters associated with these issuances.

- Furthermore, issuers of capital must recognize that the capital market should not be perceived merely as a passive source of equity capital accessible to companies at their discretion to raise equity under favorable terms. Cross-country studies indicate that stock markets in developing countries have played a vital role in financing new investments through Initial Public Offerings (IPOs), contrasting with developed countries where new investment financing has primarily relied on internal surplus generation. Typically, new companies seeking funds have turned to venture capital or private placement rather than resorting to public issues.

Mutual Funds

- Currently, the mutual funds industry operates under the purview of the SEBI (Mutual Funds) Regulations, 1996, along with subsequent amendments. These SEBI regulations provided a framework for the establishment of numerous companies, both domestic and foreign. While the Unit Trust of India remains the largest mutual fund, managing assets worth nearly Rs. 70,000 crores, its market share has been declining.

- With the burgeoning securities markets and the tax advantages associated with investing in mutual fund units, mutual funds have gained widespread popularity. Foreign-owned Asset Management Companies (AMCs) are now driving the industry forward by introducing innovative products, setting higher standards for customer service, enhancing disclosure norms, and exploring new distribution channels.

Reforming the Insurance Sector

- The insurance sector in India is governed by various legislations including the Insurance Act, 1938, the Life Insurance Corporation Act, 1956, the General Insurance Business (Nationalisation) Act, 1972, the Insurance Regulatory and Development Authority (IRDA) Act, 1999, and other related Acts. Just as the banking sector underwent liberalization and competition among public sector banks, Indian private sector banks, and foreign banks, similar principles apply to the insurance sector. There is a compelling argument for breaking the monopoly of public sector entities in insurance and allowing participation from private sector players, provided there is adequate prudential regulation in place.

- International data underscores the importance of contractual savings institutions in driving the overall savings rate, with insurance and pension schemes being crucial forms of contractual savings. A competitive insurance industry offering a diverse range of products tailored to different customer needs can stimulate savings and allocate them effectively. The insurance and pensions sector typically deals with long-term liabilities, which are matched by investments in secure long-term assets.

- A robust insurance sector serves as a significant source of long-term domestic currency capital, particularly crucial for infrastructure financing. Strengthening the insurance sector is expected to bolster the long-term segment of the capital market by introducing new players, thereby enhancing its depth and liquidity. Reforms in the insurance sector have the potential to channel finance to the corporate sector, provided efforts are made to reduce financial deficits concurrently.

- As early as 1994, the Malhotra Committee recommended opening up the insurance sector to new private companies. However, it took five years to reach a consensus on this matter, and legislation allowing foreign equity up to 26% in the insurance sector was finally presented to Parliament in 1999.

Overall Approach to Reforms

- Over the past several years, significant improvements have been observed in the operations of various contributors to the financial markets. Both the government and regulatory authorities have adopted a gradual approach to reform. The entry of foreign entities has facilitated the adoption of international practices and systems, while advancements in technology have bolstered customer service.

- Despite these advancements, certain gaps persist, such as the absence of an inter-bank interest rate benchmark, a vibrant corporate debt market, and a fully developed derivatives market. Nevertheless, the cumulative impact of developments since 1991 has been largely positive, evident in India's resilience during the Southeast Asian crisis.

Conclusion

The financial sector constitutes a vital component of the Indian economy. Financial experts advocate for effective reforms to maintain competitiveness and attractiveness to global investors. Economic reforms have shifted the policy focus towards promoting industries and building integrated infrastructure. Financial sector reforms have been at the forefront of India's economic liberalization since the mid-1990s. These reforms have included deregulating interest rates, dismantling directed credit, strengthening the banking system, and enhancing the functioning of capital markets, including the government securities market. Regulators and economists have placed particular emphasis on banking reforms to stimulate the economy and broaden access to financial services. The primary objective of financial sector reforms in the 1990s was to establish an efficient, competitive, and stable financial system capable of significantly contributing to economic progress.

FAQs on Recent Reforms in the Financial Sector - Management Optional Notes for UPSC

| 1. What is the importance of banking legislation and reform measures in India? |  |

| 2. What are some of the key banking sector acts in India and the years they were implemented? | |

| 3. How has the banking sector in India been reformed since 1991? | |

| 4. What are some recent reforms in the financial sector in India? | |

| 5. How has the capital market in India been opened to foreign investors? | |

MCQs

,Summary

,Important questions

,Semester Notes

,Recent Reforms in the Financial Sector | Management Optional Notes for UPSC

,Sample Paper

,Extra Questions

,Objective type Questions

,Exam

,ppt

,Previous Year Questions with Solutions

,video lectures

,past year papers

,Recent Reforms in the Financial Sector | Management Optional Notes for UPSC

,Viva Questions

,study material

,shortcuts and tricks

,mock tests for examination

,Recent Reforms in the Financial Sector | Management Optional Notes for UPSC

,Free

,practice quizzes

;

Recent Reforms in the Financial Sector Free PDF Download

Importance of Recent Reforms in the Financial Sector

Recent Reforms in the Financial Sector Notes

Recent Reforms in the Financial Sector UPSC Questions

Study Recent Reforms in the Financial Sector on the App

|

© EduRev

|

Education Revolution

|

|