Ramesh Singh Summary: Introduction to Economics- 1

Introduction

Economics is the systematic study of the production, allocation and consumption of goods and services. Because resources (land, labour, capital and entrepreneurship) are limited relative to human wants, economists study how individuals and societies manage limited resources. In 1935, Lionel Robbins summarised this viewpoint by defining economics as the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses.

More than a Dismal Science

- Economics is often referred to as the "dismal science," criticized for being difficult to understand by the general public and even university-educated individuals.

- Despite its criticisms, economics plays a crucial role in improving the world.

- Understanding economics can be challenging, especially for those without a background in the subject.

- Merely knowing economics is not sufficient; the ability to apply economic concepts in everyday life is essential.

- The book on the Indian economy intertwines economic theory with analyses of economic issues, emphasizing the importance of understanding footnotes and the glossary for a comprehensive grasp of the subject matter.

Defining Economics

- Economics examines human economic activities-actions involving production, exchange and consumption of goods and services.

- Human activities are interlinked; an interdisciplinary approach (history, political science, sociology) strengthens economic understanding.

- The economic activities are:

(i) All activities involving money are considered economic activities.

(ii) Where money is involved, there is an economic motive or gain.

(iii) Examples include getting a job, buying and selling, conducting business, etc. - Complexities do exist in Defining Economics:

(i) Defining economics is complex and contentious.

(ii) Common definitions revolve around resource use and distribution.

(iii) Two acclaimed definitions focus on how societies use resources and make choices. - Core Definitions of Economics have been given as:

(i) "Economics is the study of how societies use resources to produce valuable commodities and distribute them among different people."

(ii) "Economics studies how individuals, firms, governments, and organizations make choices that determine a society's resource utilization."

Try yourself: What is the core purpose of economics?

Micro and Macro

- After the Great Depression in the 1930s, economics split into:

(i) Microeconomics, and

(ii) Macroeconomics. - John Maynard Keynes is known as the father of macroeconomics, which emerged with his book "The General Theory of Employment, Interest and Money" in 1936.

- Microeconomics focuses on specifics (trees), while macroeconomics deals with the bigger picture (forest).

- Micro analyzes the economy from the bottom-up, while macro takes a top-down approach.

- Macro examines inflation and growth dynamics, while micro looks at consumer choices and income.

- Although distinct, micro and macro are interconnected, with overlapping issues like the impact of inflation on raw material costs and consumer prices.

- Micro theory explores price determination, while macro is based on observations unexplained by existing theories.

- While micro lacks competing schools of thought, macro includes schools like New Keynesian and New Classical.

- Econometrics, the third core area of economics, applies statistical and mathematical methods to economic analysis.

- Advancements in econometrics have facilitated sophisticated analyses in micro and macroeconomics.

What is Economy?

- An economy is the organised system of production, distribution and consumption of goods and services for a defined group (a country, a firm, a family).

- Principles of economics are generally the same across economies, but outcomes differ because of institutional, social and historical factors.

Sectors and Types of Economies

Economic activities in a country/economy are broadly divided into three main sectors and derive their types by the dominant form of economies they operate.

(A) Primary Sector

- It comprises economic activities involving natural resource exploitation such as mining, agriculture, and oil exploration.

- Although agriculture remains vital, its share in India's GDP has been declining. However, it still employs about 50% of the population, underscoring its importance.

(B) Secondary Sector

- It encompasses economic activities involving the processing of raw materials from the primary sector (industrial sector).

- Sub-sector, manufacturing, serves as the primary employer in many Western developed nations, leading to their industrialization.

- India's industrial sector is estimated to grow by 6.2% in FY25, supported by strong growth in construction activities and utilities.

(C) Tertiary Sector

- All economic activities involving service production, e.g., education, healthcare, banking, and communication.

- India's services sector grew by 7.2% in FY24, driven by public administration, defense, finance, insurance, and real estate.

- Experts later introduced two additional sectors: quaternary and quinary, which are considered sub-sectors of the tertiary sector.

(D) The Quaternary Sector

- Also known as the 'knowledge' sector.

- The activities related to education, research, and development fall under this sector.

- This sector plays a crucial role in determining the quality of human resources within an economy.

(E) Quinary Sector

- This sector encompasses all actions and decisions made at the highest levels.

- It includes top decision-makers in government, including their bureaucracy, and the private-corporate sector.

- The Quinary Sector involves a small number of individuals who are regarded as the "brains" behind the socio-economic performance of an economy.

Stages of Economic Growth (Rostow)

- W. W. Rostow proposed a theory in 1960 outlining five linear stages of economic growth through agriculture, industry, and services.

- Exceptions to the standard growth pattern exist, as seen in countries like India, Indonesia, Philippines, Thailand, and Vietnam.

- These countries transitioned from agrarian to service-based economies without substantial industrial sector growth.

- India's services sector has continued to grow robustly, with services exports surging by 21.3% between April and October 2024, reaching US$216 billion compared to US$192 billion in the same period in 2023

Economic Systems

- Human life relies on the consumption of goods and services.

- Essential items like food, water, shelter, and clothing are crucial for survival.

- The primary challenge for humanity is ensuring people have access to these necessities.

- This challenge involves two main aspects:

(i) Production of goods is necessary.

(ii) Distribution of goods to those in need is essential. - Setting up productive assets requires investment.

- The question of 'who' will invest and 'why' arises in this context.

- This challenge has led to the development of various economic systems.

- Various ways exist to organize an economy, leading to different economic systems.

- While numerous economic systems exist, three major ones stand out.

- Below is a brief overview of these major economic systems:

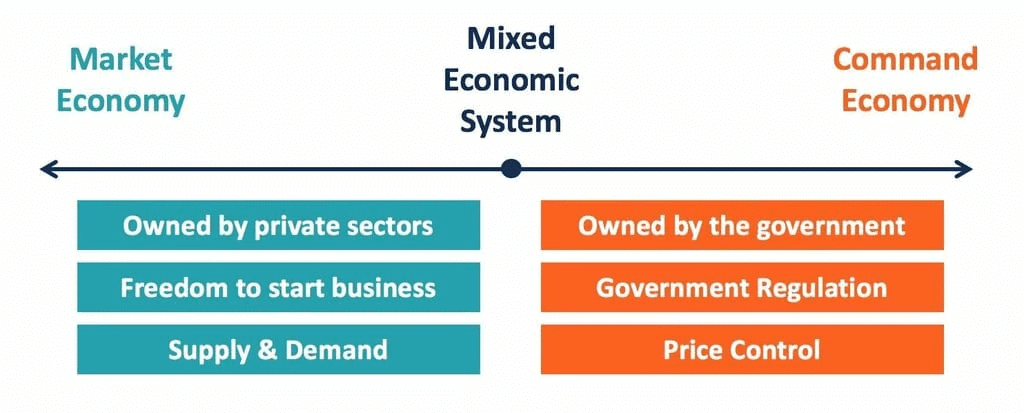

(A) Market Economy

- Emerged as the first formal economic system post traditional economies.

- Traced back to Adam Smith's work "An Inquiry into the Nature and Causes of the Wealth of Nations" in 1776.

- Self-interest as a motivator for economic activities leading to unintended social benefits, known as the "invisible hand".

- Division of labor for increased prosperity through specialization.

- Market determined by forces of demand and supply for the invisible hand to operate effectively.

- Regulation through market competition.

- Laissez-faire policy for efficient economic operation, emphasizing non-interference by the government.

- Driven by capitalism and free market economy, with subtle differences.

- Capitalism focuses on wealth creation and asset ownership, while a free market economy emphasizes wealth exchange.

- Capitalism may involve government regulations and potential monopolies, whereas a free market economy relies solely on market forces with minimal government intervention.

- Tested in the United States in the late 18th century, leading to its spread across Euro-America.

- Initial success followed by challenges like the Great Depression in 1929, widening inequality and necessitating some government intervention.

Cons of This System

- Supported by democratic rights and freedoms, the system fostered individual success, innovation, and business activities.

- Operational for over 150 years with subtle changes, the system had limitations, summarized as:

(i) Lack of support for those with lower purchasing power (i.e., the poor).

(ii) Minimal to no welfare actions by the state.

(iii) Continued economic inequality despite efforts like progressive taxation. - The existing policies failed to address economic recovery post-Depression.

- During the Depression, John Maynard Keynes introduced macroeconomics and proposed new policy approaches to aid economic recovery.

- Keynes recommended integrating traits from non-market economies to rectify the crisis, leading to the evolution of the mixed economic system.

(B) Non-Market (State) Economy

- Rooted in Karl Marx's ideas (1818-83), it had two variants: socialist and communist.

- Socialist model (e.g., USSR, 1917-89): state controlled natural resources.

- Communist model (e.g., China, 1949-85): state controlled labor and resources.

- It is also known as state economy, command economy, centrally planned economy and had following main beliefs:

(i) Country's resources for the well-being of all.

(ii) Resources best used under society's ownership (socialism/communism). State controls all economic roles.

(iii) No property rights to individuals to prevent exploitation and economic inequality.

(iv) Absence of market, competition, total state monopoly.

(v) People work in state-owned enterprises according to ability, receive state facilities based on needs.

(vi) State makes decisions on production, supply to people. - System first tested by Bolsheviks in ex-USSR (1919), spread to Eastern Europe and China

Cons of the System

- Scarcity of investible capital due to no wealth creation.

- Misallocation and wastage of resources due to state control.

- Absence of motivation for innovation and hard work.

- Lack of democratic rights, emergence of state capitalism.

- Internal decay since the 1970s, rejection of market socialism.

- Movement towards mixed economy by USSR (Perestroika, Glasnost, 1985-91) and China (Open Door Policy, 1978-present)

- Evolution towards mixed economy, borrowing traits from both systems.

- End of ideological divide, Cold War implications

Mixed Economy

- Mixed economic system emerged in the late 1930s with market economies adopting policies from non-market economies to recover from the Depression.

- France was the first country to officially adopt national planning in 1944-45, signaling the formal adoption of the mixed economic system.

- By the late 20th and early 21st centuries, the system was further solidified as non-market economies, including China and Vietnam, embraced market-oriented reforms.

- The World Bank recognized the necessity of state intervention in the economy, deviating from its previous stance in support of free market principles.

- Both market and non-market economic systems have shortcomings, leading to the idea that a blend of both is optimal, tailored to each country's socio-economic needs.

- Both state and private sectors have economic roles, with the private sector focusing on areas where profit motives are effective, like in the production of private goods.

- The state should manage roles that lack profit incentives for the private sector, such as providing public goods consumed by all without direct payments.

- Economic roles of both sectors can evolve as needed over time rather than staying fixed.

- Regulation of the economic system, including rules, competition, and taxation, is the responsibility of the state in a mixed economy.

- A mixed economic system is characterized by continuous adaptation to socio-economic needs, ensuring flexibility and responsiveness.

Distribution Systems

Three distribution systems evolved alongside the three economic systems.

(i) Capitalist Economy

- Goods and services distributed through the market based on market principles.

- People buy according to their needs at market prices.

(ii) State Economy

- Goods and services distributed directly by the state to people without payment.

(iii) Mixed Economy

- Hybrid distribution system combining state and market models.

- People buy certain goods from the market, while others are supplied by the state for free or at subsidized prices.

- Consensus favoring the mixed economic system.

- Evolution influenced by various ideologies with lasting impacts on global economies.

Global Policy Models and Consensus

Washington Consensus

Set of reform policies proposed by IMF, World Bank, and US Treasury and originated in Washington,

- Since all of these institutions were based in Washington, the policy prescription

was called the Washington Consensus by the US economist John Williamson,

- It consists of 10 reform policy points:

- Fiscal discipline

- Redirecting public expenditure to key fields

- Tax reform for lower rates and broader base

- Interest rate liberalization

- Competitive exchange rate

- Trade liberalization

- Liberalization of FDI inflows

- Privatization

- Deregulation to remove entry barriers

- Secure property rights

- Associated with neoliberalism, market fundamentalism, and globalization.

- Criticism for being too dogmatic and extreme in market reliance.

- Originally aimed at Latin America's issues.

- Later applied broadly but faced criticism, especially after the 2008 financial crisis, leading to increased advocacy for state intervention.

- It was viewed as imposing neoliberal policies on nations.

- Controversy over its implications and effects.

- Linked to liberalization, privatization, and globalization.

- Reduced state intervention in economies.

- Seen as influencing the 2008 subprime crisis and Great Recession.

- Shift towards favoring state intervention post-recession.

Beijing Consensus

- The Beijing Consensus emerged as a concept in 2004 by Joshua Cooper Remo.

- It represents the Chinese model of economic development initiated by Deng Xiaoping post-Mao Zedong's era in 1976.

- Seen as an alternative to the Washington Consensus, it consists of three main pillars:

(i) Constant experimentation and innovation

(ii) Peaceful distributive growth with gradual reforms

(iii) Self-determination and inclusion of selective foreign ideas - Received increased attention during the Western economic recession, contrasting it to the liberal market approach of the Washington Consensus.

- Controversy exists on whether other developing countries should adopt the Chinese model due to differing contexts and performance heterogeneity.

- Despite claims of the 'death of the market' and 'rise of state-led growth,' China's economic peak coincided with a dominant market presence.

- Interest in the model waned as China's economic slowdown, coupled with increasing global protectionism and concerns over debt-trap diplomacy, led to reevaluation of state-led growth strategies.

Santiago Consensus:

- Another alternative to the Washington Consensus.

- Proposed by James D. Wolfensohn, then President of the World Bank Group.

- Emphasizes inclusion, not just economic but social as well.

- Focuses on socio-economic development with local characteristics.

- Similar social aspects seen in the Beijing Consensus.

- Utilizes financial resources along with information technology and partnerships.

- Embraces openness and globalization for sharing global best practices in development.

- World Bank establishes a "knowledge bank" for this purpose.

- Inspires governments worldwide to prioritize inclusive socio-economic growth.

- Evident in India's third generation economic reforms in 2002, aimed at inclusive prosperity.

Capitalism as a Tool of Growth Promotion

- Capitalism initially failed post-Great Depression and evolved into a mixed economy.

- Resurgence of capitalism observed post-Washington Consensus and post-globalization (World Trade Organization).

- Experts link the 2007 Great Recession to extreme capitalistic tendencies in developed nations.

- World acknowledges capitalism as imperfect but beneficial for growth promotion.

- Countries globally adopt a pro-capitalistic stance within mixed economies for growth and welfare.

- India's shift towards a pro-corporate and pro-poor policy continues, with emphasis on production-linked incentive (PLI) schemes, digital public infrastructure, and welfare schemes such as PM Garib Kalyan Yojana in recent budgets.

- Capitalism viewed more as a growth and income promotion tool rather than a standalone economic system.

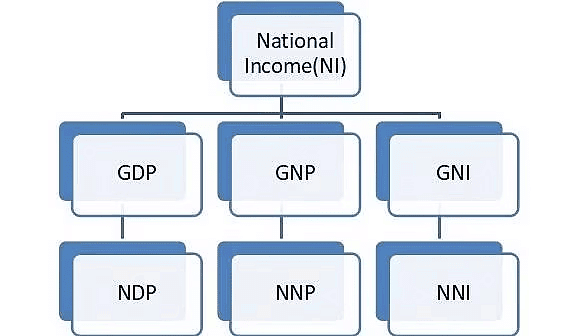

National Income: Concepts and Measures

- Measuring progress has been a major riddle for experts.

- Income as an indicator of progress was tried by many before the idea of the gross domestic product (GDP) was put forward by the US economist Simon Kuznets in 1934.

- The method tries to calculate (account) a country's income at domestic and national levels - in gross and net forms - having four clear concepts - GDP, NPL, GNP, and NNP.

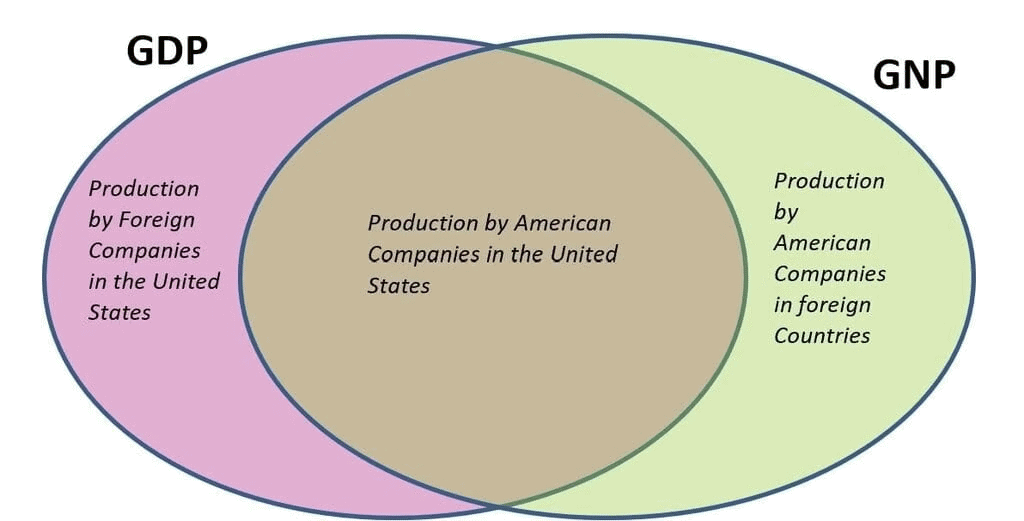

Gross Domestic Product (GDP)

- GDP is the total value of all final goods and services produced within a nation's boundaries during a one-year period.

- For India, the calendar year spans from 1 April to 31 March.

- By the expenditure approach: GDP = C + I + G + (X - M), where C = private consumption, I = gross investment, G = government spending, X = exports, M = imports.

- GDP is calculated by summing national private consumption, gross investment, government spending, and trade balance (exports minus imports).

- Subtracting imports not produced in the nation and adding exports of goods and services not sold domestically adjusts for transactions outside the country.

- 'Gross' equates to 'total' in economics, akin to 'domestic' referring to economic activities within a nation or country using its capital.

- 'Product' encompasses goods and services collectively, and 'final' denotes a product's end value without further potential additions.

- Annual percentage change in GDP signifies an economy's growth rate.

- GDP is a quantitative measure, reflecting the economy's internal strength by volume, but not its qualitative aspects.

- GDP serves as a widely-used metric for comparing global economies, with the IMF ranking nations based on GDP sizes.

- Since 1990, rankings have considered purchasing power parity (PPP), with India presently ranking as the world's fourth-largest economy at exchange rates and third-largest at PPP.

Net Domestic Product (NDP)

- NDP is GDP adjusted for depreciation, representing GDP minus the total value of depreciation incurred during the production of goods and services.

- Assets, except for human beings, undergo depreciation as they are used, necessitating the calculation of wear and tear.

- Governments set depreciation rates for assets, with different assets having varying rates based on factors like utility and longevity.

- In economies, depreciation is also observed in the external sector when the domestic currency devalues against foreign currencies.

- NDP = GDP - Depreciation, always indicating a lower value than GDP due to unavoidable depreciation.

- Techniques like ball bearings and lubricants aim to mitigate losses from depreciation.

- Different uses of the concept of NDP are as:

(i) NDP is primarily used domestically to analyze historical depreciation trends in the economy and specific sectors.

(ii) It highlights efforts in research and development to reduce depreciation levels over time. - NDP isn't ideal for cross-country comparisons due to varying depreciation rates set by different economies, sometimes lacking logical basis.

- Depreciation rates can be influenced by economic policy decisions, such as adjustments to stimulate sales or investment in specific sectors.

GROSS NATIONAL PRODUCT (GNP)

- GNP combines a country's GDP with its 'income from abroad', considering cross-border economic activities.

- Components of 'Income from Abroad' involve:

(i) Private Remittances: Net result of money transfers by Indian nationals working abroad and foreign nationals working in India.

(ii) Interest on External Loans: Net outcome of interest payments on money lent out and borrowed by the economy.

(iii) External Grants: Net balance of grants flowing to and from India. - In 2022, India was the top recipient of remittances globally, followed by Mexico and China according to the World Bank.

- India tends to have a negative balance in 'Income from Abroad' due to trade deficits and interest payments on foreign loans.

- Formula:

GNP = GDP - Income from Abroad, resulting in India's GNP always being lower than its GDP. - Uses of GNP are:

(i) Provides a more comprehensive view of national income than GDP, reflecting both quantitative and qualitative aspects of the economy.

(ii) Reveals insights into production behavior and patterns, dependency on foreign products, human resource standards, and financial interactions with other economies.

Net National Product (NNP)

- NNP of an economy is the GNP after deducting the loss due to 'depreciation'.

- Formula: NNP = GNP - Depreciation

or

NNP = GDP - Income from Abroad - Depreciation. - Different uses of NNP have been given as follows:

(i) This is the 'National Income' (NI) of an economy.

(ii) Per Capita Income: NNP divided by the total population gives the 'per capita income' (PCI) of a nation.

(iii) Depreciation Impact: Higher depreciation rates lead to lower PCI of a nation.

(iv) Rate of Depreciation: Different rates of depreciation impact the comparison of national incomes by international financial institutions. - The 'base year' and methodology for calculating national accounts were revised by the Central Statistics Office (CSO) in January 2015.

Cost and Price of National Income

Two sets of costs and prices need to be decided when calculating national income.

(A) Cost

- Income of an economy can be calculated at factor cost or market cost.

- Factor cost is the input cost incurred in production (e.g., cost of capital, raw materials, labor).

- Market cost is derived after adding indirect taxes to the factor cost.

- India switched to calculating national income at market price in January 2015.

- Market price is calculated by adding product taxes to the factor cost.

- Transition to market price calculation was facilitated by GST implementation.

(B) Price

- Income can be derived at constant and current prices.

- Constant price reflects inflation from a base year, while current price includes present-day inflation.

- Current price is akin to the maximum retail price (MRP) seen on goods in the market.

Revised Method

- The Central Statistics Office (CSO) released revised National Accounts data in January 2015.

- The base year transitioned from 2004-05 to 2011-12, following the National Statistical Commission's recommendation to update base years every 5 years.

- The revision aligns with the System of National Accounts (SNA), 2008 standards.

- Major Changes incorporated in this Revision are:

(i) Headline growth rate is now measured by GDP at constant market prices, referred to as "GDP" internationally.

(ii) Sector-wise estimates of Gross Value Added (GVA) will now be presented at basic prices rather than factor cost.

(iii) Comprehensive coverage of the corporate sector includes manufacturing and services, incorporating annual accounts from companies filed with the Ministry of Corporate Affairs (MCA).

(iv) The financial sector's coverage is enhanced by including information from stock brokers, stock exchanges, asset management companies, mutual funds, and regulatory bodies.

(v) Improved coverage of local bodies and autonomous entities, encompassing around 60% of grants/transfers provided to these institutions.

Comparing GVA and GDP

- GVA and GDP are calculated using two main methods - demand side and supply side.

- Under the supply side approach, GVA is determined by adding the value added by various sectors in the economy (e.g., agriculture, industry, and services).

- This method captures the income generated by all economic factors across the country.

- On the demand side, GDP is calculated by summing up all expenditures made within the economy.

- The four main sources of expenditures in an economy are:

(i) Private consumption

(ii) Government spending

(iii) Business investments, and

(iv) Net exports. - GDP includes all taxes collected and subsidies provided by the government. It equals GVA plus net taxes (taxes minus subsidies).

- While GDP is useful for comparative studies between economies, GVA is more suitable for comparing different sectors within the economy.

- GVA is particularly important for analyzing quarterly growth data as quarterly GDP is derived by allocating observed GVA data into different spending categories.

Fixed-Base To Chain-Base Method

- The Government is considering a shift from the fixed-base method to the chain-base method for GDP calculation.

- In the chain-base method, GDP estimates are compared with the previous year instead of a fixed base year, which is updated every year.

- Unlike the fixed-base method, the chain-base method adjusts weights annually to reflect structural changes in the economy.

- The current gig economy in India is said to be better reflected in the GDP statistics using the chain-base method.

- Advantages of the Chain-Base Method over the Fixed-Base Method involve:

(i) Allows for quicker capture of structural changes by incorporating new activities and items annually.

(ii) Facilitates easier and better comparison of India's growth data with other countries, aligning with international standards.

(iii) Aids in preventing controversies related to datasets.

Standing Committee On Economic Statistics(SCES)

- A committee established by the Government in late December 2019.

- Headed by ex-Chief Statistician Pronab Sen.

- Comprises 24 members from various organizations, including UNO, RBI, Ministry of Finance, Niti Aayog, Tata Trust, and economists/statisticians from universities.

- Tasked with examining economic datasets like the Periodic Labour Force Survey, Annual Surveys of Industries and Services Sectors, Time Use Survey, Economic Census, etc.

- Includes P. Chandrasekhar, H. Swaminathan, and J. Unni, among others.

- Signatories to a March 2019 Joint Statement criticizing data handling.

- Replaced existing Standing Committees on labor, industry, and services.

- Established due to India's non-compliance with the IMF's Special Data Dissemination Standard.

- Concerns raised by experts since early 2015 regarding economic datasets and their publication.

IMF's Special Data Dissemination Standard (SDDS)

- Launched in 1996 to enhance data transparency.

- Includes over 20 data categories such as national income accounts, production indices, employment, and central government operations.

- India's deviations from the SDDS:

(i) Delays in data dissemination as per prescribed periodicity.

(ii) Failure to list data category in the Advance Release Calendar (ARC).

(iii) Non-dissemination of data for a specific period. - IMF considers the deviations as "non-serious".

- Independent observers view the deviations as a result of indifference to data dissemination procedures

Income Estimates for 2024-25

(A) Real GDP: Estimated at ₹178.2 lakh crore, 6.4% growth (Economic Survey 2024-25).

(B) Nominal GDP: ~₹325 lakh crore (~$3.9 trillion), projected $4.2 trillion by 2025-26.

(C) GVA at Basic Prices: ~₹295 lakh crore, 6.6% growth (FY25).

(D) Net Taxes: ~₹30 lakh crore, up 12% from FY24.

(E) Per Capita Income: ~₹1,20,000 (constant prices), ₹2,10,000 (current prices, FY25).

Way Forward

- India faces global headwinds-geopolitical tensions and inflation around ~5% in 2024-requiring resilient policies.

- Policy priorities include agile fiscal and monetary policy, capital expenditure emphasis (capex), and reforms such as potential GST 2.0 to broaden base and simplify administration.

- Structural priorities include digital public infrastructure, green energy transition, strengthening human capital and self-reliance (Atmanirbhar Bharat) in critical sectors.

- Balancing growth, inclusion and macro-stability remains the central challenge for policymakers.

FAQs on Ramesh Singh Summary: Introduction to Economics- 1

| 1. What is scarcity and why does it matter in economics? |  |

| 2. How do microeconomics and macroeconomics differ in their approach to studying the economy? | |

| 3. What exactly is opportunity cost and how does it apply to real-life decisions? | |

| 4. Can you explain the difference between positive economics and normative economics with examples? | |

| 5. What are the basic economic problems and how do countries try to solve them? | |