B Com Exam > B Com Questions > Varma traders bought a machinery on 1st april...

Start Learning for Free

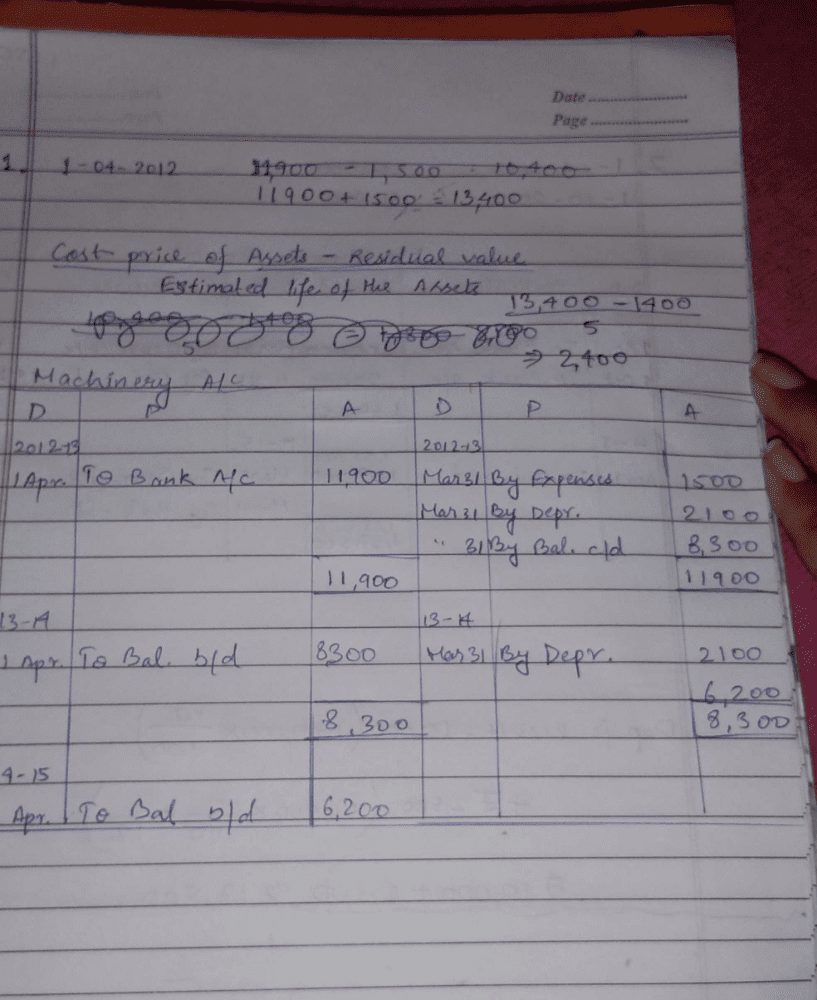

Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.?

Most Upvoted Answer

Varma traders bought a machinery on 1st april '2012 for rs 11900 and s...

Calculation of Annual Depreciation and Preparation of Machine Account

Fixed Instalment Method

Under the fixed instalment method, the annual depreciation is calculated by dividing the original cost of the machine minus its residual value by the estimated life of the machine.

Annual Depreciation = (Original Cost - Residual Value) / Estimated Life

Annual Depreciation = (Rs 11,900 - Rs 1,400) / 5 = Rs 2,100

Machine Account for the First Three Years

Year 1:

| Particulars | Amount (Rs) |

|---|---|

| Machine A/C (Original Cost) | 11,900.00 |

| Establishment A/C | 1,500.00 |

| To Bank A/C | 13,400.00 |

Depreciation A/C:

| Particulars | Amount (Rs) |

|---|---|

| Depreciation A/C | 2,100.00 |

| To Accumulated Depreciation A/C | 2,100.00 |

Year 2:

| Particulars | Amount (Rs) |

|---|---|

| Depreciation A/C | 2,100.00 |

| To Accumulated Depreciation A/C | 2,100.00 |

Year 3:

| Particulars | Amount (Rs) |

|---|---|

| Depreciation A/C | 2,100.00 |

| To Accumulated Depreciation A/C | 2,100.00 |

Explanation

The fixed instalment method of depreciation assumes that the asset will depreciate by the same amount each year. In this case, the annual depreciation is calculated by dividing the original cost of the machine minus its residual value by the estimated life of the machine. The annual depreciation is then charged to the depreciation account and credited to the accumulated depreciation account.

In the machine account, the original cost of the machine and the establishment expenses are debited to the account, while the amount paid for the machine is credited to the bank account. In the depreciation account, the annual depreciation is debited to the account, and the same amount is credited to the accumulated

Community Answer

Varma traders bought a machinery on 1st april '2012 for rs 11900 and s...

|

Explore Courses for B Com exam

|

|

Similar B Com Doubts

Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.?

Question Description

Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? for B Com 2025 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? covers all topics & solutions for B Com 2025 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.?.

Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? for B Com 2025 is part of B Com preparation. The Question and answers have been prepared according to the B Com exam syllabus. Information about Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? covers all topics & solutions for B Com 2025 Exam. Find important definitions, questions, meanings, examples, exercises and tests below for Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.?.

Solutions for Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? in English & in Hindi are available as part of our courses for B Com.

Download more important topics, notes, lectures and mock test series for B Com Exam by signing up for free.

Here you can find the meaning of Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? defined & explained in the simplest way possible. Besides giving the explanation of

Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.?, a detailed solution for Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? has been provided alongside types of Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? theory, EduRev gives you an

ample number of questions to practice Varma traders bought a machinery on 1st april '2012 for rs 11900 and spent rs 1500 on its establishment . the estimated life of the machine is five years. After which its residual value is estimated rs 1400. Calculate annual depreciation according to fixed instalment method and prepare machine account for first three years.? tests, examples and also practice B Com tests.

|

|

Explore Courses for B Com exam

|

|

Signup for Free!

Signup to see your scores go up within 7 days! Learn & Practice with 1000+ FREE Notes, Videos & Tests.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup