Economic Development: October 2024 Current Affairs | General Test Preparation for CUET UG - CUET Commerce PDF Download

Insolvency and Bankruptcy Board of India (IBBI)

Why in news?

The Insolvency and Bankruptcy Board of India (IBBI) has now mandated that Resolution Professionals (RPs) provide a copy of its report to both creditor and debtor in all cases.

Overview:

- The IBBI was established on October 1, 2016, following the provisions of the 'Insolvency and Bankruptcy Code, 2016'.

- It is tasked with executing the IBC, which consolidates and amends laws pertaining to the insolvency resolution of individuals, partnership firms, and corporate entities in a timely manner.

- The IBBI regulates the professional conduct and processes involved in insolvency cases.

- It oversees insolvency professional agencies, insolvency professional entities, insolvency professionals, and information utilities.

- The Board enforces regulations concerning corporate insolvency resolution, individual insolvency resolution, corporate liquidation, and individual bankruptcy under the IBC.

- Additionally, it has been designated as the 'Authority' under the Companies (Registered Valuers and Valuation Rules), 2017, to regulate and promote the profession of valuers in India.

About Insolvency and Bankruptcy Board of India (IBBI)

The IBBI is composed of members appointed by the Central Government, including:

- A Chairperson.

- Three members from officers of the Central Government, who must be of a rank not lower than Joint Secretary, each representing the Ministry of Finance, Ministry of Corporate Affairs, and Ministry of Law, ex-officio.

- One member nominated by the Reserve Bank of India (RBI), ex-officio.

- Five additional members nominated by the Central Government, with at least three being whole-time members.

- The term of office for the Chairperson and other members (excluding ex-officio members) lasts five years or until they reach sixty-five years of age, whichever comes first, and they are eligible for re-appointment.

What is Insolvency and Bankruptcy?

- Insolvency refers to a financial situation where an individual or entity is unable to meet their debt obligations as they come due.

- Bankruptcy is a legal process that occurs when an individual officially declares their inability to repay their debts to creditors.

FPIs Investment Exceeds USD 1 Trillion in Indian Securities.

Why in News?

Foreign portfolio investments (FPIs) into India have witnessed a significant reshuffling in the pecking order among regions. This transformation is attributed to various factors, including regulatory changes, geopolitical events, and strategic alliances.

What are the Significant Changes in India’s FPI Landscape?

Luxembourg's Ascendancy:

- Luxembourg has risen to become the third-largest source of Foreign Portfolio Investments (FPI) in India, overtaking Mauritius.

- Its Assets Under Custody (AUC) increased by 30%, reaching ₹4.85 lakh crore.

- Globally, Luxembourg now has the second-largest equity assets, just behind the United States.

- This growth is linked to stronger ties between India and Europe, marked by three key financial agreements.

- Luxembourg is home to over 1,400 FPI accounts out of approximately 3,000 in Europe (excluding the UK).

- Partnerships with places like GIFT City have further reinforced financial connections between India and Luxembourg.

France's Notable Gains:

- France has now entered the top ten countries for FPIs, seeing a significant 74% increase in its AUC, which has reached ₹1.88 lakh crore.

- This rise is mainly due to favorable tax rules under the Double Taxation Avoidance Agreement (DTAA) between India and France.

Other Players in the Reshuffled Landscape:

- Ireland and Norway have both moved up one spot, now ranking 5th and 7th in FPI jurisdictions.

- Ireland's appeal comes from its tax benefits and international reach, offering exemptions for regulated funds from Irish taxes on income and gains.

- Despite a 19% annual increase in AUC, Canada has dropped one position in the rankings, with the effects of ongoing diplomatic tensions between India and Canada on investments still unclear.

What is Foreign Portfolio Investment?

About:

- FPI includes investments from foreign individuals, companies, and institutions in Indian financial assets like stocks, bonds, and mutual funds.

- These investments are mainly aimed at short-term profits and diversifying portfolios, unlike Foreign Direct Investment (FDI), which involves long-term asset ownership.

Benefits:

- Capital Inflow: FPI leads to an influx of foreign money into Indian markets, enhancing liquidity and available capital.

- Boost to Stock Market: More FPI can positively affect the stock market, driving up valuations and increasing investor confidence.

- Technology Transfer: FPI often targets technology-focused sectors, facilitating the transfer of technology and advancements across various industries.

- Global Integration: FPI helps integrate Indian financial markets with the global landscape, aligning them with international trends and attracting foreign investors.

Risks:

- Market Volatility: FPI flows can be unstable, influenced by global economic and political factors.

- Sudden influxes or withdrawals can create market instability and currency fluctuations, affecting both domestic investors and the overall economy.

- Transparency Issues: It can be difficult for regulators to identify the ultimate beneficiaries of complex FPI structures, raising concerns about potential fund misuse and tax evasion.

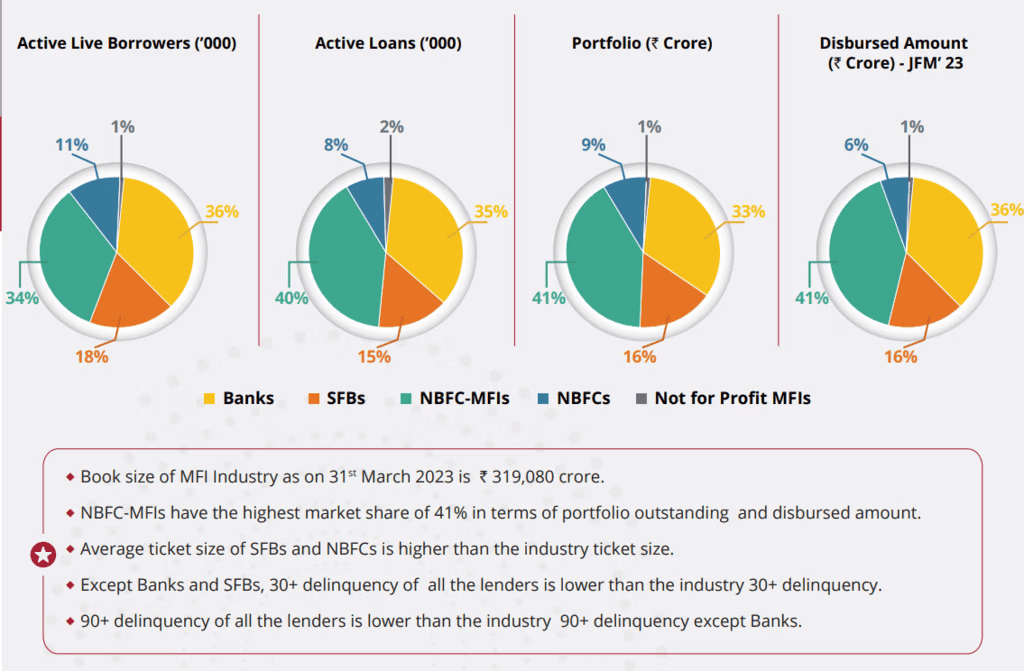

Microfinance Instituitions (MFIs)

Why in news?

The microfinance sector is gaining attention for its role in promoting financial inclusion, aiding the underserved populations by providing small loans and financial services. It significantly contributes to poverty reduction, empowers women, and fosters entrepreneurship, particularly in developing countries.

What is Microfinance?

- Microfinance involves offering financial services such as small loans, savings, and insurance to individuals and small businesses that do not have access to traditional banking.

- This sector is crucial for helping marginalized and low-income groups, especially women, to attain social equity and empowerment.

- In India, the microfinance sector has seen substantial growth, with 168 Micro Finance Institutions (MFIs) operating across 29 states and 4 Union Territories, serving over 30 million clients with a total loan portfolio of Rs. 46,842 crore.

Evolution of the Microfinance Sector in India:

- Initial Period (1974–1984): The Shri Mahila Sewa Sahakari Bank was established to provide financial services to women in the unorganized sector. NABARD promoted Self Help Group (SHG) linkage to alleviate poverty.

- Change Period (2002–2006): Norms for unsecured lending to SHGs were standardized with secured loans. In 2004, the Reserve Bank of India (RBI) recognized microfinance as part of the priority sector. However, allegations of high-interest rates led to the closure of some MFI branches.

- Growth and Crisis (2007–2010): Entry of private equity led to rapid growth in MFIs but also crises, notably in Andhra Pradesh, due to coercive collection practices resulting in borrower suicides. An Ordinance was issued to regulate MFIs.

- Consolidation and Maturity (2012–2015): The Malegam Committee's recommendations led to new RBI regulations. In 2014, Bandhan Bank received a universal banking license, and MFIN was recognized as a self-regulatory organization. The government also launched MUDRA Bank to support small businesses.

Status of Microfinance in India:

- Microfinance has created about 1.3 million jobs and contributes approximately 2% to the Gross Value Added (GVA) as per NCAER studies.

- It has the potential to serve 63 million unincorporated and non-agricultural enterprises. The RBI defines microfinance as collateral-free loans for households with annual incomes up to Rs. 3 lakh.

Business Models in Microfinance:

- Self-Help Groups (SHGs): Groups of 10–20 members, primarily women, pool savings to access credit from formal banking under the SHG-Bank Linkage Programme, supported by NABARD.

- Microfinance Institutions (MFIs): Provide micro-credit and other services like savings and insurance, often through Joint Lending Groups (JLGs) that consist of 4–10 members who share similar economic activities.

Categories of Microfinance Lenders:

- Non-Government Organizations (NGO-MFIs): Registered under the Society Registration Act 1860 or Indian Trust Act 1880, extending micro-credit.

- Co-operative Societies: Registered under relevant laws, offering microfinance services, such as Primary Agricultural Credit Societies (PACS).

- Section 8 Companies: Non-profit entities providing micro-credit under the Companies Act, 2013.

- Non-Banking Finance Companies (NBFC-MFIs): These institutions raise funds from their own resources or through bank loans to lend to JLGs, accounting for 80% of the microfinance market.

Regulatory Framework:

- The sector is regulated through the Non-Banking Financial Company-Micro Finance Institutions (NBFC-MFIs) framework established on 01.07.2014.

- This includes guidelines on eligibility for registration, client protection, preventing borrower over-indebtedness, privacy, and credit pricing, enhancing stakeholder confidence.

What are the Government Measures for the Development of Microfinance Institutions (MFIs)?

- Indian Micro Finance Equity Fund (IMEF): Launched in the 2011-12 Union Budget with an initial allocation of Rs. 100 crore, aimed at improving liquidity for smaller, socially-focused MFIs.

- Role of NABARD: NABARD's Micro Credit Innovations Department enhances access to financial services for the rural poor through various innovative microfinance initiatives.

- Self Help Group – Bank Linkage Programme (SHG-BLP): A cost-effective model that connects poor households with formal financial institutions.

- NABARD Financial Services Ltd. (NABFINS): Established as a model microfinance institution emphasizing governance, transparency, and reasonable interest rates.

- Micro Enterprise Development Programmes (MEDPs): Provide skill training for SHG members to improve production activities.

- E-Shakti Initiative: This initiative focuses on mapping existing SHGs and digitizing financial and non-financial information to improve accessibility and efficiency in financial inclusion.

- Pradhan Mantri MUDRA Yojana (PMMY): Launched to enhance credit flow to small businesses, a critical part of financial inclusion.

How does Microfinance Contribute to Financial Inclusion?

- Poverty Alleviation: Microfinance serves as a crucial mechanism for alleviating poverty by providing financial services to low-income populations, allowing them to diversify income and improve living conditions.

- Impact on Health, Social Capital, and Economy: Access to credit positively affects health and education, leading to economic development; for instance, access to credit for mothers can increase school enrollment rates.

- Microfinance as a Development Tool: It offers resilience against economic fluctuations, acting as a support system during crises.

- Opportunity for Commercial Banks: There is potential for commercial banks to innovate in microfinance, as MFIs often limit their product offerings, despite high recovery rates in this sector.

- Women Empowerment: Microfinance facilitates women's entrepreneurship, with many MFIs focusing on lending to women due to their higher repayment rates.

What are the Challenges and Way Forward for India’s Microfinance Sector?

- High outreach costs: Challenge in reaching remote areas; solutions include leveraging technology and partnering with local businesses.

- Over-indebtedness: A lack of proper assessment can lead to over-borrowing; addressing this requires enhanced risk assessment and financial education.

- Competitive disadvantage: MFIs face challenges competing with mainstream banks; potential solutions involve exploring alternative funding and advocating for regulatory reforms.

- Difficulty in acquiring reliable data: This complicates appraisals; standardized frameworks and investments in data analytics can help.

- Limited reach to the urban poor: Tailoring products and partnering with urban local bodies can improve access.

- Inadequate risk management practices: Improving credit risk assessment and promoting financial literacy are essential.

- Accessing clients in remote areas: Poor infrastructure can hinder access; mobile technology and local partnerships can assist.

- Operational flexibility: Vulnerability to changes in banking policies can be mitigated by building internal capacity and advocating for policy changes.

- Lack of awareness: Financial literacy campaigns and partnerships with educational institutions can help raise awareness.

- Limited product offerings: Expanding microinsurance and savings products can address the needs of low-wage workers.

Conclusion:

- The microfinance program has had a major effect on the Indian economy.

- It has shown that it can work well as a business model.

- This program has the ability to reach poor and marginalized groups.

- By supporting the banking system, it adds to sustainable microfinance services.

- It promotes inclusive development and economic fairness in India.

51st meeting of RBI Monetary Policy Committee

Why in News?

Recently, the Monetary Policy Committee (MPC) meeting of the Reserve Bank of India (RBI) was chaired by the RBI Governor.

What are the Key Decisions Taken at the 51 MPC Meeting?

- Unchanged Repo Rate: The MPC decided to maintain the repo rate at 6.5% for the tenth consecutive time.

- Change in Monetary Policy Stance: The MPC shifted its policy stance to 'Neutral' from 'withdrawal of accommodation'. This neutral stance provides the MPC with more flexibility to adjust monetary policy as required, whereas the previous stance was aimed at curbing inflation by restricting the money supply.

- Inflation Targets: The RBI has kept its Consumer Price Index (CPI) inflation forecast for FY2025 at 4.5%. The Flexible Inflation Targeting (FIT) framework, introduced in 2015, allows for temporary deviations from a target of 4% (+/- 2%) to support economic growth.

- Real GDP Growth Projections: The RBI maintained its real GDP growth projection for FY25 at 7.2%, indicating a resilient growth trajectory supported by private consumption and investment demand.

- Hike in UPI123PAY Transaction Limit: The RBI increased the transaction limit for UPI 123PAY from Rs 5,000 to Rs 10,000 and raised the UPI lite limit from Rs 500 to Rs 1,000. Additionally, the UPI lite wallet limit was increased from Rs 2,000 to Rs 5,000, facilitating payments for users with non-smartphones without needing internet connectivity.

- Reserve Bank-Climate Risk Information System (RB-CRIS): The RBI proposed the establishment of RB-CRIS, a data repository aimed at addressing the fragmented availability of climate-related data. This initiative will include a web-based directory of meteorological and geospatial data and a data portal with standardized datasets accessible to regulated entities.

- Direction of NBFCs: The RBI issued a strong advisory to non-banking financial companies (NBFCs), microfinance institutions (MFIs), and housing finance companies (HFCs) to foster a 'compliance first' culture focusing on adherence to regulations and effective customer grievance handling.

What is RBI's Stance on NBFCs in the 51 meeting of RBI MPC?

- Growth at Any Cost Approach: RBI Governor expressed concerns about a prevalent mentality among some NBFCs that prioritizes growth over sustainable business practices and robust risk management.

- Review of Compensation Practices: The RBI directed NBFCs to reassess their employee compensation structures, particularly regarding bonuses tied to short-term performance, to mitigate incentives for risky or unsustainable behaviors.

- Usurious Practices: There were raised concerns regarding NBFCs charging exorbitant interest rates and imposing high processing fees and penalties.

- Push Effect of Growth Targets: The RBI highlighted that aggressive growth targets could lead to retail credit growth that does not match actual demand, risking high indebtedness and financial stability.

- Investor Pressure: Some NBFCs, including MFIs and HFCs, are pressured by investors to achieve high returns on equity (RoE). The RBI urged these entities to pursue sustainable business goals instead of compromising long-term stability for short-term gains.

What are Non-Banking Financial Companies (NBFCs)?

- About NBFCs: A Non-Banking Financial Company (NBFC) is defined as a company operating under the Companies Act, 1956, primarily engaged in providing loans and advances, acquiring financial securities, and engaging in leasing and hire-purchase transactions. However, NBFCs do not include institutions whose main activities involve agriculture, industrial activities, the purchase or sale of goods (except securities), service provision, or dealing with immovable property.

- Criteria for Classification: An NBFC must conduct financial activities as its principal business, meaning over 50% of its total assets should be in financial assets, and income from these financial assets must also exceed 50% of its gross income. This is often referred to as the '50-50 test'.

- Differences Between Banks and NBFCs: Although NBFCs perform similar functions to banks, there are key differences: they cannot accept demand deposits, do not form part of the payment and settlement system, and cannot issue cheques drawn on themselves.

- Deposit Insurance Facility: Unlike banks, depositors of NBFCs do not have access to the Deposit Insurance and Credit Guarantee Corporation.

- Registration Requirements for NBFCs: Under the RBI Act, 1934, it is mandatory for every NBFC to obtain a certificate of registration from the RBI before commencing operations, with a minimum Net Owned Funds (NOF) of Rs 25 lakhs (or Rs 2 crore since April 1999) required for registration.

- Exemptions from Registration: Certain categories of NBFCs are exempt from RBI registration as they are overseen by other authorities, such as Venture Capital Funds (regulated by SEBI), Insurance Companies (regulated by IRDA), and Housing Finance Companies (regulated by NHB).

Recent Trends in NBFCs:

- In FY24, the assets under management (AUM) of NBFCs grew by 18% to Rs 47 trillion.

- The Non-Performing Assets (NPA) ratio stood at 2.6% as of June 2024, indicating a healthy growth rate of 18% annually.

Conclusion

- The 51st MPC meeting of the RBI focused on a neutral monetary policy stance while keeping its inflation target in mind.

- It stressed the need for NBFCs (Non-Banking Financial Companies) to follow sustainable practices instead of just pushing for rapid growth.

- The meeting reinforced the importance of compliance, responsible lending, and risk management to ensure long-term financial stability.

- Additionally, it announced that transaction limits for UPI (Unified Payments Interface) would be increased.

- The RBI insisted on compliance among NBFCs to support sustainable growth.

GDP Base Year Revision

Why in News?

Why in News?

Recently, the Ministry of Statistics and Programme Implementation (MoSPI) convened a group of economists and forecasters to discuss the revision of the base year for India’s Gross Domestic Product (GDP). This initiative highlights MoSPI's commitment to conducting broader consultations, particularly in light of past criticisms and debates regarding previous base year revisions. The last revision in 2015 transitioned the base year from 2004-05 to 2011-12 but was met with scrutiny due to perceived methodological flaws.

Previous Base Year Revision Controversies

- Methodological Concerns: The prior revision replaced the method of computing GDP for the private corporate sector (PCS) by utilizing audited balance sheets from the Ministry of Corporate Affairs (MCA) database, leading to the exclusion of the Index of Industrial Production (IIP) and Annual Survey of Industries (ASI) data.

- Single Deflator Criticism: Experts raised concerns about the use of a single deflator for calculating real GDP growth instead of the internationally accepted double deflation method, which uses various price indices for different outputs and inputs.

- Discrepancies in GDP Estimates: Although GDP growth appears strong, weak consumption suggests significant measurement issues, including discrepancies between production and expenditure methods of calculating GDP.

- Under-reporting of Data: Despite increased registrations of companies, especially in the service sector, many do not report to the Registrar of Companies (RoC), obscuring their contribution to domestic output.

- Underestimating Unorganised Sector: The 2015 revision faced backlash for inadequately incorporating data from the unorganised sector, leading to a lower representation of informal producers.

- Averaging Problem: Averaging production and expenditure is acceptable in developed nations but not in developing countries like India, where independent measures of both sides are lacking.

What is a Base Year?

- About Base Year: A base year serves as a specific reference point against which economic figures for subsequent and prior years are evaluated.

- Need for a Base Year: It provides a stable reference point and acts as a benchmark for assessing economic performance, facilitating comparisons over time.

- Features of a Base Year: The base year should be a normal year, devoid of abnormal events such as natural disasters, and must not be too distant in the past.

- Reasons for Revising the Base Year:

- Fluid Nature of Indicators: Economic indicators are dynamic, influenced by changing consumer behaviors and economic structures, necessitating revisions to reflect current realities.

- Impact on Economic Indicators: Incorporating new data through base year revisions can adjust GDP levels, affecting public expenditure, taxation, and public sector debt.

- International Standard Practice: The United Nations-System of National Accounts 1993 recommends periodic revisions of computation methods.

- Frequency of Base Year Revisions: Ideally, the base year should be updated every 5 to 10 years to align national accounts with the latest data.

- History of Base Year Revisions:

- Since the inception of national income estimates in 1956 (with FY 1949 as the base year), India has revised its base year seven times, with the latest change in 2015 from FY 2005 to FY 2012.

What are the Considerations for the New Base Year?

- Formation of the Advisory Committee: In June 2024, MoSPI established a 26-member Advisory Committee on National Accounts Statistics (ACNAS) to determine the new base year, chaired by Biswanath Goldar.

- Potential Base Years: The committee is inclined towards adopting 2022-23 as the new base year, with 2023-24 also under consideration, while years affected by significant economic events (like demonetization and GST) are not preferred.

- Utilising GST Data: Discussions are in progress regarding the inclusion of Goods and Services Tax (GST) data for a more comprehensive economic analysis.

- Methodological Improvements: The advisory committee is evaluating enhancements such as including data from the Annual Survey of Unincorporated Sector Enterprises (ASUSE) and possibly implementing the double deflation method for more accurate GDP measurement.

Conclusion

- The historical discussions around India's GDP base year changes have been controversial.

- The Ministry of Statistics and Programme Implementation (MoSPI) is now working to include expert opinions.

- These efforts aim to create a clear and methodologically sound way of estimating GDP.

- Improving the accuracy and trustworthiness of GDP estimates is a key goal.

- MoSPI is focusing on using updated data sources.

- They are also applying strict methods to ensure reliable results.

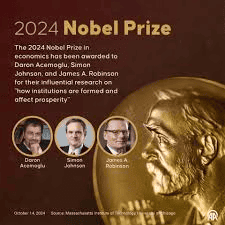

Nobel Prize for Economics 2024

Why in news?

The Nobel Prize in Economics for 2024 has been awarded to Daron Acemoglu, Simon Johnson, and James A. Robinson for their profound research on the formation of institutions and their impact on economic prosperity. Their studies shed light on the reasons behind the wealth disparity among nations, emphasizing the significance of institutional frameworks over simple geographical or cultural factors. The prize, amounting to 11 million kronor (approximately USD 1.1 million), will be distributed among the laureates in acknowledgment of their valuable contributions.

What are the Key Focus Areas of the Study?

- The research conducted by Acemoglu, Johnson, and Robinson delves into how varying institutional frameworks, especially in nations colonized by Europeans, have shaped economic outcomes.

- It was found that in regions where Europeans encountered high mortality rates, they were less inclined to settle and often established extractive institutions that have endured into modern times.

- The study argues that differences in institutions are crucial in determining economic success, rather than factors like geography or culture.

- An illustrative example is the divided city of Nogales, located on the US-Mexico border, where the economic opportunities and political rights on the US side vastly surpass those on the Mexican side.

What are the Key Facts About Winners?

- Simon Johnson: He gained prominence during his tenure at the International Monetary Fund (IMF) from 2007 to 2008 and currently serves as a professor at the Massachusetts Institute of Technology (MIT). He co-authored the book "Power and Progress: Our Thousand-Year Struggle Over Technology and Prosperity" (2023) with Daron Acemoglu. In his work, he emphasizes that poverty in many nations is rooted in entrenched political and economic institutions, making solutions complex and requiring long-term strategies.

- Daron Acemoglu: A professor at MIT, Acemoglu frequently collaborates with Johnson. He suggests that their research supports the notion that countries transitioning from authoritarian regimes often experience significant economic growth within 8 to 9 years, but cautions that democracy alone does not guarantee success. He co-authored "Why Nations Fail: The Origins of Power, Prosperity, and Poverty" (2012) with James A. Robinson.

- James A. Robinson: A professor at the University of Chicago and co-author of "Why Nations Fail" alongside Daron Acemoglu. Robinson has expressed skepticism about China's ability to sustain economic growth under its authoritarian regime, drawing parallels with historical instances such as the Soviet Union. He highlights that many societies, including the United States, have evolved into more inclusive societies by overcoming previous systems of oppression and privilege.

What is the Nobel Prize in Economic Sciences?

- About: Formally known as the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel, this prize was established in 1968 by the Swedish central bank. It complements the annual Nobel Prizes awarded in physics, chemistry, medicine, literature, and peace, which were founded according to Alfred Nobel's will.

- Other Economics Notable Laureates:

Year Recipient(s) Contribution 2023 Claudia Goldin Research on gender pay gaps. 2022 Ben Bernanke, Douglas Diamond, Philip Dybvig Work on banks and financial crises. 2019 Abhijit Banerjee, Esther Duflo, Michael Kremer Research on poverty alleviation. - Gender disparity in Nobel Prizes: The economics prize ranks as the second most male-dominated award after the physics prize, with only three women having received it. This reflects the historical underrepresentation of women in the fields of science and economics.

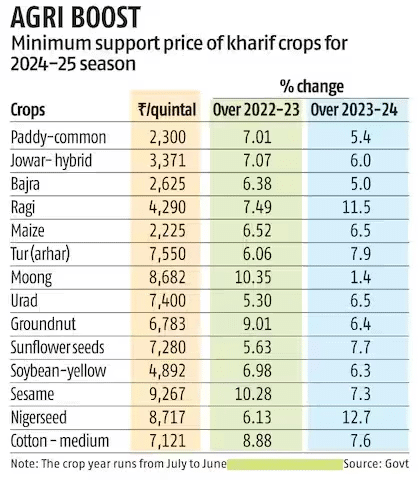

MSP and its Legalisation

Why in News?

The editorial titled ‘Legal guarantee for MSP is a must’ was published in The Business Line on 01/07/2024. It discusses the recent increases in Minimum Support Prices (MSP) for Kharif crops. Farmers are unhappy because the compensation they receive is not enough to cover their rising costs. MSP is not against free market principles; rather, it helps stabilize the market and reduce severe price swings. Recent MSP hikes for 14 crops have disappointed protesting farmers and those hoping to double their incomes.

- The price increases have been criticized for ignoring the inflation in farming expenses that farmers are currently facing.

- For example, the MSP for paddy rose from ₹2,183 per quintal to ₹2,300, only a small increase of ₹117, which is about 5%.

- This small increase feels unfair to many paddy farmers, as their costs have gone up by more than 20% in 2023.

- A report from a government expert committee in 2017 suggested that MSP announcements should be more than just routine price updates.

- There is a lack of clear progress in doubling farmers’ income, and the government has been reluctant to make MSP a legal requirement.

- Concerns exist that making MSP legal could lead to inflation and harm the competitiveness of agricultural exports.

What is the Minimum Support Price (MSP)?

- About: The MSP regime was established in 1965 by setting up the Agricultural Prices Commission (APC) as a form of market intervention to enhance national food security and protect farmers from significant decline in market prices.

- MSP Calculation: Commission for Agricultural Costs & Prices (CACP) calculates three types of production costs for every crop, both at the state and all-India average levels.

- A2: Covers all paid-out costs directly incurred by the farmer in cash and kind on seeds, fertilisers, pesticides, hired labour, leased-in land, fuel, irrigation, etc.

- A2+FL: Includes an estimated value of unpaid family labour with A2.

- C2: A comprehensive cost, which is A2+FL cost plus imputed rental value of owned land plus interest on fixed capital, rent paid for leased-in land.

- The government maintains that the MSP was fixed at a level of at least 1.5 times the all-India weighted average Cost of Production (CoP), but it calculates this cost as 1.5 times the A2+FL cost.

How can Legalising MSP help Indian Agriculture?

- Income Security for Farmers: A legally guaranteed MSP would provide farmers with protection against price fluctuations, ensuring that they receive a minimum price for their crops, which could stabilize their income and reduce the risk of financial distress.

- The average monthly income of agricultural households is around ₹10,695, often insufficient for a dignified life, contributing to the distress that leads to approximately 30 farmer suicides each day.

- Boost to Rural Economy: Improved price realization from government procurement and private sector transactions could enhance the purchasing power of rural communities, stimulating economic activity.

- Extending FRP Model and Direct Compensation: The model mandating private mills to procure sugarcane at or above the Fair and Remunerative Price (FRP) could be extended to other MSP-covered crops. Farmers should receive direct compensation if they are forced to sell below MSP, reimbursing them for the price difference.

- Legal Mandate for Private Crop Purchases: Private entities should be legally required to purchase crops at or above MSP, with rigorous monitoring systems and penalties for violations.

- Encouragement for Investment: With assured returns, farmers might be more inclined to invest in better farming techniques, leading to increased productivity and agricultural growth.

- Corporate-Centric Approach: When there is a conflict between consumer prices and farmer compensation, governments tend to favor profit-making corporations involved in agri-produce processing.

What are the Challenges Related to Farming and Legalising the MSP in India?

- Budgetary Concerns: Legalising MSP faces arguments regarding its feasibility, as the value of all crops under MSP may exceed ₹11-lakh crore, while India’s total budgeted expenditure was around ₹45-lakh crore in 2023-24.

- Farmers retain about 25% of their produce for personal use, complicating the implementation of a legal MSP.

- Complexity in Implementation: The challenge of creating legal provisions for MSP is exacerbated by India's vast array of crops and diverse agricultural landscape, making compliance and fair implementation difficult.

- Market Demand Mismatch in Agriculture: Farmers often lack mechanisms to anticipate market demand, leading to price volatility and uncertainty. For example, during the 2016 kharif season, government recommendations led to oversupply and price drops for pulses.

- Impact on Market Dynamics: Critics argue that improperly managed MSP could distort market dynamics, disincentivising private investment and innovation in agriculture.

- Limitations of APMC Law: The Agricultural Produce Market Committee (APMC) Act restricts farmers from selling their produce outside designated markets, leaving them vulnerable to middlemen and lacking access to efficient technologies.

Recommendations of Swaminathan Commission

- The commission recommends ensuring an MSP at least 50% higher than the weighted average cost of production, termed the 'C2+50% formula,' which includes the cost of capital and land rent.

- Recommendations of Ashok Dalwai Committee: The report suggests following the Model Agricultural Land Leasing Act to protect poor tenants and regulate rent.

- Comprehensive Policy Framework: A holistic national agriculture policy is needed, focusing on effective procurement policies and the five 'Cs' - Conservation of water and soil, Climate change resilience, Cultivation, Consumption, and Commercial viability.

- Need to Amend APMC Act: States should revise their APMC Acts to align with the Model Act and promote the formation of Self Help Groups and similar organizations for small and marginal farmers.

- Balancing Market Forces and Government Support: Acknowledging that while some agricultural segments can thrive through market forces, others require support through mechanisms like MSP.

- Assured Price to Farmers (APF): Implement an APF system that includes both MSP and a profit margin, ensuring fair returns for farmers based on C2 costs.

Categorisation and Implementation of MSP Crops

- Crops should be categorized based on their national and regional importance, with the central government overseeing the APF for all-India crops and states managing regionally important crops.

- Establishment of Commodity-based Farmers' Organisations: These organizations can provide guidance on global demand-supply projections, helping farmers make informed planting decisions.

- Comprehensive Cost Inclusion in MSP: The MSP should incorporate all production costs, ensuring farmers receive a price that covers basic expenses and a reasonable profit margin.

- Use of Evolving Technologies: Implementing electronic platforms like those in Karnataka can enhance price transparency and market access for farmers, potentially increasing their incomes.

Conclusion

- The agricultural sector has experienced many difficulties over the years.

- There is a strong need for a legal guarantee for Minimum Support Price (MSP) to help solve this crisis.

- Although an agreement was made with farmers who were protesting, the Central Government has not taken significant action in the past two years.

- The government should have quickly responded to the demand for a legal guarantee for MSP.

- Other important issues also need to be addressed to shift the country's focus from food security to nutrition security.

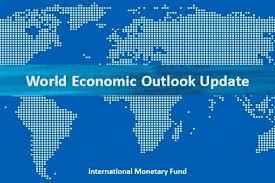

World Economic Outlook Report

Why in News?

Recently, the International Monetary Fund (IMF) released its World Economic Outlook (WEO) report for October 2024. In this, the IMF reaffirmed India's growth projections at 7% for FY2024 and 6.5% for FY2025.

Key Highlights of the WEO Report:

- India Specific Findings:

- Growth Projections: The report estimates India's growth for the current fiscal year, showing a decrease from 8.2% in FY 2023-24. This reduction is attributed to the waning of pent-up demand following the pandemic as the economy adjusts back to its potential growth path.

- Inflation: Headline inflation in India is predicted to decrease, with projections of 4.4% for FY 2024-25 and 4.1% for FY 2025-26. This trend reflects a global decrease in inflation rates after they peaked during the pandemic.

- Domestic Demand: Despite a global slowdown, India's consumption and investment remain robust, bolstered by domestic policies and a favorable investment environment. The Reserve Bank of India (RBI) has kept its growth projection for the current financial year at 7.2% due to strong domestic consumption. These factors might indirectly influence India’s growth trajectory through potential external shocks.

- Global Growth Projections:

- Global growth is expected to stabilize at 3.2% for both 2024 and 2025. The IMF forecasts the U.S. economy to grow by 2.8% in 2024 and 2.2% in 2025, while China's economy is projected to expand by 4.8% in 2024 and 4.5% in 2025.

- Sectoral Shifts:

- Prices of goods continue to exceed those of services due to the pandemic, with a global shift anticipated towards greater consumption of services. Additionally, the global automotive sector is evolving as it transitions to electric vehicles (EVs), which may lower emissions but could also lead to job losses in capital-heavy manufacturing sectors.

Challenges Highlighted by the WEO Report:

- Global Economic Slowdown: Medium-term global growth forecasts remain subdued due to factors such as aging populations, weak investment, and slow productivity growth. Geoeconomic fragmentation and trade tensions are significant threats to global supply chains and market efficiency.

- Social Resistance to Reforms: Structural reforms, although essential, often face substantial public opposition rooted in distrust, misinformation, and behavioral factors rather than purely economic concerns.

- Fiscal Constraints and Debt: High debt levels, particularly in low-income and emerging market nations, necessitate careful debt management to prevent fiscal crises.

- Climate and Energy Transition: The shift to clean energy is crucial but demands significant investment and support, which poses challenges for many economies facing fiscal pressures.

Key Recommendations Suggested by the WEO Report:

- Structural Reforms: Policymakers should focus on reforms in health, education, labor markets, and digitalization to alleviate productivity constraints and promote long-term growth.

- Social Acceptability Framework: Reform initiatives should include public consultations, foster trust, and ensure transparent communication to enhance social acceptance.

- Fiscal Policy Adjustments: Countries are encouraged to pursue gradual and credible fiscal adjustments to maintain debt sustainability while avoiding drastic cuts that could hinder growth. Continued public investments, especially in the digital and infrastructure realms, are essential for supporting growth.

- Climate Resilience and Green Investments: Expanding climate financing for vulnerable nations and implementing carbon pricing policies alongside WTO-compliant green subsidies are critical for advancing the green transition.

State Contingent Debt Instruments (SCDIs)

Why in news?

The Global Sovereign Debt Roundtable (GSDR), which addresses challenges in debt restructuring processes, is set to discuss State Contingent Debt Instruments (SCDIs).

SCDIs:

- It helps speed up debt restructuring by providing bonds that offer returns based on whether countries achieve certain economic or fiscal goals.

- For example, GDP-linked bonds issued by Ukraine are connected to the country's economic growth.

- These bonds do not have a fixed interest rate.

- The payment structure changes based on factors like economic growth, natural resource revenue, or tax income.

- SCDIs serve as "deal accelerators", particularly in situations where there are major disagreements about a country's economic future.

GSDR:

- GSDR, which is co-chaired by the IMF, World Bank, and the G20 Presidency (currently Brazil), began its operations in 2023.

- The group includes official bilateral creditors, which consist of both traditional members of the Paris Club and new creditors.

- It also involves private creditors and countries that are borrowing money.

- The Paris Club, established in 1956, is an informal group of creditor nations that collaborate to assist countries facing financial challenges, especially those having trouble repaying debts.

Conclusion

- The Global Sovereign Debt Roundtable's GSDR emphasis on State Contingent Debt Instruments (SCDIs) presents a modern solution for tackling issues related to debt restructuring.

- By using tools such as GDP-linked bonds, SCDIs connect debt repayments to how well a country's economy is doing. This creates more flexibility, which can help speed up the process of reaching restructuring agreements.

- This method is especially important during times of economic uncertainty, serving as a "deal accelerator" to bridge the gap between the interests of creditors and borrowing nations.

- Under the guidance of key organizations like the IMF, World Bank, and the G20 Presidency, along with the participation of both traditional and new creditors, the GSDR's initiatives on SCDIs show potential for creating more effective and robust debt restructuring processes in the global financial system.

Threat to Indian Online Gaming Sector

Why in news?

According to a report from the Digital India Foundation (DIF), money laundering poses a significant threat to the integrity and future viability of the Indian online gaming sector.

Key Points of the Report

- International Online Betting Threats: The report titled "Combating Money Laundering in Online Gaming Ecosystem" emphasizes the increasing trend of utilizing international online betting platforms for money laundering and terror financing in the context of cybercrime.

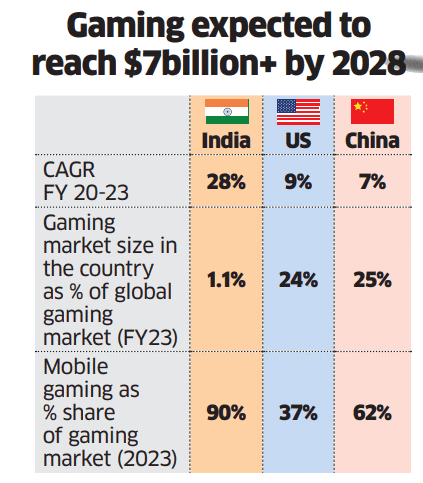

- Sectoral Growth: The online gaming industry in India is experiencing rapid growth, boasting a Compound Annual Growth Rate (CAGR) of 28% from FY20 to FY23, with projected revenue reaching USD 7.5 billion in five years.

- Employment Generation: With 568 million gamers in India, the sector is creating significant employment opportunities across diverse fields such as fintech, cybersecurity, and cloud services. It is anticipated to generate 250,000 jobs by 2025, alongside the emergence of over 400 startups and 100 million daily online gamers.

- Vulnerabilities and Risks: The report identifies several mechanisms employed for money laundering in the online gaming sector, including:

- Illegal operators: Many platforms circumvent regulations using mirror sites and Virtual Private Networks (VPNs).

- In-game currencies and assets: Frequently exploited for illicit activities.

- Cryptocurrencies: Offer anonymity and facilitate international money laundering.

- Mule accounts: Accounts used to disguise the source of illegal funds during transactions.

- Smurfing and money dumping: Techniques involving small transactions to evade detection.

What is Online Gaming?

- About: Online gaming refers to playing video games with other players through the internet, allowing for real-time interaction and competition across various platforms such as computers, gaming consoles, or smartphones.

- Classification: Online games can be categorized into:

- Skill-Based Games: Legal in India, these games prioritize skill over chance, such as Game 24X7, Dream11, and Mobile Premier League (MPL).

- Games of Chance: These games are determined primarily by luck rather than skill, like Roulette, where players are often attracted by the potential for monetary rewards.

Current Scenario:

- Youth Demographics: India has over 600 million individuals under 35 years old, making up 45% of the population and driving growth in the gaming industry.

- Smartphone Penetration: Smartphone usage has reached 75%, enhancing access to gaming and increasing user engagement. Mobile gaming constitutes 90% of total gaming revenue, predominantly through free-to-play models and in-app purchases.

- E-sports Growth: E-sports viewership in India has jumped to over 80 million, supported by government initiatives and a growing number of professional gamers.

What are the Challenges to the Gaming Sector?

- Financial Integrity Issues: The illegal betting market in India attracts over USD 100 billion in deposits annually, raising concerns regarding financial integrity due to the ease of asset transfers and conversions that fuel money laundering and fraud.

- Cybersecurity Threats: The risk of cyber attacks threatens user safety and data protection in gaming, compounded by users bypassing restrictions with VPNs and geo-blockers to access illegal gambling sites.

- Misuse of In-Game Assets: The potential misuse of in-game assets and cryptocurrencies poses regulatory challenges.

- Operation of Illegal Offshore Platforms: The existence of illegal offshore online betting sites complicates regulatory efforts.

- Circumvention of Regulations: Many platforms evade existing regulations through mirror sites, illegal branding, and misleading claims, indicating a need for stronger regulatory oversight and enforcement.

What can be the Risk-mitigation steps?

- Establishment of Taskforce: Form a dedicated taskforce of experts to propose policy measures for improved regulation of the gaming sector.

- Mandatory Registration: Require all online and offshore Real Money Gaming (RMG) operators to register under the Central Goods and Services Tax Act, 2017, within 30 days of becoming liable.

- Creation of a Whitelist: Publish and regularly update a list of legal online RMG operators to ensure that payment gateways, hosting providers, and ISPs cater exclusively to these operators.

- Advertising Advisory: The Information and Broadcasting Ministry should issue advisories restricting advertisements to only those online gaming applications that are on the whitelist.

- Collaboration with Financial Institutions: Partner with banks and payment service providers to establish protocols for blocking transactions to known illegal gambling operators.

- Cross-Border Cooperation: Take the lead in developing multilateral agreements with international organizations and other nations to bolster cooperation against illegal online gambling.

SEBI Tightens Futures and Options (F&Os) Rules

Why in News?

SEBI has introduced a six-step framework to protect investors and curb speculative trading, specifically targeting futures and options (F&O) trading by reducing volumes on expiry days and limiting retail participation.

What are the Future and Options (F&O)?

- Futures are agreements to purchase or sell an asset, such as stocks, indexes, or commodities, at a specific price on a future date.

- Options provide the ability, but not the requirement, to buy or sell an asset at a predetermined price before a certain deadline.

SEBI’s Six-Step F&O Framework (Effective November 2024 – April 2025):

- Upfront collection of options premiums: Traders will need to pay the cost of options at the start.

- Intraday monitoring of position limits: There will be close observation of how many positions traders hold during the day.

- Removing calendar spread benefits on expiry day: Benefits related to calendar spreads will not be available on the day options expire.

- Increasing contract size for index derivatives: The size of contracts for index derivatives will be made larger.

- Rationalizing weekly index derivatives: There will be only one standard index for weekly derivatives per exchange.

- Enhancing margin requirements on options expiry days: Higher margin amounts will be needed on the days when options expire.

Key Changes for Retail Investors:

- Upfront Premium Payments: Retail investors are now required to pay the entire options premium in advance, which limits their ability to use a lot of leverage when trading options.

- Higher Minimum Contract Size: The lowest contract size for index derivatives has increased to ₹15 lakhs, making it more expensive to participate and reducing speculative trading among retail investors.

- Changes to Weekly Expiries: Only one main index on each exchange will be allowed to have weekly expiries, which decreases opportunities for speculative trading and reduces daily market fluctuations.

- Elimination of Calendar Spread Advantages: Calendar spreads are no longer permitted on expiry days, which discourages traders from using aggressive trading strategies.

Impact on Brokers and Revenue:

- Decline in Trading Volumes: Brokers that depend on F&O trading will experience a drop in trading volumes because there are fewer retail traders participating and there are higher hurdles for entry.

- Revenue Drop in Options Trading: Companies like Zerodha might see a decrease in revenue ranging from 30% to 50% as fewer retail investors take part in options trading.

- Shift to Equity Trading: Retail investors are likely to move their focus to equity trading, which will require brokers to change their services and offerings.

- Adaptation for Brokers: Brokers that have a good balance between cash and derivatives will face less impact, while those that concentrate mainly on F&O will need to change their strategies.

Difficulties in Increasing Life Expectancy

Why in News?

After decades of steady increases in human life expectancy due to advancements in medicine and technology, recent trends suggest that these gains are starting to slow down, according to a new study.

The Key Findings of the Study:

- Slowing of Life Expectancy Gains: After many years of increasing life expectancy due to improvements in medicine and technology, the rate of these increases has greatly slowed down. The study indicates that human life expectancy has almost leveled off, and significant increases are unlikely without major advances in anti-aging medicine.

- Regional Analysis: The research looked at life expectancy data from 1990 to 2019 in areas known for having the longest lifespans, such as Australia, Japan, and Sweden.

- In these regions, the average life expectancy rose by only 6.5 years over the 29-year span.

- Challenges of Radical Life Extension: Researchers discovered that even though healthcare improvements allow people to live longer, the aging process of the human body—characterized by the decreasing function of internal organs—limits how long people can live.

- Even if diseases like cancer and heart disease are cured, aging itself still poses a significant challenge.

- Low Probability of Reaching 100: The study estimates that girls born in the longest-living regions have only a 5.3% chance of living to be 100 years old, while boys have a 1.8% chance. Therefore, despite advances in medicine, living to 100 remains uncommon without methods to slow down aging.

- Aging as the Primary Barrier: Researchers believe that to significantly increase average life expectancy, it is essential to find breakthroughs that can slow the aging process, rather than just improving treatments for common illnesses.

- Some experimental drugs, like metformin, have shown promise in animal studies, but human testing is still necessary.

India’s Present Status:

- Current Life Expectancy: As of 2024, the average life expectancy in India is about 70 years. This is lower compared to countries like Japan and Switzerland, where people live to over 83 years.

- Healthcare Improvements: India has made notable strides in fighting infectious diseases and enhancing maternal and child health. However, there is a rising concern as chronic illnesses and lifestyle diseases, such as heart disease and diabetes, are becoming the main reasons for death.

Way forward

- Focus on Anti-Aging Research: India needs to put more money into studying aging and regenerative medicine. This means finding ways to slow down how we age instead of just treating illnesses that come with age.

- Strengthening Healthcare Systems: By improving access to good healthcare and preventive medicine, we can better manage diseases related to aging. This will help improve people's quality of life as they grow older, even if they don't live significantly longer.

- Policy Support for Longevity Research: There is a need for rules and policies that back medical research aimed at technologies for extending life. This includes supporting drug trials and clinical studies that focus on aging.

- Public Health Interventions: Enhancing public health efforts to tackle lifestyle diseases like obesity and diabetes, as well as improving management of age-related health issues, can lead to longer lives and better overall health.

Ensuring Railway Safety

Why in News?

The turmoil has not subsided since the tragic accident involving the GFCJ container train, which, while travelling at high speed, collided with the 13174 Agartala-Sealdah Kanchanjunga Express, resulting in 11 deaths and approximately 40 injuries.

Indian Railways: Recent Issues

- Tragic Accident: A container train operated by GFCJ crashed into the 13174 Agartala-Sealdah Kanchanjunga Express, resulting in 11 deaths and approximately 40 injuries.

- Premature Conclusions: The Chairperson of the Railway Board quickly blamed the container train crew and shared incorrect information regarding the number of casualties.

- Slow Rollout of Kavach System: The Kavach system, which is a local signalling technology designed to prevent accidents, has been slowly introduced due to limited industrial capacity.

- Staffing Issues: Although Indian Railways has a large workforce, there are significant gaps in safety-related positions. This situation leads to stress and overwork among the current staff members.

- Ambiguous Protocols: The unclear rules for managing failures in Automatic signals create confusion and raise the chances of accidents occurring.

What are the major challenges that Indian Railways faces?

- Safety Concerns: There are not enough measures in place to stop accidents and ensure overall safety, even with new technology available.

- Staffing Shortages: There are important job openings that need to be filled, such as train drivers, train managers, and signal maintainers, which results in staff being overworked.

- Slow Technological Implementation: The rollout of safety technologies, like the Kavach system, is taking longer than expected because of limited resources in the industry and a lack of attention to these issues.

- Ambiguous Safety Protocols: The rules for dealing with signal failures and emergencies are poorly written and not clear, leading to confusion.

- Managerial and Communication Issues: Quick judgments and poor communication from higher management weaken trust and make it harder to manage crises effectively.

What can be the solution?

- Improved Safety Procedures: Make the rules for dealing with automatic signal failures and emergencies clearer and more effective.

- Faster Technology Use: Speed up the use of safety technologies like the Kavach system, aiming to cover between 4,000 and 5,000 kilometers each year.

- Boost Recruitment in Key Areas: Quickly hire new staff for important safety positions to lessen the pressure on current employees.

- Support Industrial Growth: Help and motivate related industries to enhance their ability to produce and implement safety technologies.

- AI-Powered Safety Monitoring: Use AI tools to examine digital information from station loggers and train microprocessors to gain useful safety insights.

- Emphasize Managerial Responsibility: Make sure that any issues related to management are thoroughly looked into and resolved to better safety management overall.

Steps taken by the government:

- The government has created the Rashtriya Rail Sanraksha Kosh (RRSK), a special fund with a total of Rs. 1 lakh crore over the next 5 years, aimed at financing the replacement, renewal, and upgrading of essential safety assets.

- As of May 2023, the government has installed Electrical/Electronic Interlocking Systems at 6,427 stations. These systems manage points and signals from a central location to reduce accidents caused by human mistakes.

- It is important to improve safety protocols for dealing with signal failures and emergencies. This includes providing clear guidelines and proper training for staff members.

- There is a need to speed up the use of safety technologies such as the Kavach system, with a goal of implementing it over 4,000 to 5,000 km each year to enhance overall safety and lower the chances of collisions.

|

164 videos|800 docs|1160 tests

|

study material

,Economic Development: October 2024 Current Affairs | General Test Preparation for CUET UG - CUET Commerce

,video lectures

,Viva Questions

,Economic Development: October 2024 Current Affairs | General Test Preparation for CUET UG - CUET Commerce

,Semester Notes

,Extra Questions

,shortcuts and tricks

,Summary

,Important questions

,ppt

,practice quizzes

,Free

,Previous Year Questions with Solutions

,Economic Development: October 2024 Current Affairs | General Test Preparation for CUET UG - CUET Commerce

,Exam

,Objective type Questions

,past year papers

,Sample Paper

,MCQs

,mock tests for examination

;

Economic Development: October 2024 Current Affairs Free PDF Download

Importance of Economic Development: October 2024 Current Affairs

Economic Development: October 2024 Current Affairs Notes

Economic Development: October 2024 Current Affairs CUET Commerce Questions

Study Economic Development: October 2024 Current Affairs on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!