Accounting for Share Capital (Part - 5)

Page No 8.126:

Question 80:

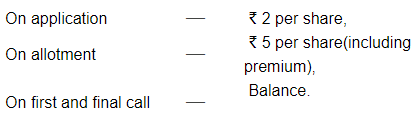

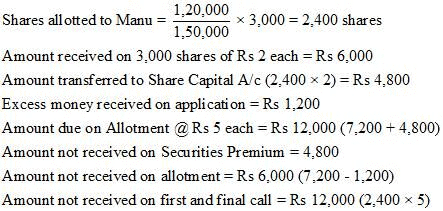

Jeevan Dhara Ltd. invited applications for issuing 1,20,000 equity shares of ₹10 each at a premium of ₹2 per share. The amount was payable as follows:

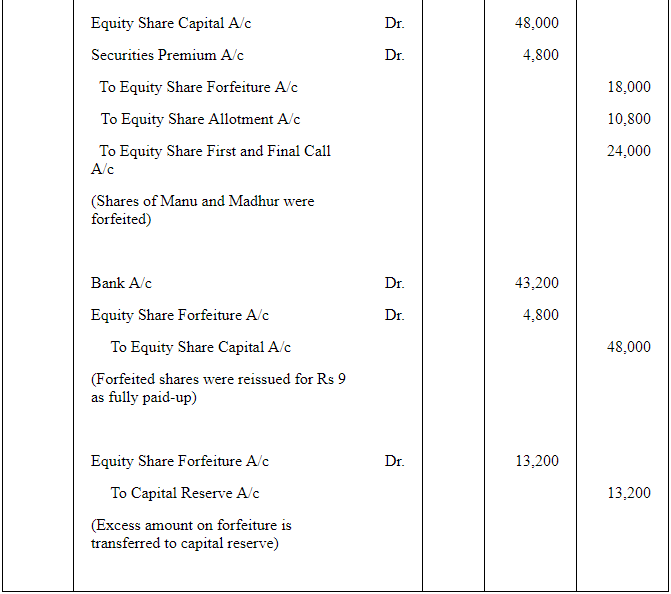

Applications for 1,50,000 shares were received . Shares were allotted to all the applicants on pro rata basis. Excess money received on applications was adjusted towards sums due on allotment . All calls were made. Manu who had applied for 3,000 shares failed to pay the amount due on allotment and first and final call Madhur who was allotted 2,400 shares failed to pay the first and final call . Shares of both Manu and Madhur were forfeited . The forfeited shares were reissued at ₹9 per share as fully paid-up.

Pass necessary journal entries for the above transactions in the books of Jeevan Dhara Ltd.

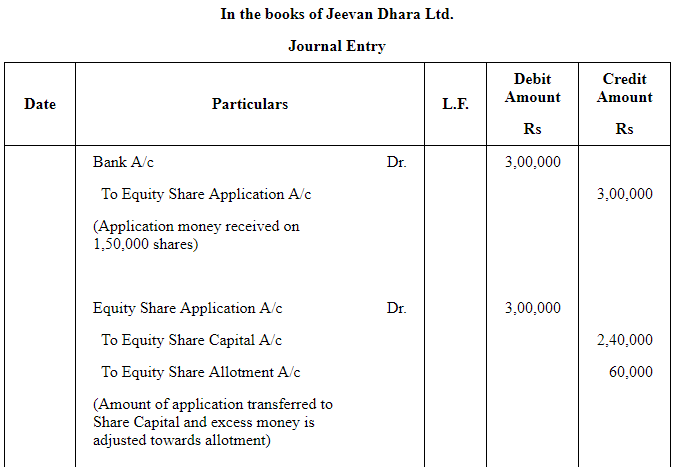

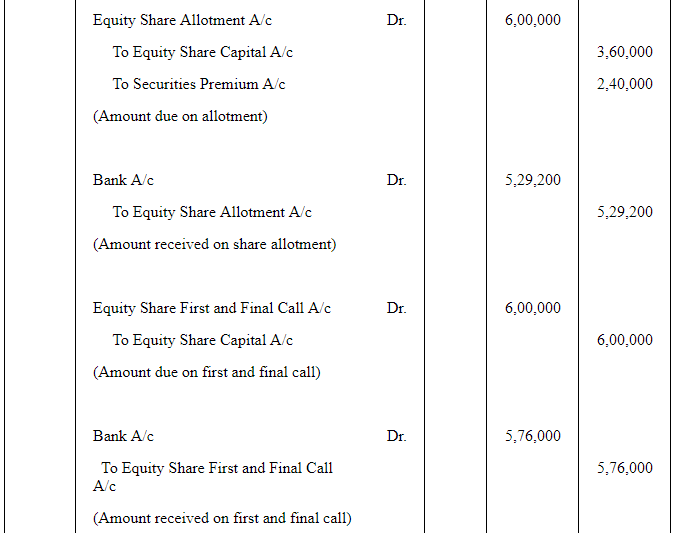

ANSWER:

Working Notes:

WN1: Calculation of Amount not received on Allotment and First and Final Call

WN2: Calculation of amount not received from Madhur

Question 81:

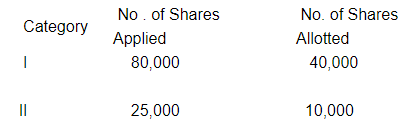

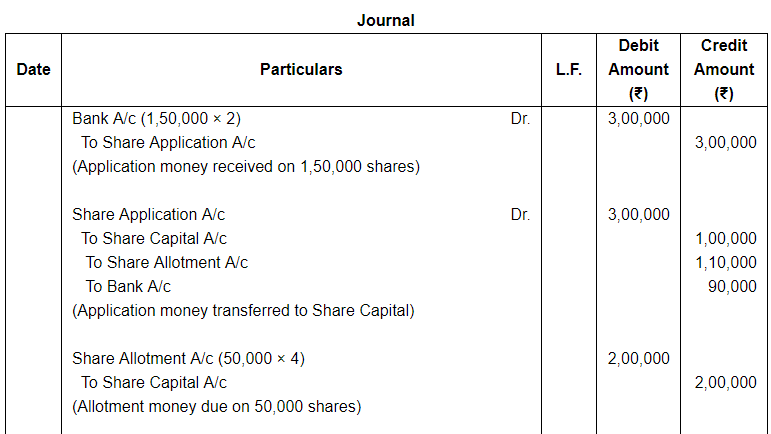

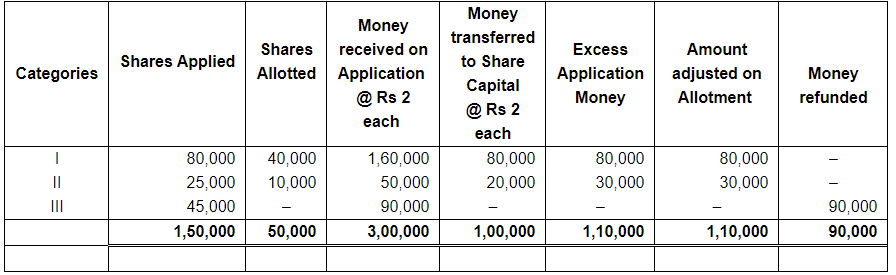

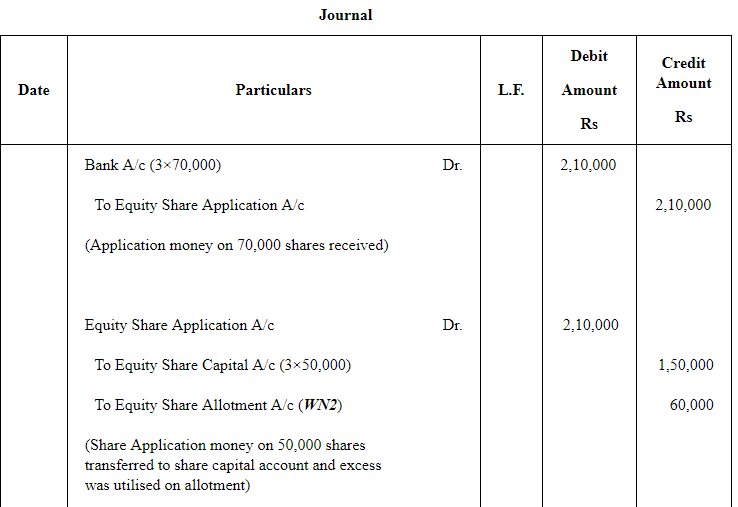

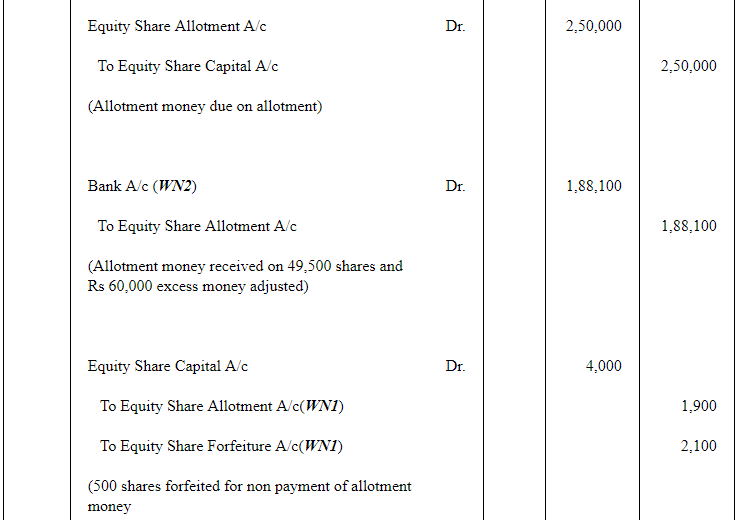

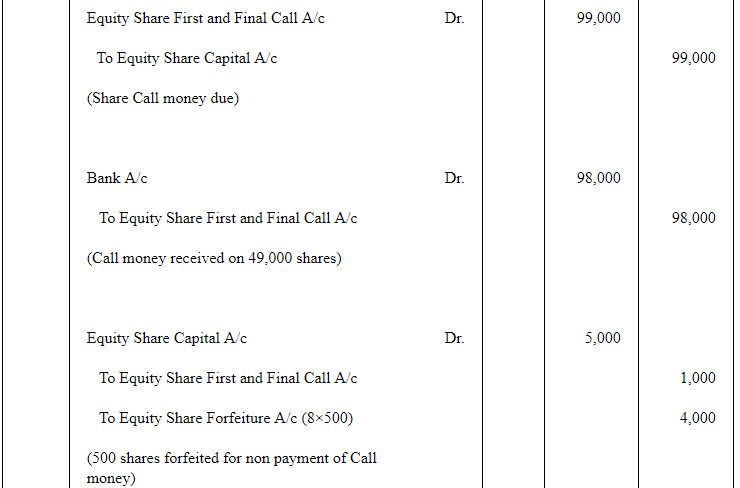

JJK Ltd. invited applications for issuing 50,000 equity shares of ₹10 each at par. The amount was payable as follows:

| On Application | -- | ₹2 per share, |

| On Allotment | -- | ₹4 per share; and |

| On First and Final call | -- | Balance Amount. |

The issue was oversubscribed three times. Applications for 30% shares were rejected and money refunded. Allotment was made to the remaining applicants as follows:

Excess money paid by the applicants who were allotted shares was adjusted towards sums due on allotment.

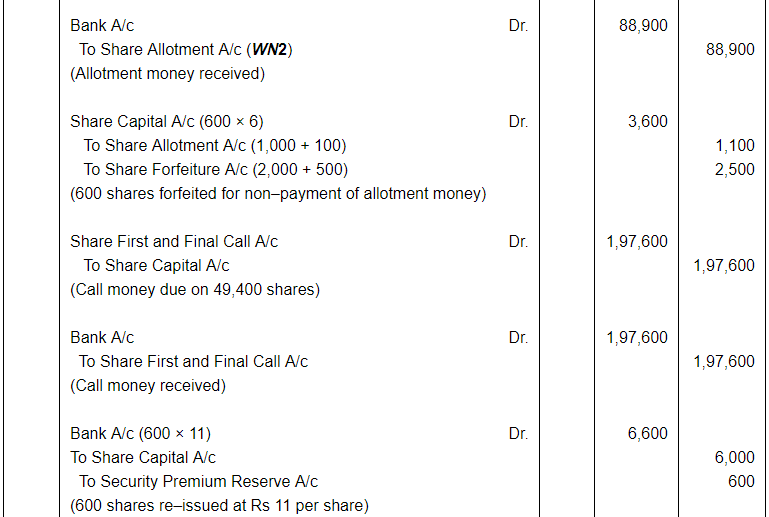

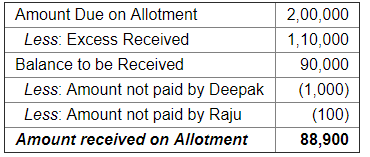

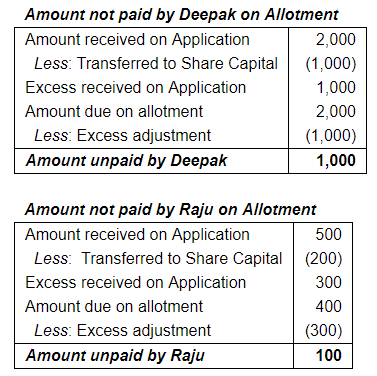

Deepak, a shareholder belonging to Category I , who had applied for 1,000 shares ,failed to pay the allotment money. Raju, a shareholder holding 100 shares, also failed to pay the allotment money. Raju belonged to Category II. Shares of both Deepak and Raju were forfeited immediately after allotment . Afterwards, first and final call was made and was duly received . The forfeited shares of Deepak and Raju were reissued at ₹11 per share fully paid-up.

Pass necessary journal entries for the above transactions in the books of company.

ANSWER:

Working Notes:

WN1:Computation Table

WN2:Calculation of Amount Received on Allotment

WN3: Calculation of Shares Applied/Allotted

Question 82:

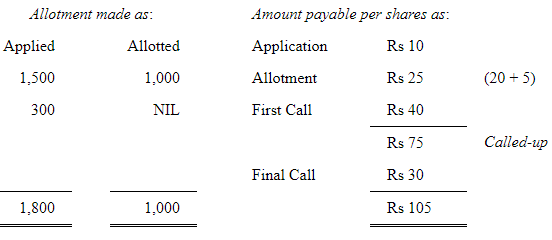

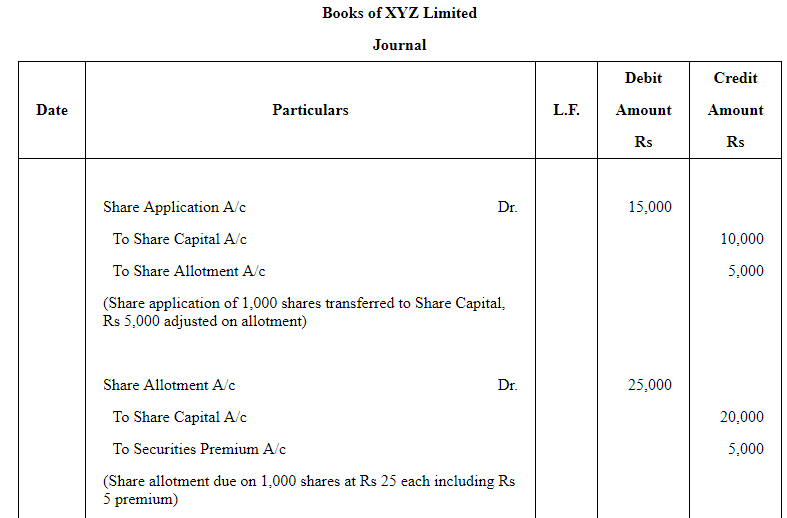

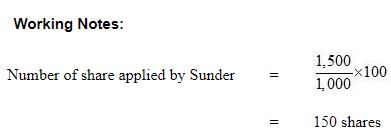

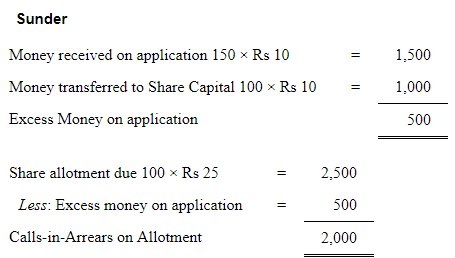

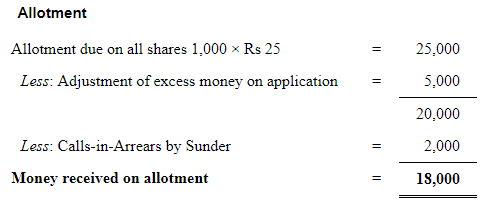

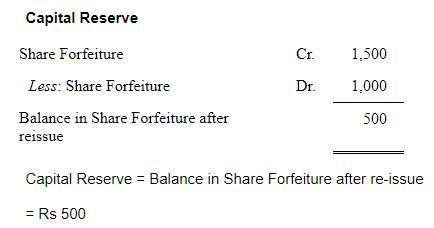

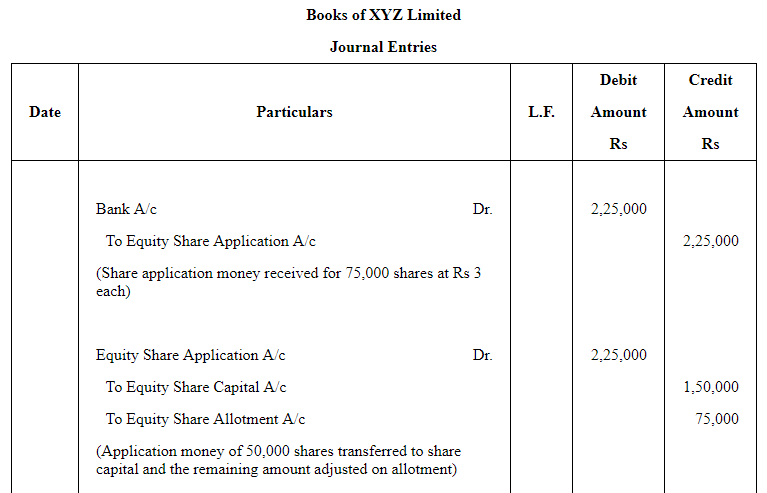

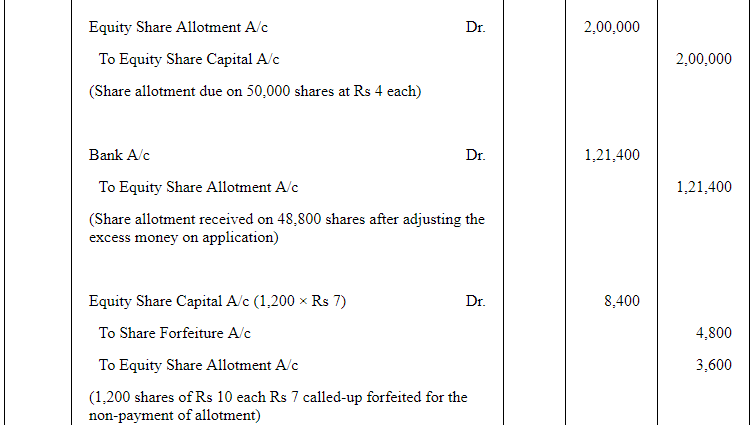

XYZ Ltd . is registered with an authorised capital of ₹2,00,000 divided into 2,000 shares of ₹100 each of which, 1,000 shares were offered for public subscription at a premium of ₹5 per share , payable as:

On application -- ₹10 per share,

On allotment -- ₹25 per share (including premium),

first call -- ₹40 per share

On final call -- ₹30 per share

Applications were received for 1,800 shares, of which applications for 300 shares were rejected outright; the rest of the application were allotted 1,000 shares on pro rata basis. Excess application money was transferred to allotment.

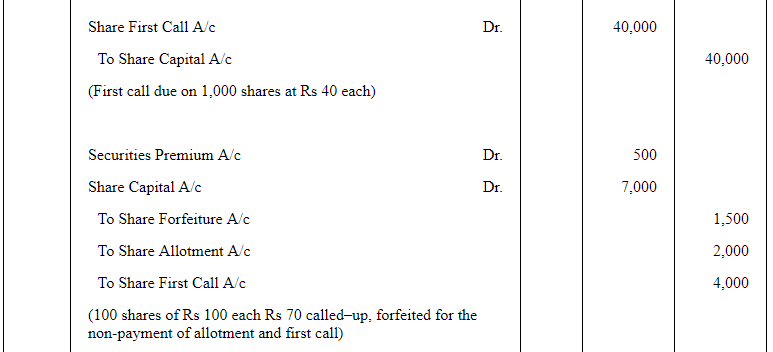

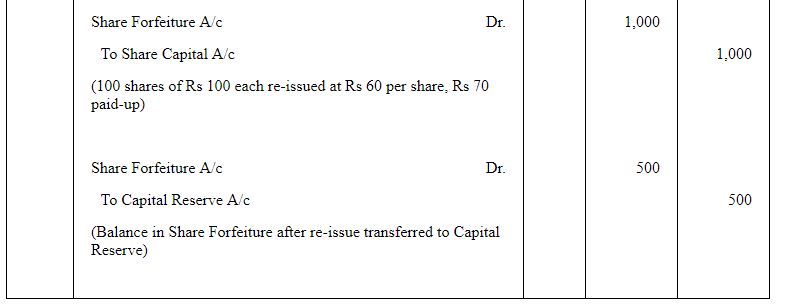

All the money was duly received except from Sundar, holder of 100 shares, who failed to pay allotment and first call money. His shares were later forfeited and reissued to Shyam at ₹60 per share ₹70 paid-up. Final call has not been made.

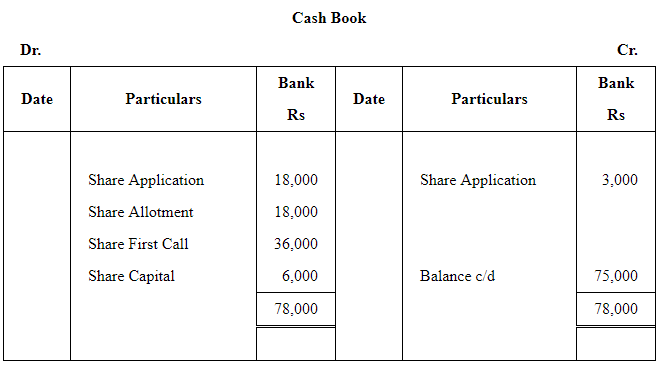

Pass necessary Journal entries and prepare Cash Book in the books of XYZ Limited.

ANSWER:

Authorised capital 2,000 shares of Rs 100 each.

Issued 1,000 shares of Rs 100 each at premium of Rs 5

Applied 1,800 shares

Page No 8.127:

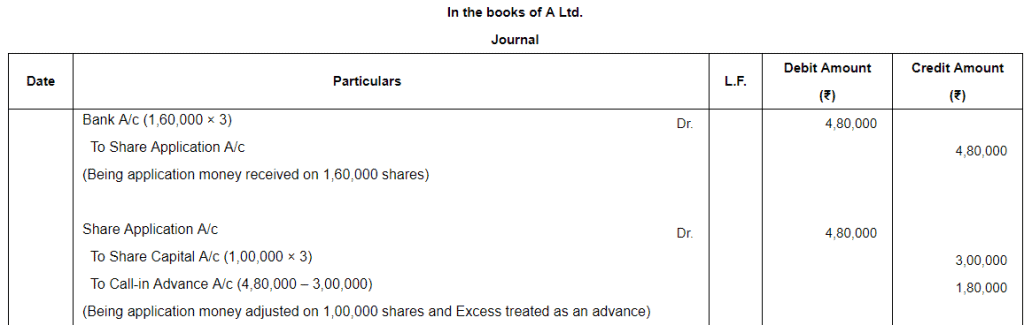

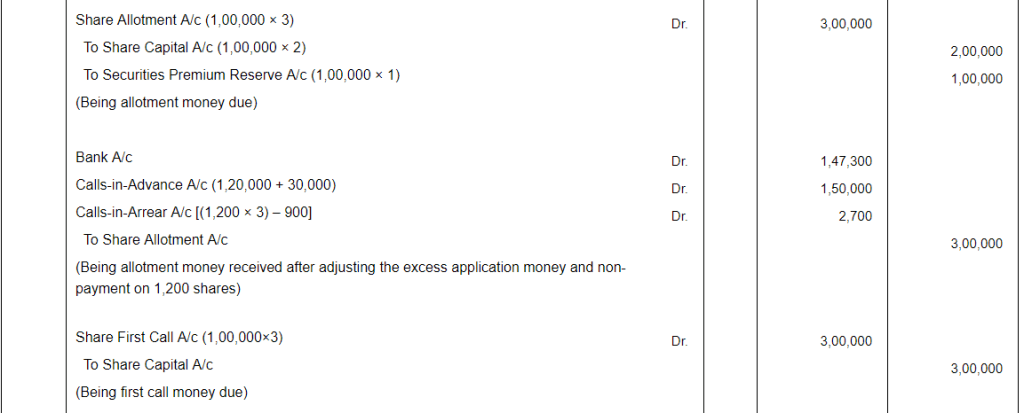

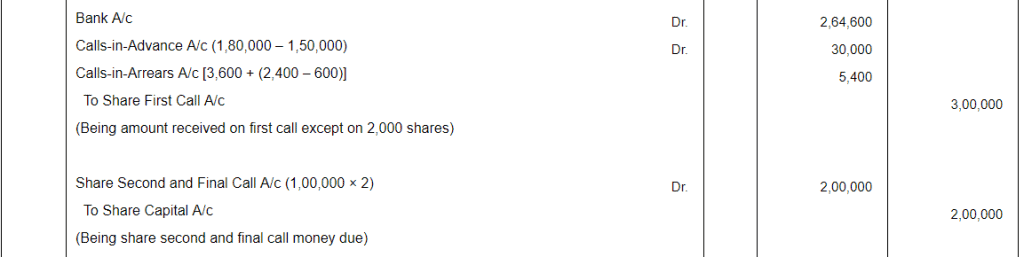

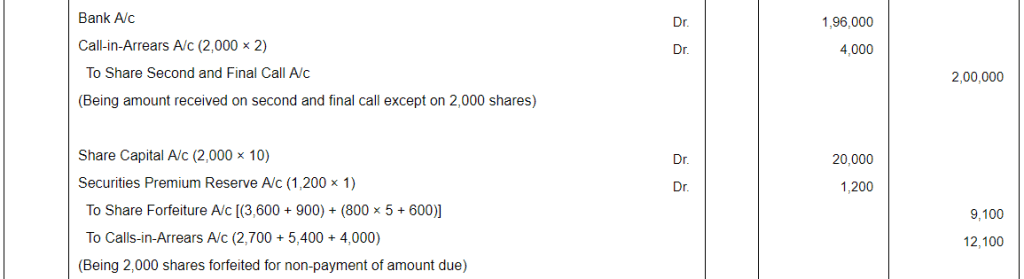

Question 83:

A Ltd. invited applications for issuing 1,00,000 shares of ₹10 each at a premium of ₹1 per share. The amount was payable as follows:

On Application - 3 per share;

On Allotment - 3 per share (including premium);

On First Call - 3 per share;

On Second and Final Call - Balance amount.

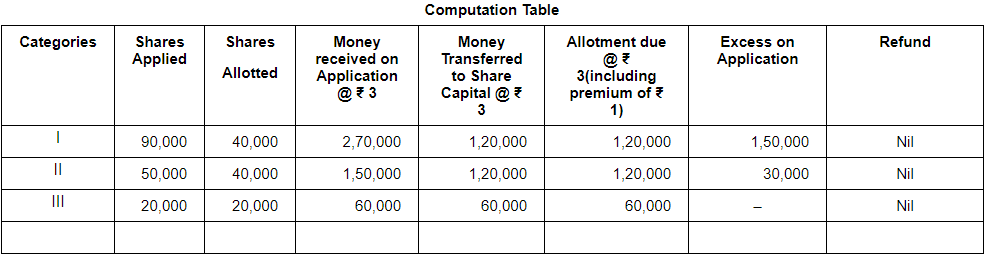

Applications for 1,60,000 shares were received. Allotment was made on the following basis:

(i) To applicants for 90,000 shares - 40,000 shares;

(ii) To applicants for 50,000 shares - 40,000 shares;

(iii) To applicants for 20,000 shares - Full shares.

Excess money paid on application is to be adjusted against the amount due on allotment and calls.

Rishabh, a shareholder, who applied for 1,500 shares and belonged to category (ii), did not pay allotment, first and second and final call money.

Another shareholder, Sudha, who applied for 1,800 shares and belonged to category (i), did not pay the first and second and final call money.

All the shares of Rishabh and Sudha were forfeited and were subsequently reissued at ₹7 per share fully paid.

Pass the necessary Journal entries in the books of A Ltd. Open Calls-in-Arrears Account and Calls-in-Advance Account wherever required.

ANSWER:

Working Notes:

Question 84:

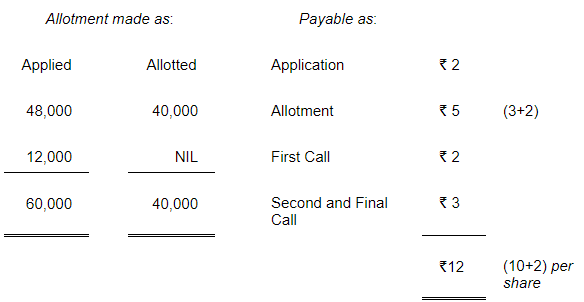

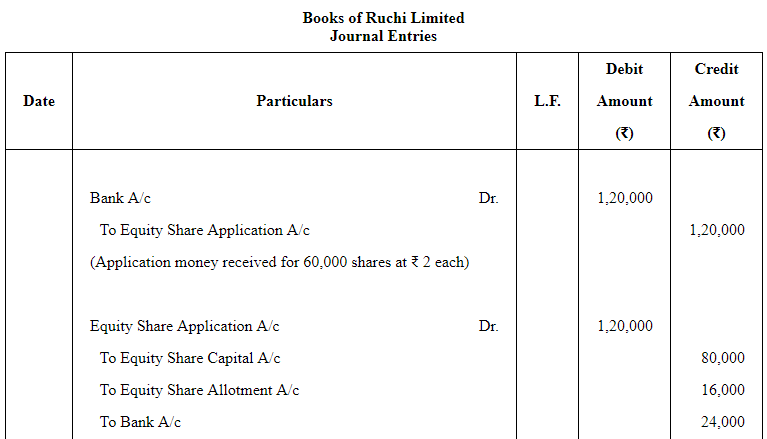

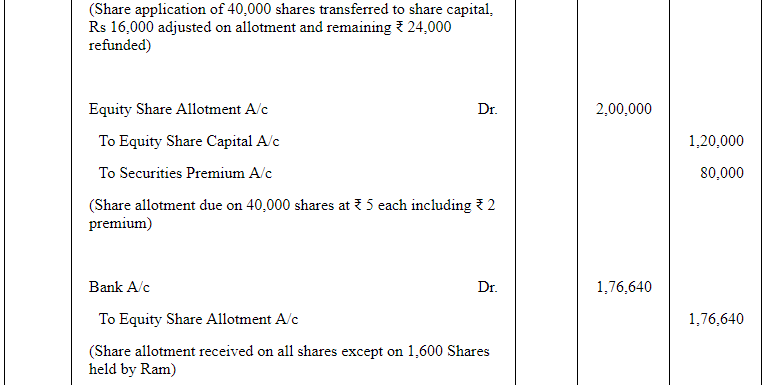

Ruchi Ltd. issued for public subscription 40,000 Equity Shares of ₹10 each at a premium of ₹2 per share payable as:

On application -- ₹2 per share;

On allotment -- ₹5 per share (including premium),

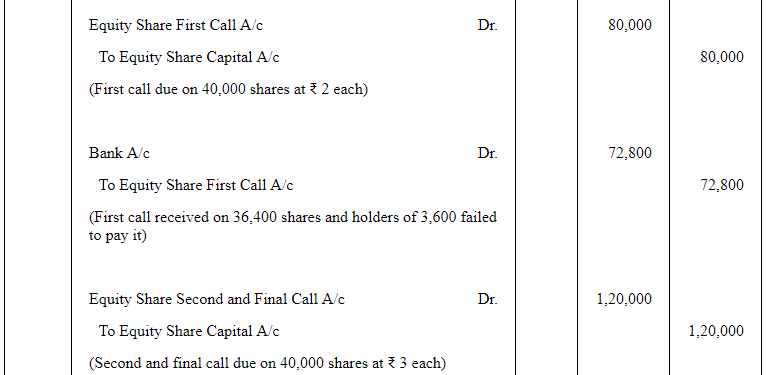

On first call -- ₹2 per share,

On second and final call -- ₹3 per share.

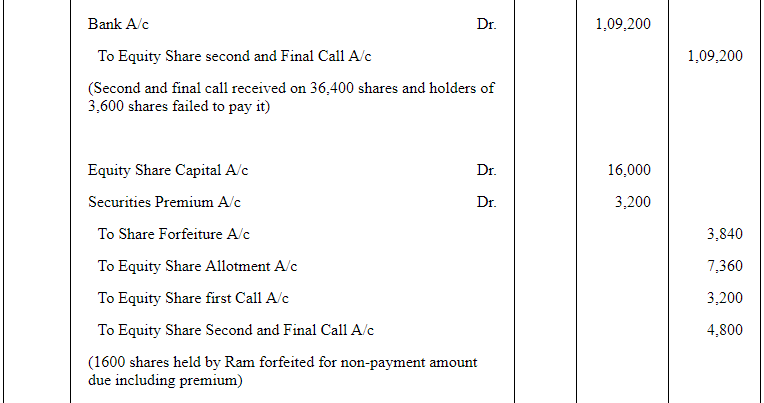

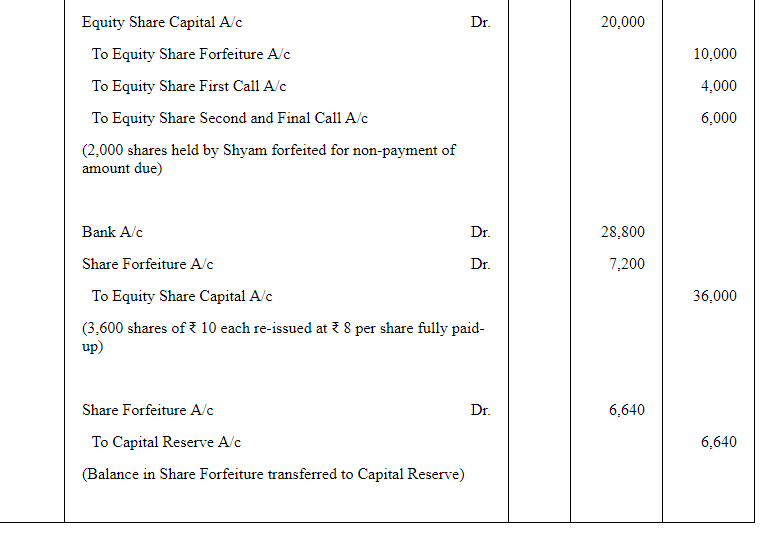

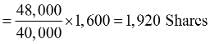

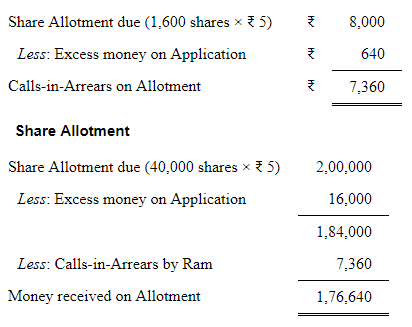

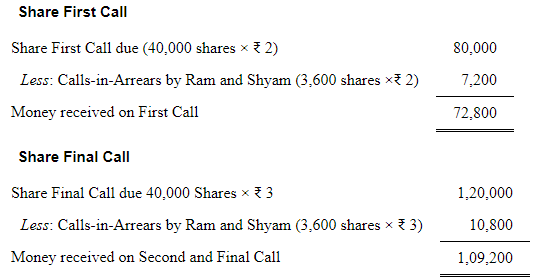

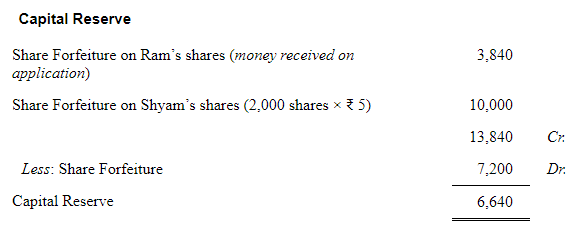

Applications were received for 60,000 shares. Allotment was made on pro rata basis to the applicants for 48,000 shares, the remaining applications being refused. Money overpaid on application was utilised towards sums due on allotment. Ram to whom 1,600 shares were allotted failed to pay the allotment money and Shyam to whom 2,000 shares were allotted failed to pay the two calls. These shares were subsequently forfeited after the second and final call was made. All the forfeited shares were reissued as fully paid-up @ ₹8 per share.

Give necessary Journal entries for the above transactions.

ANSWER:

Issued capital 40,000 shares of ₹10 each at premium of ₹2

Applied ₹60,000 shares

Working Notes:

Working Notes:

Ram's shares

Number of shares applied by Ram

Page No 8.128:

Question 85:

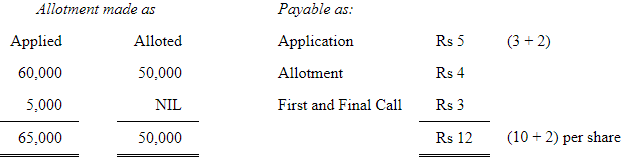

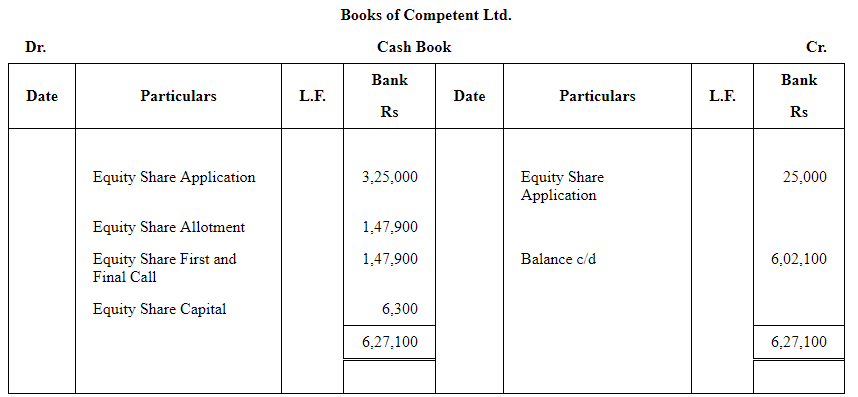

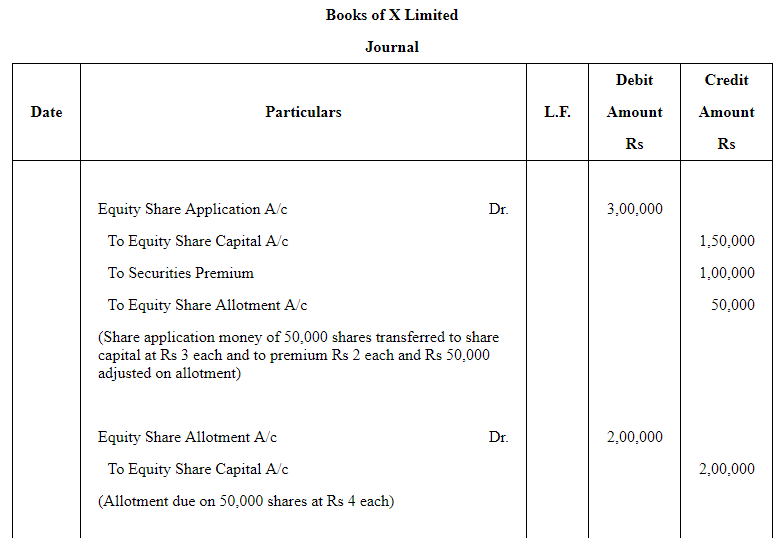

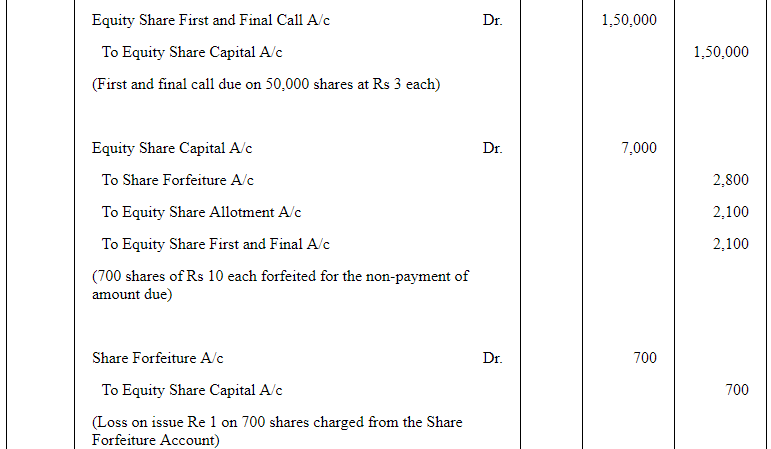

Competent Ltd. issued a prospectus inviting applications for 50,000 Equity Shares of ₹10 each, payable ₹5 as per application (including ₹2 as premium), ₹4 as per allotment and the balance towards first and final call.

Applications were received for 65,000 shares. Application money received on 5,000 shares was refunded with letter of regret and allotments were made on pro rata basis to the applicants of 60,000 shares. Money overpaid on applications including premium was adjusted on account of sums due on allotment.

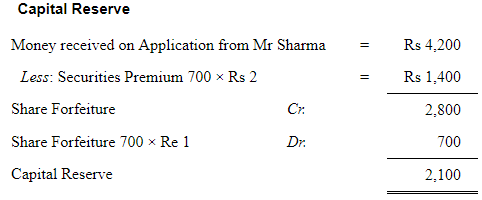

Mr. Sharma to whom 700 shares were allotted failed to pay the allotment money and his shares were forfeited by the Directors on his subsequently failure to pay the call money.

All the forfeited shares were subsequently sold to Mr. Jain credited as fully paid-up for ₹9 per share.

You are required to set out the Journal entries and the relevant entries in the Cash Book.

ANSWER:

Issued shares 50,000 of Rs 10 each at a premium of Rs 2

Applied share 65,000

Working Notes-

Mr. Sharma's Share

Number of shares applied by Mr Sharma

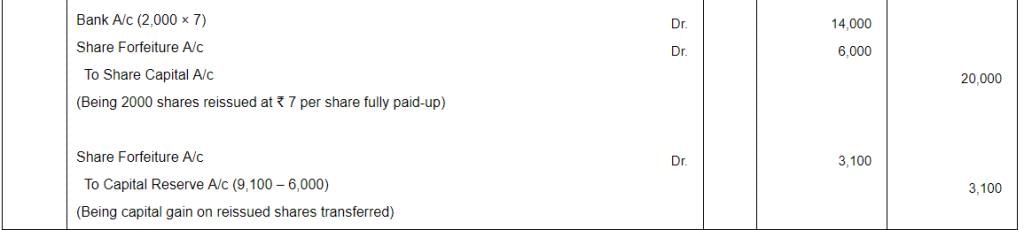

Question 86:

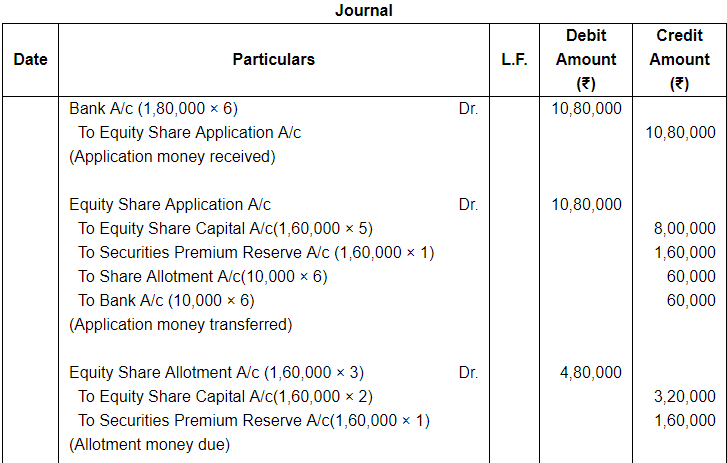

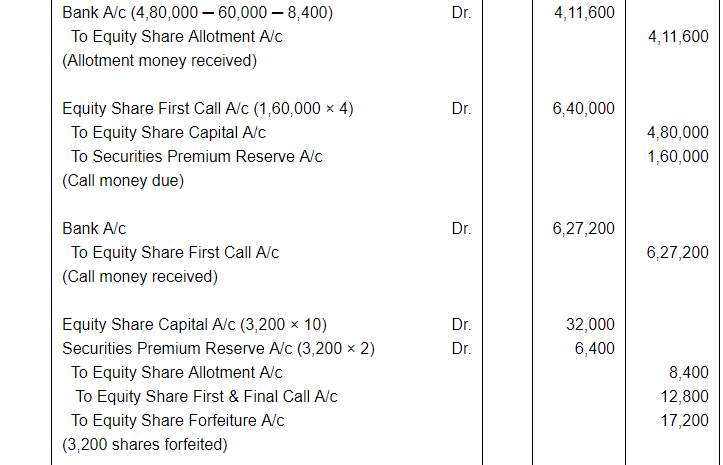

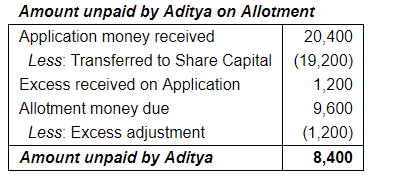

Nitro Paints Ltd. invited applications for issuing 1,60,000 equity shares of ₹10 each at a premium of ₹3 per share. The amount was payable as follows:

On application -- ₹6 per share(including premium ₹1);

On allotment -- ₹3 per share(including premium ₹1); and

The balance -- on First and Final call.

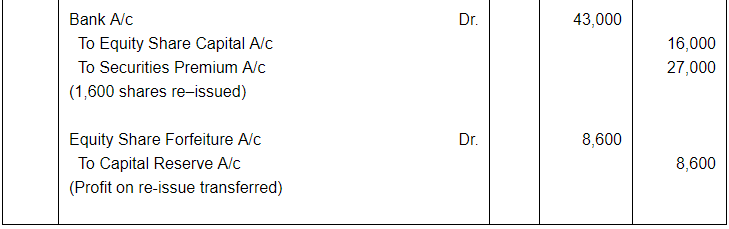

Applications for 1,80,000 shares were received .Applications for 10,000 shares were rejected and pro rata allotment was made to the remaining applicants.Over payment received on application was adjusted towards sums due on allotment . All calls were made and were duly received except allotment and final call from Aditya who was allotted 3,200 shares. His shares were forfeited . Half of the forfeited shares were reissued for ₹43,000 as fully paid-up.

Pass necessary journal entries for the above transactions in the books of Nitro Paints Ltd.

ANSWER:

Question 87:

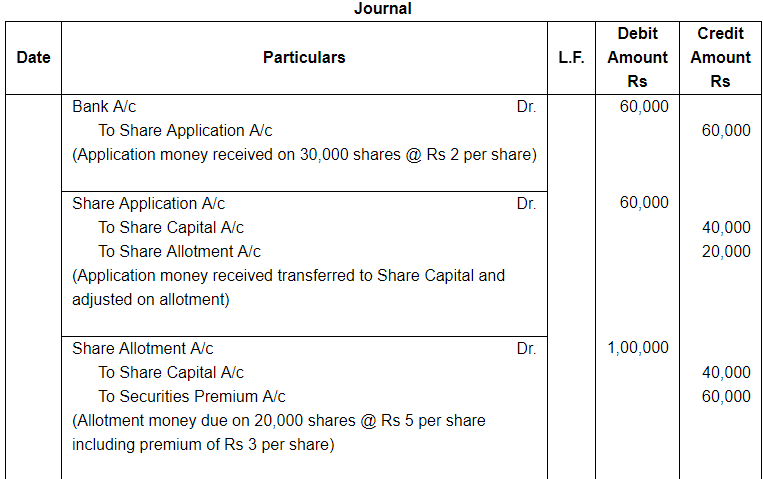

Raja Ltd. invited applications for issuing 50,000 Equity Shares of ₹10 each . The amount was payable as follows:

On application -- ₹3 per share,

On allotment -- ₹5 per share,

On first and final call -- Balance.

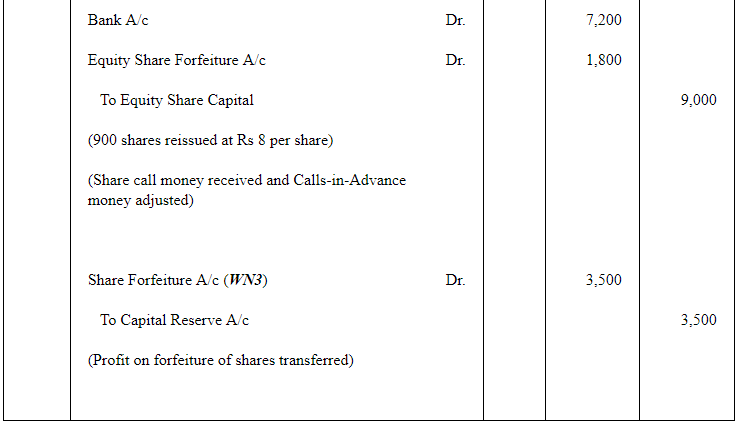

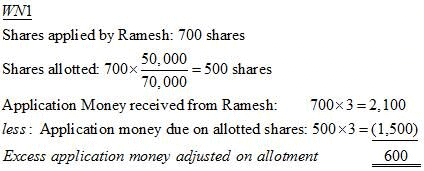

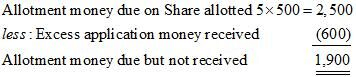

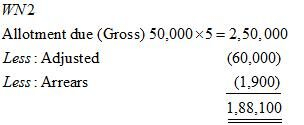

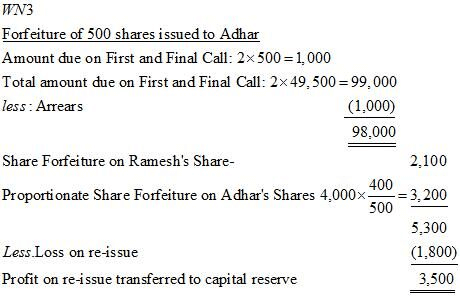

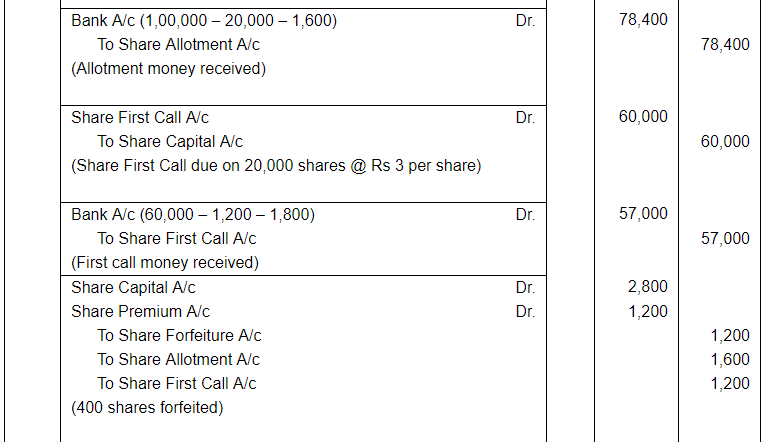

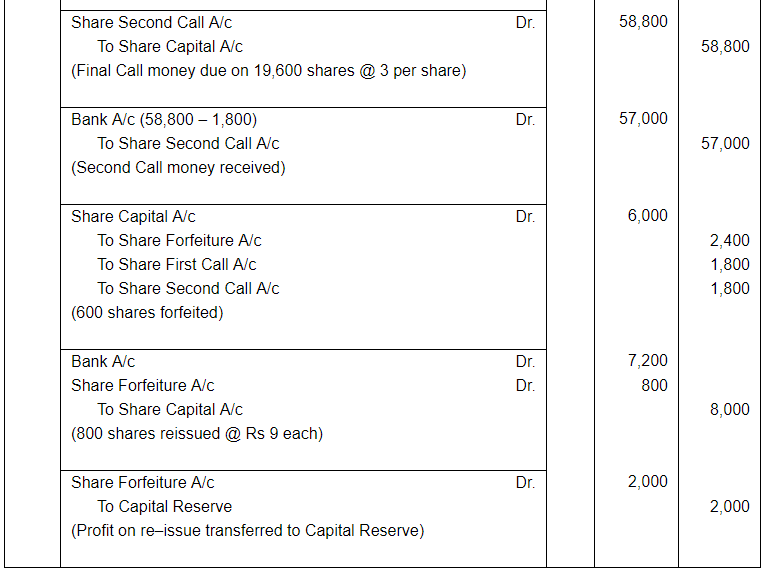

Applications for 70,000 shares were received . Allotment was made to all applicants on pro rata basis. Excess money received on application was adjusted towards sums due on allotment . Ramesh, who had applied for 700 shares , did not pay the allotment money and on his failure to pay the allotment money his shares were forfeited. Afterwards , the first and the final call was made . Adhar, who had been allotted 500 shares, did not pay the first and final call . His shares were also forfeited . Out of the forfeited shares 900 shares were reissued at ₹8 per share as fully paid-up . The reissued shares included all the shares of Ramesh.

Pass necessary journal entries for the above transactions in the books of the company.

ANSWER:

Working Note:

Question 88:

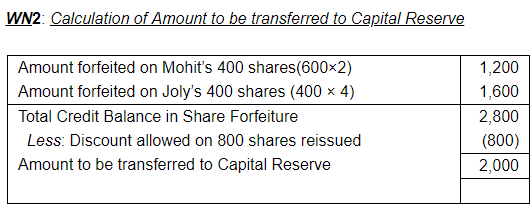

Prince Limited issued a prospectus inviting applications for 20,000 equity shares of ₹10 each at a premium of ₹3 per share payable as follows:

With application -- 2,

On allotment (including premium) -- ₹5,

On first call -- ₹3,

On second call -- ₹3.

Applications were received for 30,000 shares and allotment was made on pro rata basis. Money overpaid on application s was adjusted to the amount due on allotment.

Mr Mohit whom 400 shares were allotted , failed to pay the allotment money and the first call , and his shares were forfeited after the first call . Mr Joly, whom 600 shares were allotted , failed to pay for the two calls and hence, his shares were forfeited .

Of the shares forfeited, 800 shares were reissued to Supriya as fully paid for ₹9 per share, the whole of Mr Mohit's shares being included.

ANSWER:

Page No 8.129:

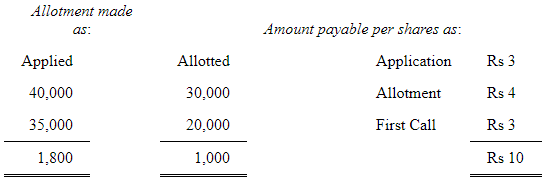

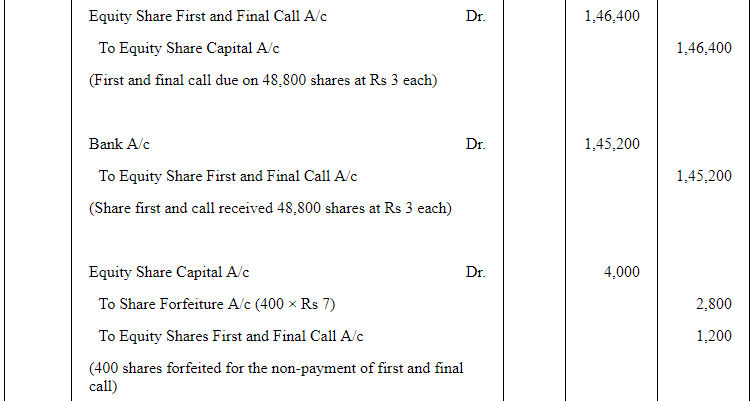

Question 89:

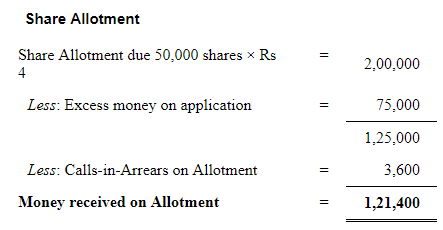

XYZ Ltd. invited applications for issuing 50,000 Equity Shares of ₹10 each . The amount was payable as:

On application -- ₹3 per share,

On allotment -- ₹4 per share,

On first and final call -- ₹3 per share.

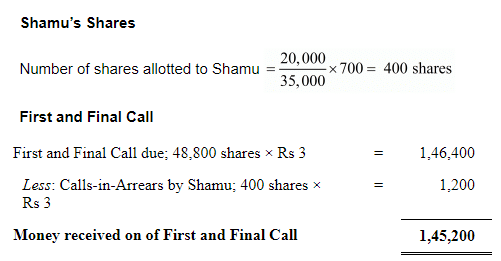

Applications were received for 75,000 shares and pro rata allotment was made as:

Applicants for 40,000 shares were allotted 30,000 shares on pro rata basis.

Applicants for 35,000 shares were allotted 30,000 shares on pro rata basis.

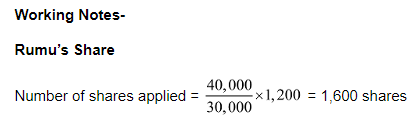

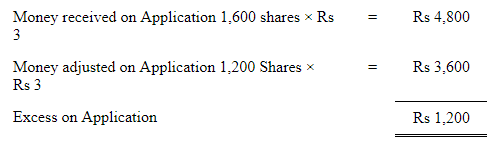

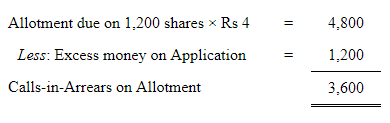

Ramu, to whom 1,200 shares were allotted out of the group applying for 40,000 shares, failed to pay the allotment money. His shares were forfeited immediately after allotment.

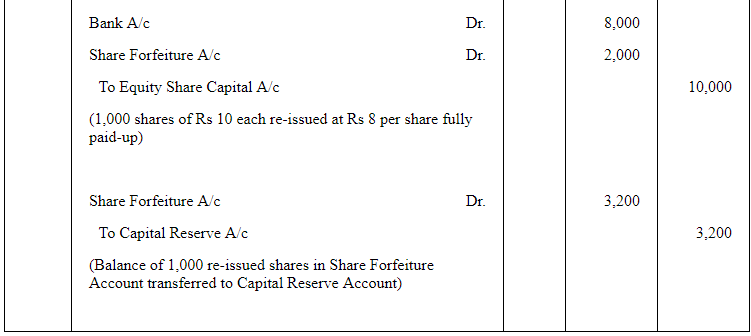

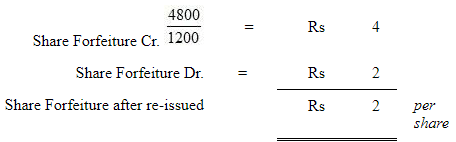

Shamu, who had applied for 700 shares out of the group applying for 35,000 shares, failed to pay the first and final call . His shares were also forfeited. Out of the forfeited shares, 1,000 shares were reissued @ Applicants for 40,000 shares were allotted 30,000 shares on pro rata basis. 8 per share as fully paid-up. The reissued shares included all the forfeited shares of Shamu.

Pass necessary Journal entries to record the above transactions.

ANSWER:

Issued 1,000 equity shares of Rs 10 each

Applied 1,800 shares

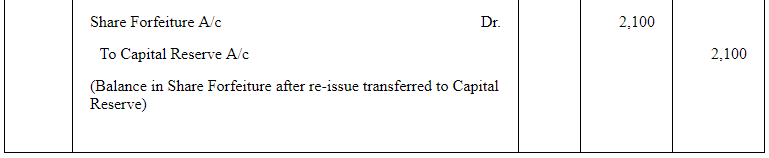

Capital Reserve

Shares re-issued out the shares forfeited from Ramu = 1,000 shares - Shamu's shares= 1,000 - 400 = 600 shares

on re-isssue Ramu's shares:

Capital Reverse on re-issue of 600 shares forfeited from Ramu

Capital Reserve after re-issue of 600 shares = Share Forfeiture after re-issue (per share) × 600 shares = Rs 2 × 600 = Rs 1,200

on re-isssue Shamu's shares:

Capital Reserve after re-issue of 400 shares = Share Forfeiture after re-issue (per share) × 600 shares

= Rs 5 × 400 = Rs 2,000

Total amount of Capital Reserve = Capital Reserve of 600 shares + Capital Reserve of 400 shares

Page No 8.129:

Question 90:

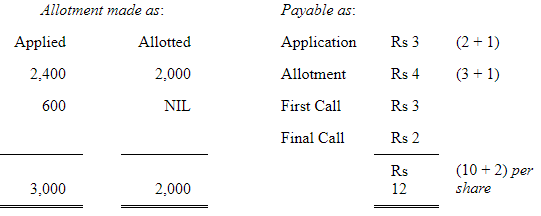

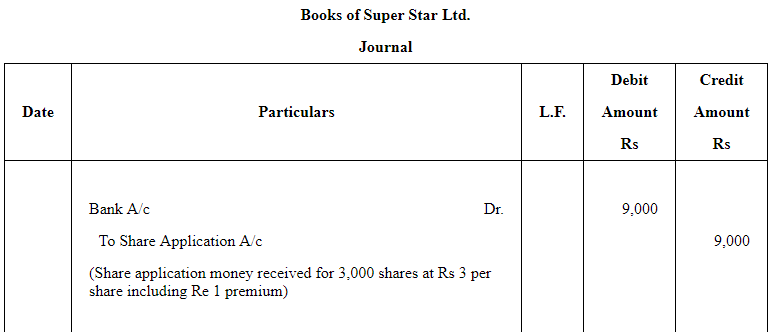

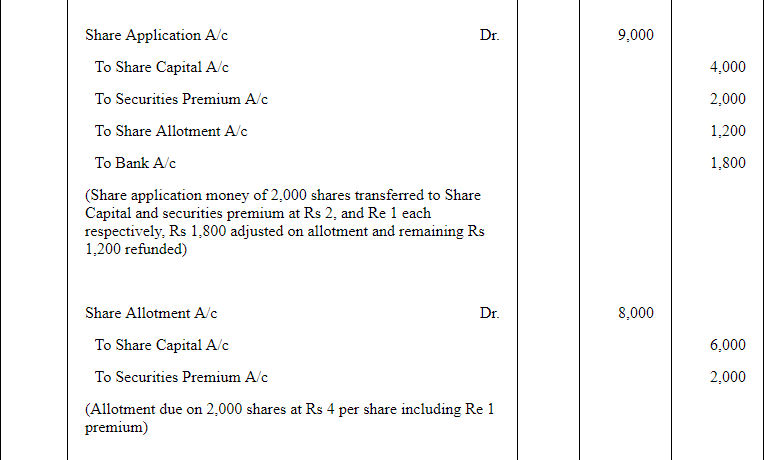

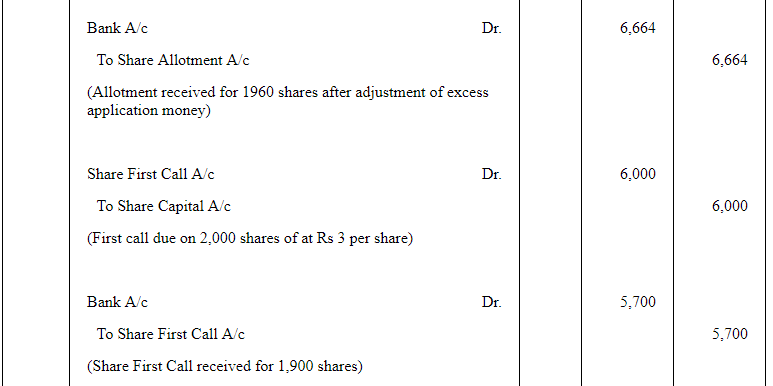

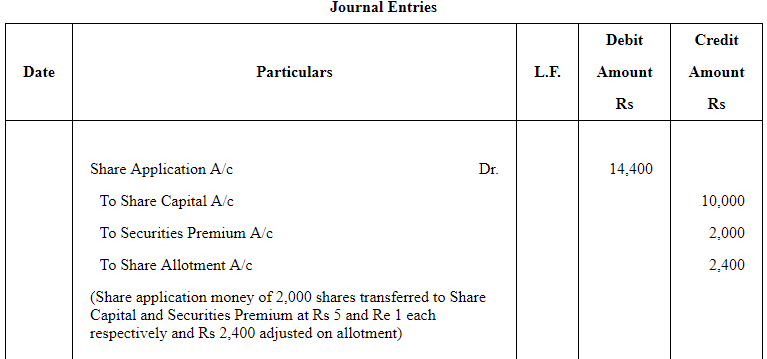

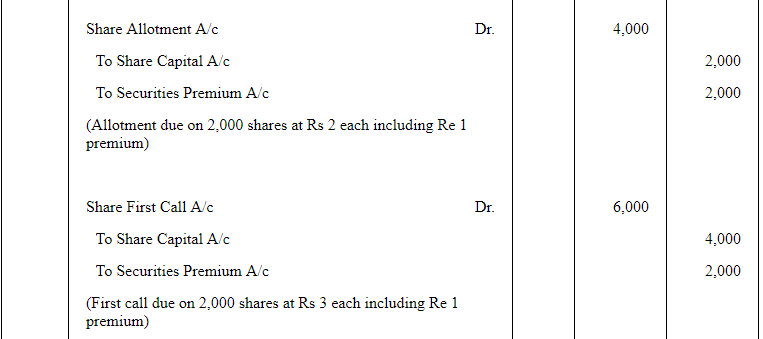

Super Star Ltd. issued a prospectus inviting applications for 2,000 shares of ₹ 10 each at a premium of ₹ 2 per share , payable as:

On application -- ₹3 per share (including ₹ 1 premium),

On allotment -- ₹ 4 per share (including ₹ 1 premium),

On first call -- ₹ 3 per share

On second and final call -- ₹ 2 per share.

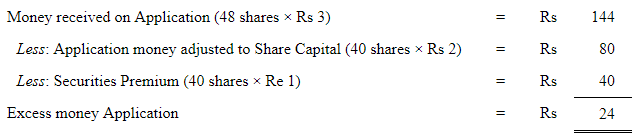

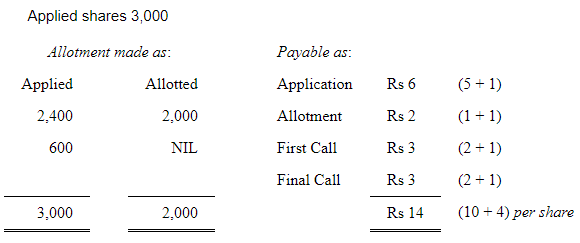

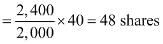

Applications were received for 3,000 shares and pro rata allotment was made on the applications for 2,400 shares . It was decided to utilise excess application money towards the amount due on allotment.

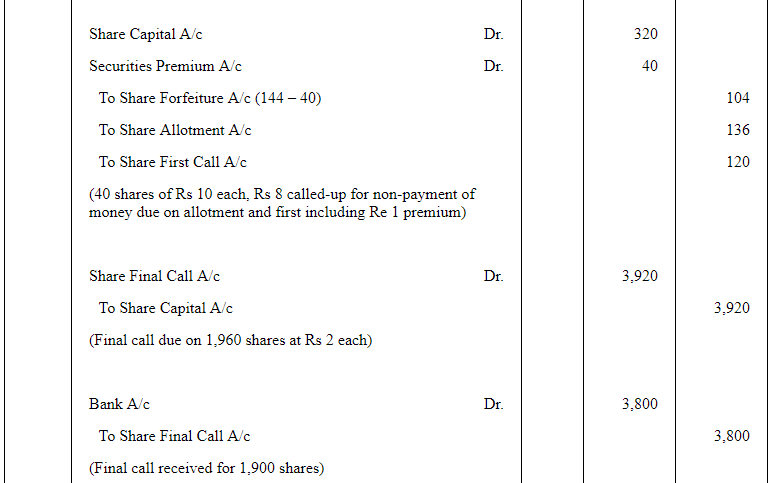

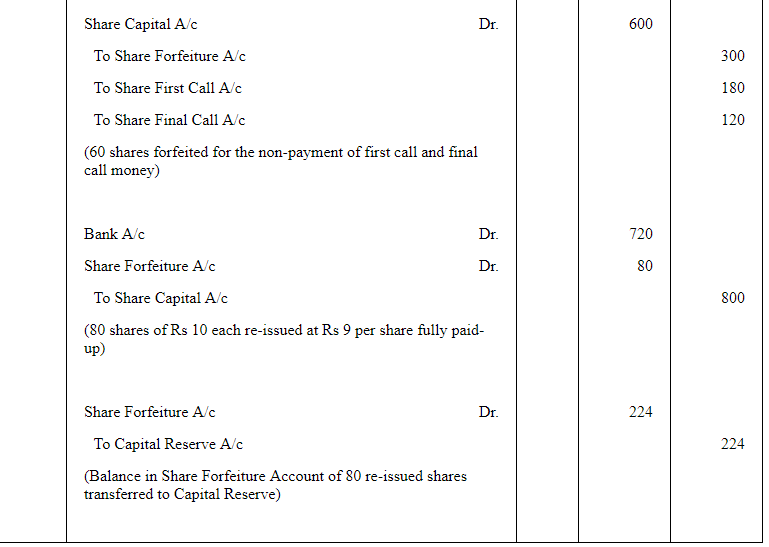

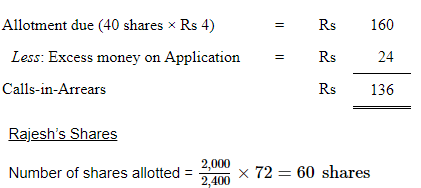

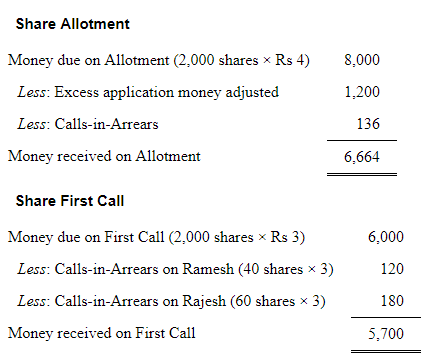

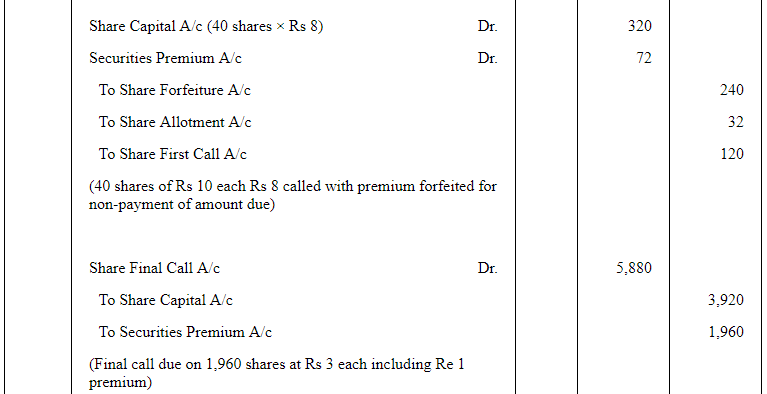

Ramesh, to whom 40 shares were allotted , failed to pay the allotment money and on his subsequent failure to pay the first call, his shares were forfeited.

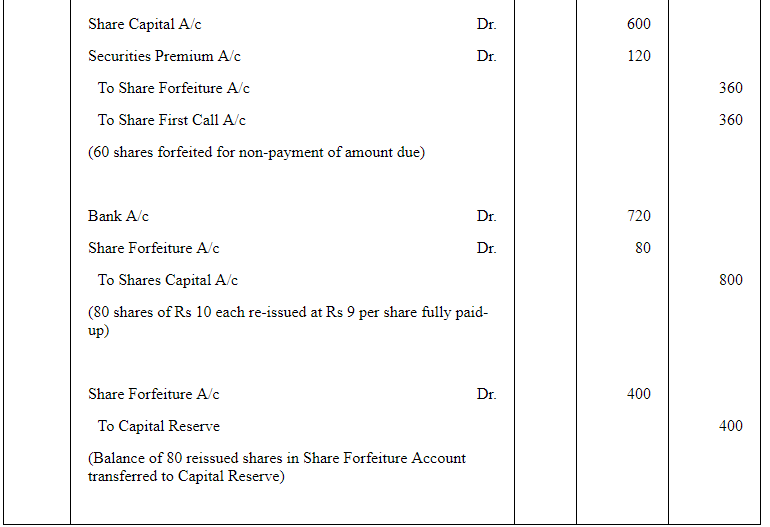

Rajesh, who applied for 72 shares failed to pay the two calls and on such failure, his shares were forfeited.

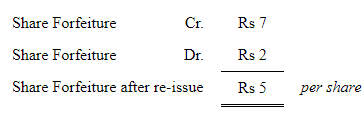

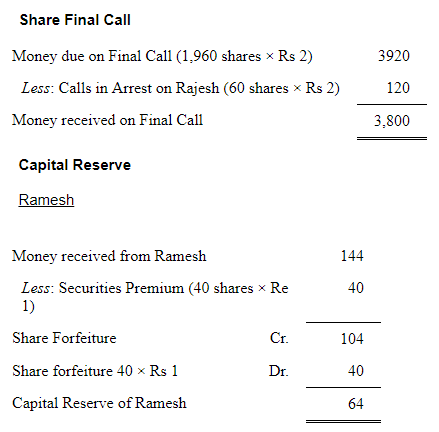

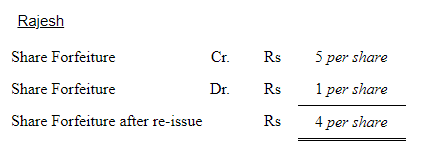

Of the shares forfeited, 80 shares were sold to Krishan credited as fully paid-up for ₹9 per share, the whole of Ramesh's shares being included.

Give journal entries to record the above transactions ( including cash transactions).

ANSWER:

Issued capital 2,000 shares of Rs 10 each at premium of Rs 2

Applied shares 3,000

Working Notes-

Ramesh's Shares

Number of shares applied

Capital Reserve on Rajesh's shares = Share Forfeiture after re-issue (per share) × No. of shares re-issued = Rs 4 × 40 = Rs 160

Total Capital Reserve = Capital Reserve of 40 shares of Ramesh + Capital Reserve of 40 shares of Rajesh = 64 + 160 = Rs 224

Question 91:

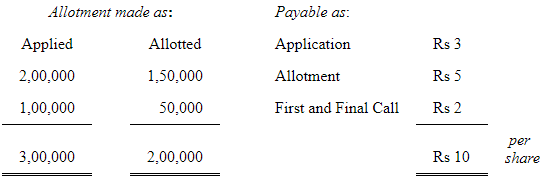

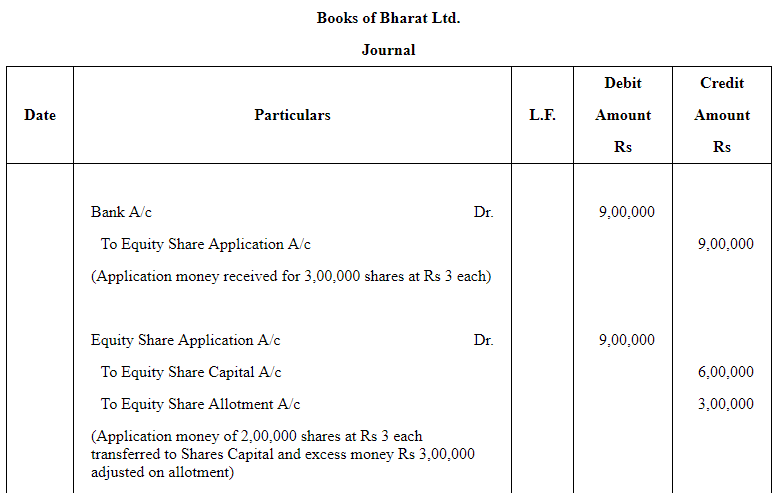

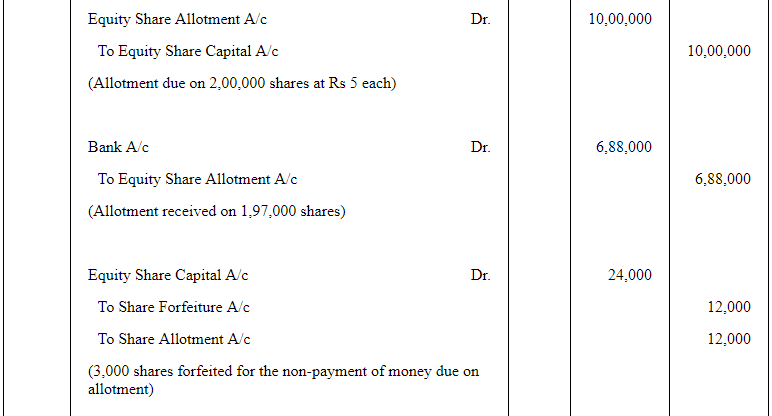

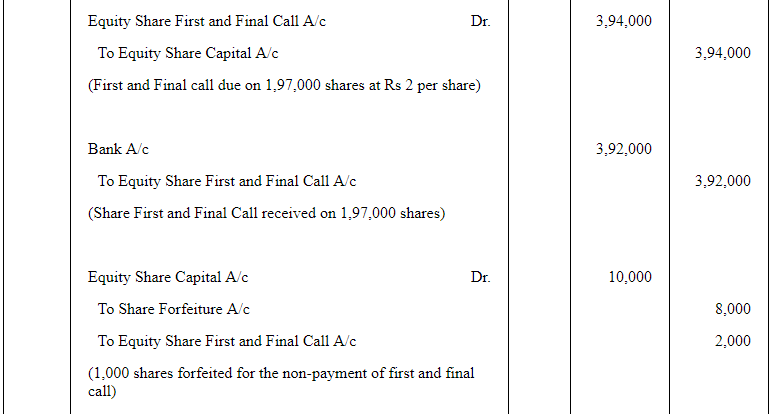

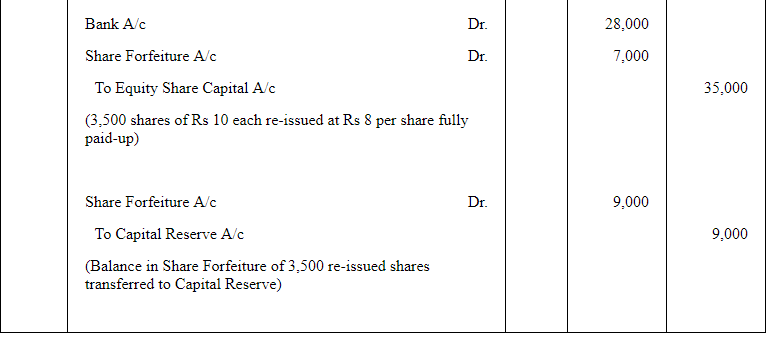

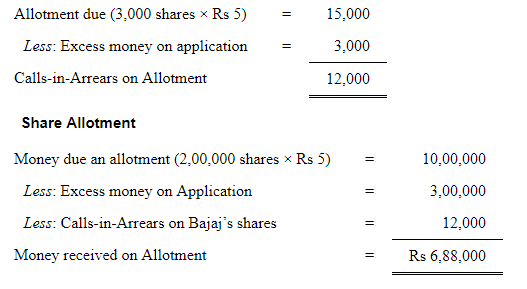

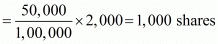

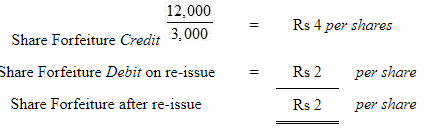

Bharat Ltd . invited applications for issuing 2,00,000 Equity Shares of ₹ 10 each. The amount was payable as:

On application ₹ 3 per share, on allotment ₹ 5 per share and on first and final call ₹2 per share. Applications for 3,00,000 shares were received and pro rata allotment was made to all the applicants on the following basis:

Applicants for 2,00,000 shares were allotted 1,50,000 shares on pro rata basis.

Applicants for 1,00,000 shares were allotted 50,000 shares on pro rata basis. Bajaj, who was allotted 3,000 shares out of group applying for 2,00,000 shares failed to pay the allotment money. His shares were forfeited immediately after allotment . Sharma, who had applied for 2,000 shares out of the group applying for 1,00,000 shares failed to pay the first and final call. His shares were also forfeited.

Out of the forfeited shares 3,500 shares were reissued as fully paid-up @ ₹8 per share . The reissued shares included all the forfeited shares of Bajaj.

Give necessary journal entries to record the above transactions.

ANSWER:

Issued capital 2,00,000 shares of Rs 10 each.

Applied shares 3,00,000

Working Note:

Bajaj's ShareNumber of shares applied

Sharma's shares

Number of shares allotted

Capital Reserve

Forfeiture of shares held by Bajaj

Capital Reserve on re-issue of Bajaj's shares = Rs 2 × 3,000 (no. of shares re-issued) = Rs 6,000

Capital Reserve on re-issue of 500 Shares of Sharma = Rs 6 × 500 (no. of shares re-issued) = Rs 3,000

Total Capital Reserve on 3,500 shares = 6,000 (re-issue of Bajaj's) + 3,000 (re-issue of Sharma's) = Rs 9,000

Page No 8.130:

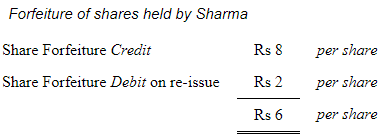

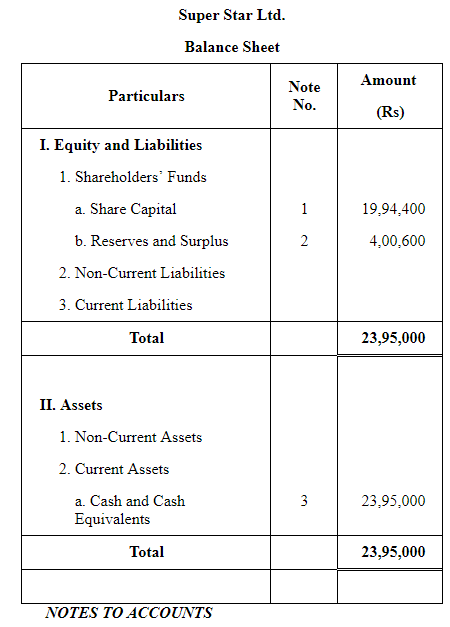

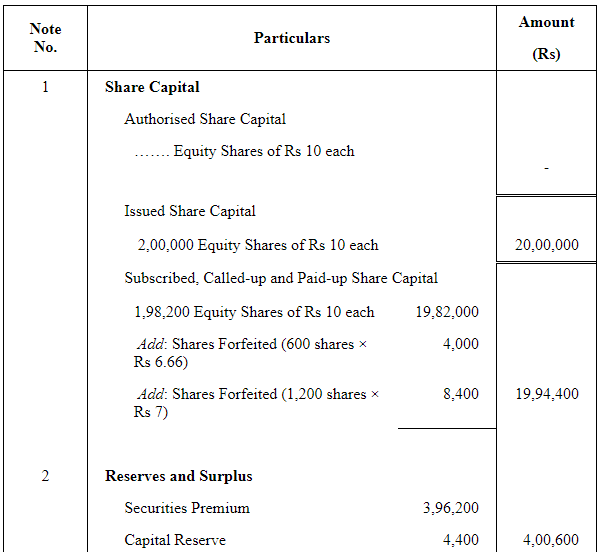

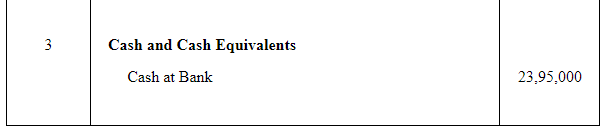

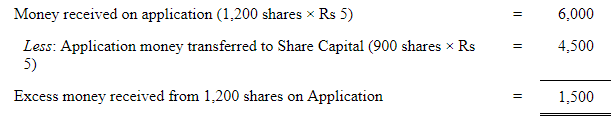

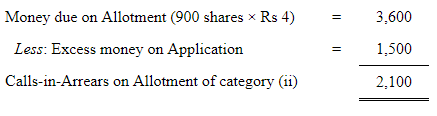

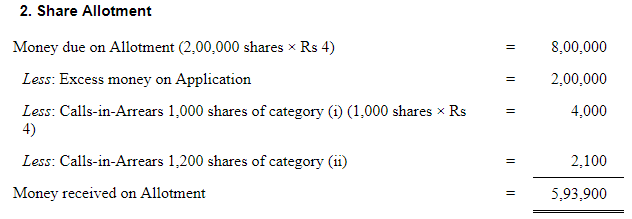

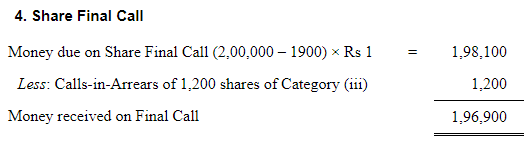

Question 92:

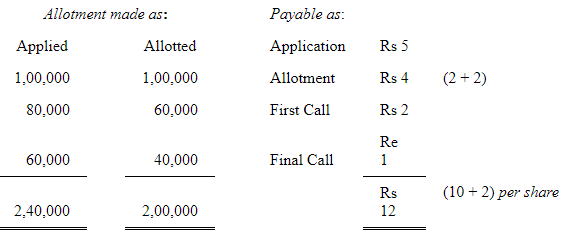

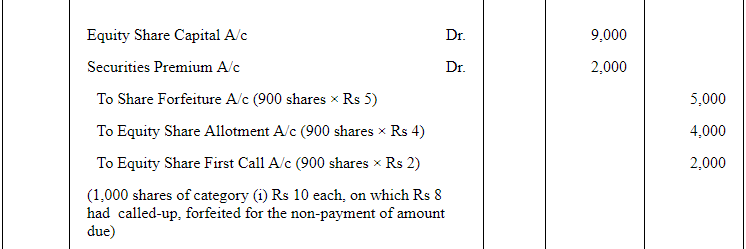

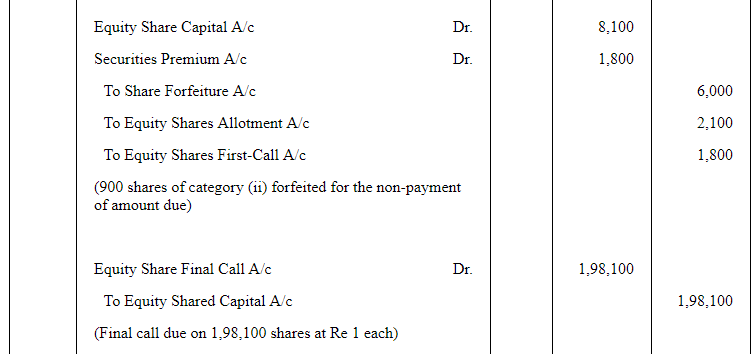

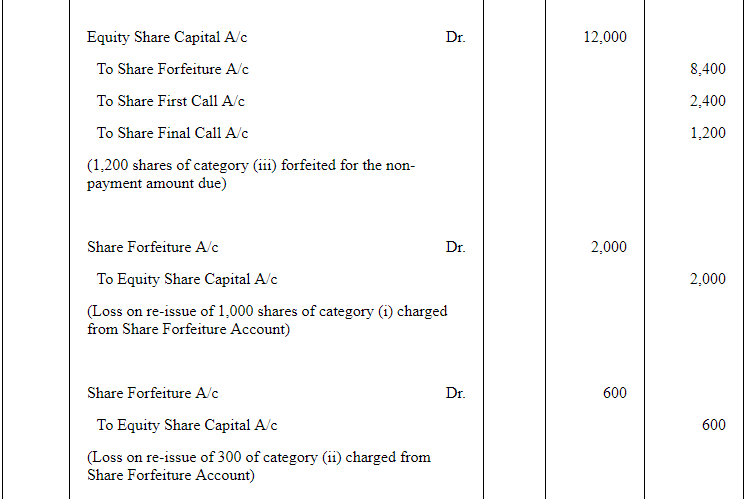

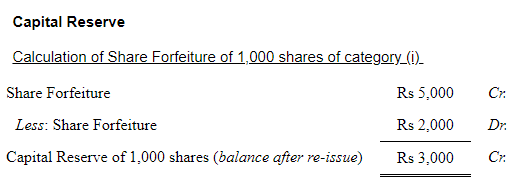

The Directors of Super Star Ltd. invited applications for 2,00,000 Equity Shares of ₹ 10 each to be issued at 20% premium. The money payable per shares was: on application ₹ 5, on allotment ₹ 4 (including premium of ₹ 2), first call ₹ 2 and final call ₹ 1.

Applications were received for 2,40,000 shares and allotment was made as:

(i) to applicants for 1,00,000 shares-- in full,

(ii) to applicants for 80,000 shares--60,000 shares,

(iii) to applicants for 60,000 shares--40,000 shares.

Applicants of 1,000 shares falling in Category

(i) and applicants of 1,200 shares falling in Category

(ii) failed to pay allotment money. These shares were forfeited on failure to pay first call. Holders of 1,200 shares falling in Category

(iii) failed to pay the first and final call and these shares were forfeited after final call.

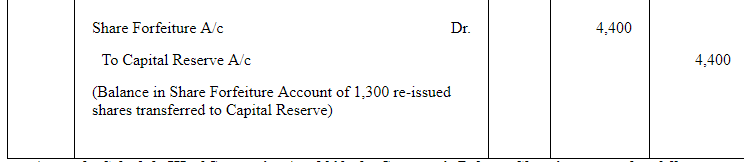

1,300 shares[1,000 of Category(i) and 300 of Category (ii)] were reissued at ₹8 per share as fully paid-up.

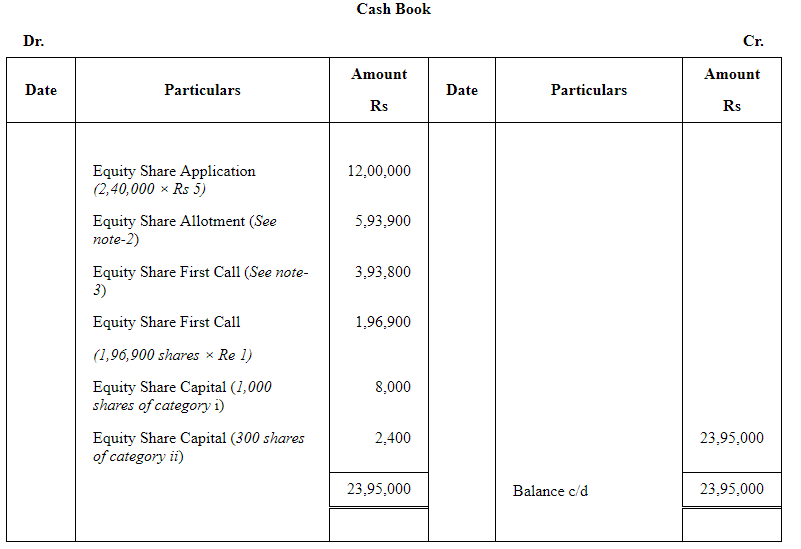

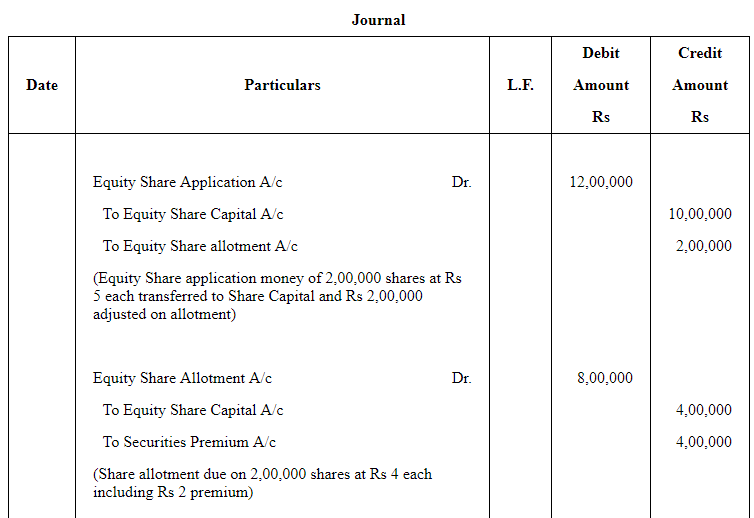

Journalise the above transactions. Prepare Cash book and Balance Sheet.

ANSWER:

Applied shares 2,40,000

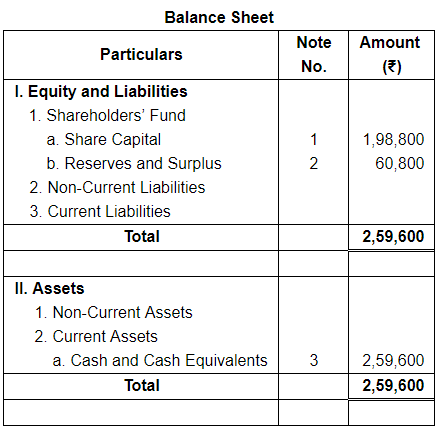

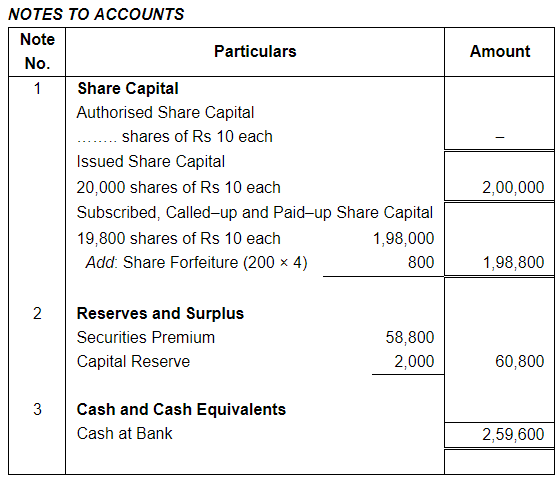

As per the Schedule III of Companies Act, 2013, the Company's Balance Sheet is presented as follows.

Working Notes:

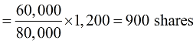

1. 1,200 shares of Category (ii)

Number of share allotted

3. Share First Call

First Call due on 2,00,000 shares × Rs 2 | = | 4,00,000 |

Less: Calls-in-Arrears on 3,100 shares × Rs 2 (1,000 + 900 + 1,200 shares of category (i), (ii) and (iii) respectively) | (6,200) | |

Money received on First Call | 3,93,800 |

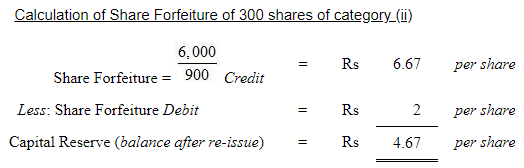

Capital Reserve of 300 shares = Capital Reserve (per share) × No. of shares re-issued = Rs 4.67 × 300 shares = Rs 1,400

Total Capital Reserve of 1,300 shares = Capital Reserve of 1,000 shares of category (i) + Capital Reserve of 300 shares of category (ii) = 3,000 + 1,400 = Rs 4,400

Page No 8.130:

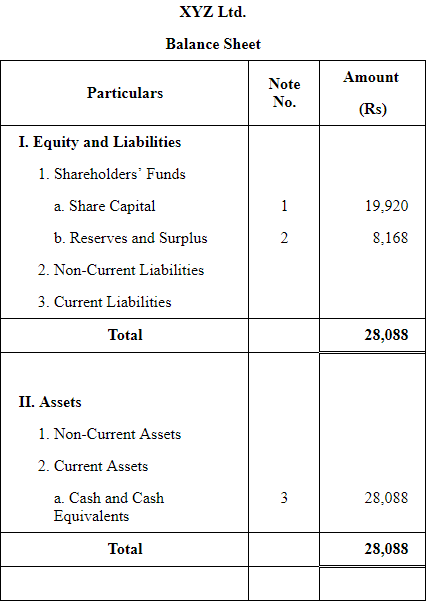

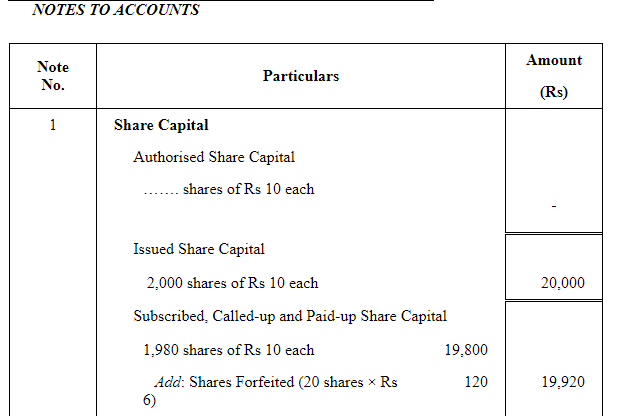

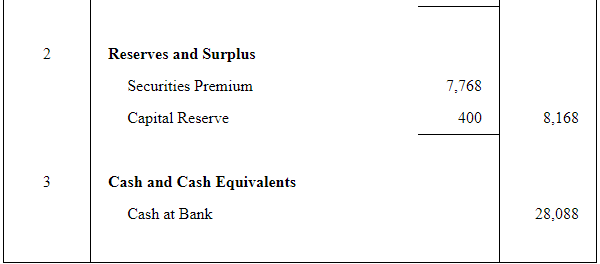

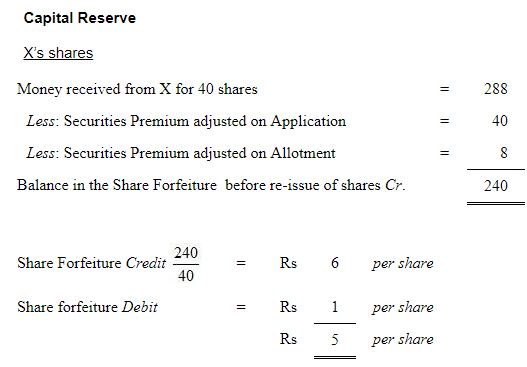

Question 93:

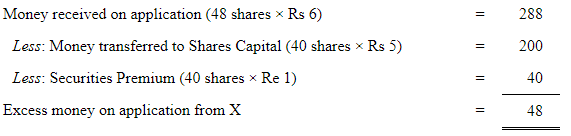

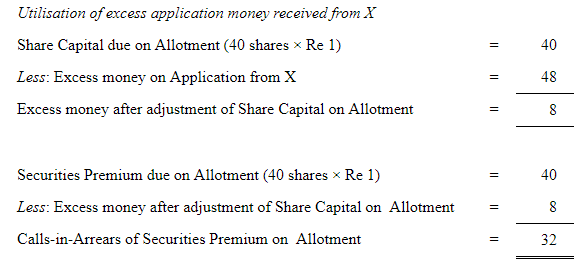

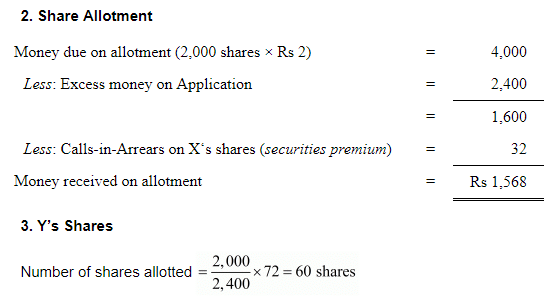

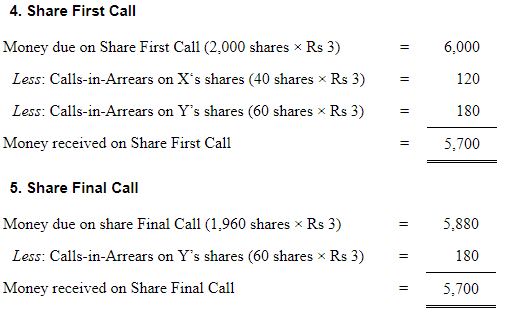

XYZ Ltd . issued a prospectus inviting applications for 2,000 shares of ₹10 each at a premium of ₹4 per share , payable as:

On application -- ₹6 (including ₹1 premium)

On allotment - ₹2 (including ₹1 premium)

On first call -- ₹3 (including ₹1 premium)

On second and final call -- ₹3 (including ₹1 premium)

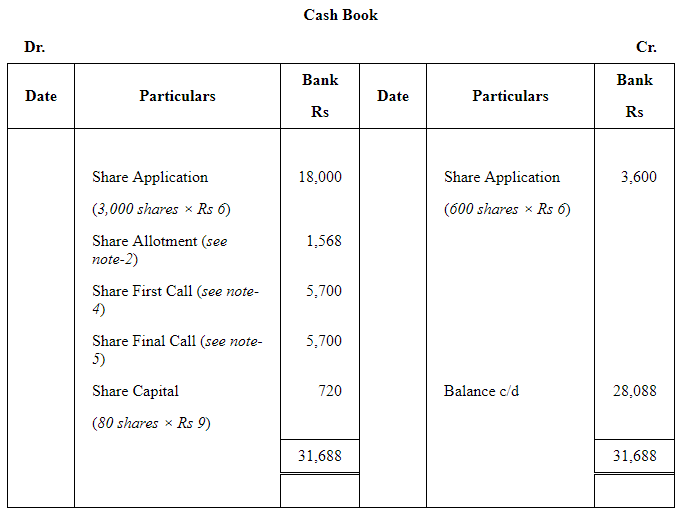

Applications were received for 3,000 shares and pro rata allotment was made on the applications for 2,400 shares. It was decided to utilise excess application money towards the amount due on allotment.

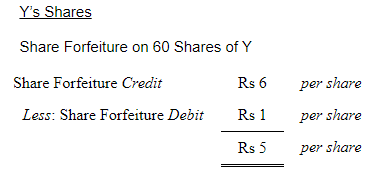

X, to whom 40 shares were allotted, failed to pay the allotment money and on his subsequent failure to pay the first call , his shares were forfeited.

Y, who applied for 72 shares failed to pay the two calls and on his such failure , his shares were forfeited.

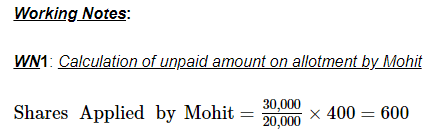

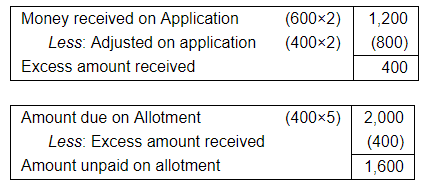

Of the shares forfeited , 80 shares were sold to Z credited as fully paid-up for ₹9 per share , the whole of Y's shares being included . Prepare Journal , Cash Book and the Balance Sheet .

ANSWER:

As per the Schedule III of Companies Act, 2013, the Company's Balance Sheet is presented as follows.

Working Notes:

1. X's Shares

Number of share applied by X

Capital Reserve on re-issue of 20 shares = Rs 5 × 20 shares = Rs 100

Capital Reserve on re-issue of 60 shares of Y = Rs 5 × 60 shares = Rs 300

Total Capital Reserve on 80 shares = Capital Reserve on re-issue of 20 shares of X + Capital Reserve on re-issue of 60 shares of Y = 100 + 300 = Rs 400

FAQs on Accounting for Share Capital (Part - 5)

| 1. What is share capital in accounting? |  |

| 2. What is the difference between equity shares and preference shares? | |

| 3. How is share capital recorded in accounting? | |

| 4. Can a company increase its share capital after the initial issuance of shares? | |

| 5. What are the accounting implications of share capital reduction? | |