Best Study Material for UPSC Exam

UPSC Exam > UPSC Notes > NCERT Video Summary: Class 6 to Class 12 (English) > Chapter Notes - Producer’s Equilibrium

Producer’s Equilibrium Class 12 Economics

Producer

A producer is an economic agent who produces goods and services for sale with the objective of

→ maximizing profit ; or → minimizing losses

Producer's Equilibrium

It refers to a situation where producer maximizes his profit or minimizes his losses.

⇒ It tells the level of output that producer should undertake to produce to achieve the objectiveof maximizing profit and at this level of output there is no incentive for firm either to increase or decrease output

Conditions of Producer's Equilibrium

A firm maximise profit that is difference between TR and TC at a level of output where two conditions are met

(a) MARGINAL REVENUE(MR) = MARGINAL COST (MC)

(b) MC BECOMES GREATER THAN MR AFTER EQUILIBRIUM LEVEL : In other words Marginal cost (MC) should be rising OR MC should cut MR from below (rising MC means that a firm achieves its profit maximising equil ibrium only in stage of diminishing return)

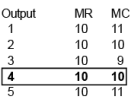

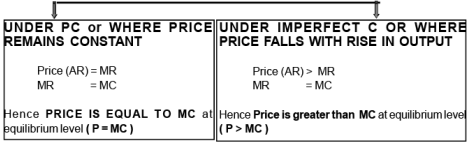

PRODUCER’S EQUILIBRIUM UNDER PERFECT COMPETITION

{WHEN MORE IS SOLD AT SAME PRICE}

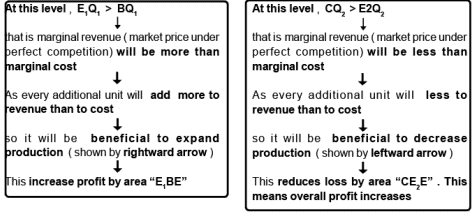

| First condition of MR = MC is satisfied at both 2nd and 4th level of output . But second condition MC > MR after equilibrium level (or MC is rising) is satisfied only at 4th level of output indicating that producing more will lead to decline in profits . Hence producer equilibrium is achieved at 4th level of output |

| Accordingly E is equilibrium point and OQ the profit maximising output .Thus the equilibrium point will be at point where MR = AR(Price) = MC. In other words in a perfect competitive market, the market price (P) should be equal to rising part of MC |

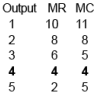

PRODUCER’S EQUILIBRIUM IMPERFECT COMPETITION

{WHEN MORE IS SOLD BY LOWERING THE PRICE}

| First condition of MR = MC is satisfied at both 2nd and 4th level of output . But second condition MC > MR after equilibrium level (or MC is rising) is satisfied only at 4th level of output indicating that producing more will lead to decline in profits. Hence producer equilibrium is achieved at 4th level of output |

⇒ Accordingly E is equilibrium point and OQ the profit maximising output.

| SPECIAL POINT :: Thus the equality of MR and MC is a necessary condition for equilibrium but it is not by itself sufficient to attain producers equilibrium. So first condition must be supplemented with the second condition to attain the producer’sequilibrium |

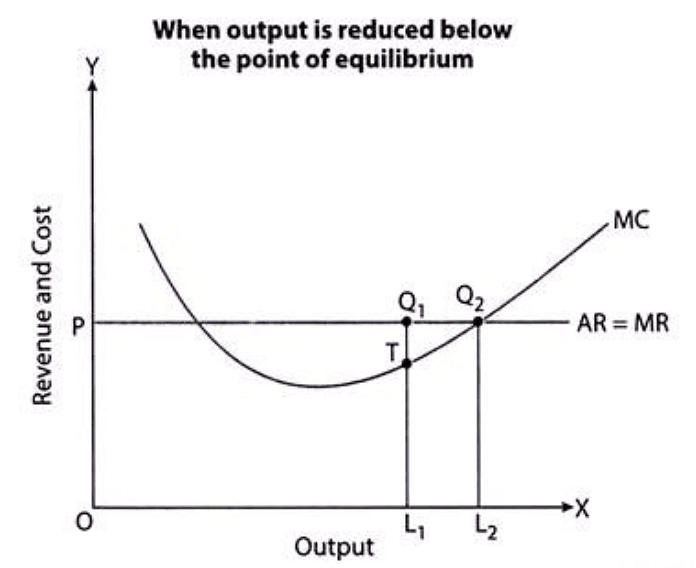

RELATION BETWEEN PRICE AND MC at EQUILIBRIUM

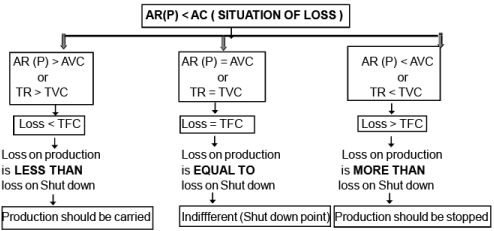

IN THE SHORT-RUN , A FIRM SHOULD PRODUCE IF AND ONLY IF AR (P) > AVC OR TR > TVC

IF a firm exercises the option of closing down and produces nothing , the losses would be equal to its fixed cost. Thus in short run a firm has to compare losses in the two situation -

(A) losses in a situation of shut down (that is loss of fixed cost) and

(B) losses if the firm continues to produce

| (Q1) Do producer always maximise their profit ? (Q2) Producer doesnot always work to maximise their profit ? (Q3) Should a producer stop production when producer means losses to him ? (Q4) Will a profit- maximising firm in a competitive market ever produce a positive level of output in the short run if the market price is less than minimum of AVC ? Give an explanation |

DIFFERENCE BETWEEN B.E.P & SHUT DOWN POINT

| B.O.D | BREAK EVEN POINT | SHUT DOWN POINT |

| Meaning | It refers to a situation when TR = TC or AR (P) = AC | It refers to a situation when TR = TVC or AR (P) = AVC |

| Situation | It i ndicates situation of no profit (abnormal) or no loss. Thus the Firm is able to earn only Normal profit that are included in COP | It i ndicates situat ion whe re firm is recovering only variable cost or the loss is equal to fixed cost |

| Decision | Since normal profit is there, firm carries on production | Producer is indifferent whether to suspend production or not . However in case of further rise in cost or Fall in price , The producer will stop production |

The document Producer’s Equilibrium Class 12 Economics is a part of the UPSC Course NCERT Video Summary: Class 6 to Class 12 (English).

All you need of UPSC at this link: UPSC

|

476 videos|360 docs

|

FAQs on Producer’s Equilibrium Class 12 Economics

| 1. What is producer's equilibrium? |  |

| 2. How is producer's equilibrium determined? | |

Ans. Producer's equilibrium is determined by comparing the marginal cost (MC) and marginal revenue (MR) of production. When MC equals MR, the producer is in equilibrium. This condition ensures that the producer is maximizing their profits by producing the optimal quantity of goods or services. If MC is less than MR, the producer should increase production, and if MC is greater than MR, the producer should decrease production.

| 3. What factors can shift a producer's equilibrium? | |

Ans. Several factors can shift a producer's equilibrium. Changes in input prices, such as the cost of labor or raw materials, can impact the producer's costs and, therefore, their equilibrium. Changes in technology or productivity can also affect the producer's equilibrium by altering their production costs. Additionally, changes in market demand for the producer's goods or services can impact the equilibrium, as it affects the marginal revenue received from sales.

| 4. What is the relationship between producer's equilibrium and profit maximization? | |

Ans. Producer's equilibrium is closely related to profit maximization. When a producer is in equilibrium, it means they are producing at the point where their marginal cost equals their marginal revenue. This balance ensures that the producer is maximizing their profits because any further increase or decrease in production would result in a decrease in overall profit. Therefore, reaching producer's equilibrium is crucial for profit maximization.

| 5. Can a producer be in equilibrium without maximizing their profits? | |

Ans. No, a producer cannot be in equilibrium without maximizing their profits. Producer's equilibrium occurs when the producer is producing the optimal quantity of goods or services to maximize their profits. If the producer is not maximizing their profits, it means they are either producing too much or too little. In either case, they would need to adjust their production levels to reach a new equilibrium that maximizes their profits.

Related Exams

About this Document

2.9K Views

4.92/5

Rating

Apr 28, 2025

Last updated

Document Description: Chapter Notes - Producer’s Equilibrium for UPSC 2025 is part of NCERT Video Summary: Class 6 to Class 12 (English) preparation.

The notes and questions for Chapter Notes - Producer’s Equilibrium have been prepared according to the UPSC exam syllabus. Information about Chapter Notes - Producer’s Equilibrium covers topics

like Producer, Producer's Equilibrium and Chapter Notes - Producer’s Equilibrium Example, for UPSC 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Chapter Notes - Producer’s Equilibrium.

Introduction of Chapter Notes - Producer’s Equilibrium in English is available as part of our NCERT Video Summary: Class 6 to Class 12 (English)

for UPSC & Chapter Notes - Producer’s Equilibrium in Hindi for NCERT Video Summary: Class 6 to Class 12 (English) course.

Download more important topics related with notes, lectures and mock test series for UPSC

Exam by signing up for free. UPSC: Producer’s Equilibrium Class 12 Economics

Description

Full syllabus notes, lecture & questions for Producer’s Equilibrium Class 12 Economics - UPSC | Plus excerises question with solution to help you revise complete syllabus for NCERT Video Summary: Class 6 to Class 12 (English) | Best notes, free PDF download

Information about Chapter Notes - Producer’s Equilibrium

In this doc you can find the meaning of Chapter Notes - Producer’s Equilibrium defined & explained in the simplest way possible. Besides explaining types of

Chapter Notes - Producer’s Equilibrium theory, EduRev gives you an ample number of questions to practice Chapter Notes - Producer’s Equilibrium tests, examples and also practice UPSC

tests

Related Searches

practice quizzes

,Summary

,ppt

,Exam

,mock tests for examination

,Important questions

,Producer’s Equilibrium Class 12 Economics

,Producer’s Equilibrium Class 12 Economics

,MCQs

,Producer’s Equilibrium Class 12 Economics

,study material

,past year papers

,Semester Notes

,video lectures

,Free

,shortcuts and tricks

,Sample Paper

,Previous Year Questions with Solutions

,Objective type Questions

,Viva Questions

,Extra Questions

;

Additional Information about Chapter Notes - Producer’s Equilibrium for UPSC Preparation

Chapter Notes - Producer’s Equilibrium Free PDF Download

The Chapter Notes - Producer’s Equilibrium is an invaluable resource that delves deep into the core of the UPSC exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Chapter Notes - Producer’s Equilibrium now and kickstart your journey towards success in the UPSC exam.

Importance of Chapter Notes - Producer’s Equilibrium

The importance of Chapter Notes - Producer’s Equilibrium cannot be overstated, especially for UPSC aspirants.

This document holds the key to success in the UPSC exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Chapter Notes - Producer’s Equilibrium

Chapter Notes - Producer’s Equilibrium Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Chapter Notes - Producer’s Equilibrium.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Chapter Notes - Producer’s Equilibrium Notes on EduRev are your ultimate resource for success.

Chapter Notes - Producer’s Equilibrium UPSC Questions

The "Chapter Notes - Producer’s Equilibrium UPSC Questions" guide is a valuable resource for all aspiring students preparing for the

UPSC exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Chapter Notes - Producer’s Equilibrium on the App

Students of UPSC can study Chapter Notes - Producer’s Equilibrium alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Chapter Notes - Producer’s Equilibrium,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Chapter Notes - Producer’s Equilibrium is prepared as per the latest UPSC syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup on EduRev and stay on top of your study goals

10M+ students crushing their study goals daily