Tools of Financial Analysis - 1 | Commerce & Accountancy Optional Notes for UPSC PDF Download

| Table of contents |

|

| Introduction |

|

| Techniques of Financial Analysis |

|

| Common Size Statements |

|

| Comparative Statements |

|

| Trend Analysis |

|

| Ratio Analysis |

|

Introduction

- The Balance Sheet provides a snapshot of the entity's wealth at a specific moment, while the Profit and Loss Account delineates the income earned and expenses incurred over a financial period. The Cash Flow Statement delineates the cash inflows and outflows associated with the aforementioned activities.

- Many small investors, like yourself, often invest in shares of various companies with limited knowledge about the companies themselves. In such cases, small investors who lack understanding of financial reports often seek assistance from mutual funds. You will delve deeper into mutual funds in another course, but to introduce the concept, mutual funds are trusts or entities managed by investment trusts and registered under the Trust Act. They pool funds from small investors and invest in shares, debentures, or bonds on their behalf. Frequently, mutual funds yield superior returns for individual and small investors compared to what they could achieve on their own. This is attributed to the expertise and experience of mutual fund managers, who specialize in investing and possess greater insight compared to novice investors. Novice investors often lack the time and expertise to analyze and evaluate a company's financial standing, necessitating a basic understanding of the company's financial statements for any dealings or investment decisions.

- Consequently, individuals intending to invest in companies or engage in transactions with them must conduct an analysis of the financial statements. This applies to all stakeholders of the company, including employees, shareholders, suppliers, government entities, tax authorities, bankers, and lenders. Lending institutions, for instance, scrutinize financial statements to assess a company's ability to repay loans, while shareholders seek insights into the company's prospects and potential returns on investment. Similarly, the government may analyze financial statements to gauge a company's performance relative to others in the same industry or to ascertain if it's operating as a viable entity or as a struggling entity. Thus, the focus and interpretation of financial statement analysis vary depending on the objectives of the analyst. With an understanding of the diverse objectives of financial statement analysis, let's delve into how exactly it is conducted.

Techniques of Financial Analysis

- Investors often base their share purchases on various company-related information. For instance, a company may have developed a groundbreaking new drug, become a takeover target, entered into exports to a thriving region, or discovered new gold deposits. Any of these factors could lead to a significant short-term boost in share prices.

- However, it's crucial to recognize that profits are fundamental to a company's long-term performance. Profits enable companies to invest in growth, repay loans, and distribute dividends. Without profits, a company's viability may be called into question. Therefore, much of the analysis focuses on understanding the company's profitability.

- Financial analysis aims to forecast a company's future performance, although it's inherently limited by the fact that it relies on historical data to predict future outcomes. While some experts use technical analysis to predict stock prices using historical data, it's important to note that such predictions may not always align with reality. Furthermore, even top economists have struggled to predict significant economic events, such as the recent Asian economic downturn. Hence, there are significant limitations to what can be expected from financial analysis.

- Efficiency in operations is another crucial aspect to consider. It's not sufficient for a company to merely invest in growth; it must also operate efficiently relative to its competitors. Additionally, analyzing debt levels and their potential impact on a company's performance is essential. While low-interest rates may justify heavy borrowing for growth investments, rising interest rates could threaten profitability and the ability to repay loans.

Financial analysis primarily focuses on three major areas: Profitability, Productivity, and Risk (evaluated through leverage or debt-equity mix). To conduct this analysis, comparisons are necessary. These comparisons typically involve:

- Comparing the performance of the target company with its competitors,

- Benchmarking against competitors or other benchmark companies,

- Comparing against industry averages, and

- Analyzing the company's performance over time (time-series analysis).

These comparisons are known as cross-sectional analysis (for the second and third types) and time-series analysis (for the fourth type). To perform such analyses, organized techniques are required, including:

- Common size statement analysis,

- Ratio analysis,

- Comparative Statement Analysis (cross-sectional analysis),

- Trend Analysis (time-series analysis), and

- Du Pont Analysis (structured ratio analysis).

These techniques are widely utilized by experts globally and will be covered in detail in subsequent sections.

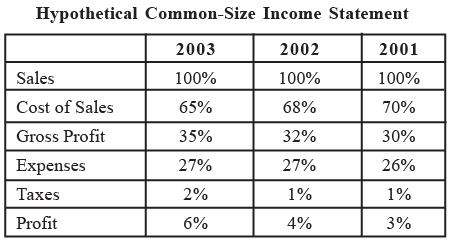

Common Size Statements

- When comparing your company to industry standards, it's crucial to ensure that financial data for each company reflects comparable price levels and is developed using similar accounting methods, classification procedures, and valuation bases. These comparisons should be limited to companies engaged in similar business activities. Any differences in financial policies between two companies should be acknowledged when evaluating comparative reports. For instance, if one company leases properties while another purchases them, or if one relies heavily on long-term borrowing while the other primarily uses shareholder funds and retained earnings, the financial statements of these companies are not entirely comparable.

- To address this challenge, common size statements are utilized. A Common Size Statement presents financial data where all items are expressed as a percentage of a common base figure. This statement is valuable for identifying changes in the relative size of various elements. Essentially, it represents a statement in which all items are depicted as a percentage of a base figure, facilitating the analysis of trends and changing relationships among financial statement items. For example, all items in an income statement for each year could be presented as a percentage of net sales. This technique is particularly useful when comparing businesses to each other or to industry averages, as differences in size are normalized by converting all figures to common-size ratios. Industry statistics are often published in common-size format.

- When conducting ratio analysis (which will be covered in detail in the next section) of financial statements, it's beneficial to adjust the figures to common-size numbers. This involves converting each line item on a statement to a percentage of the total. For instance, on a balance sheet, each figure is represented as a percentage of total assets, while on an income statement, each item is expressed as a percentage of sales.

Vertical and Horizontal Analysis

Vertical analysis involves calculating percentages, ratios, turnovers, and other financial position and operating result measures for a single fiscal period. When these figures are compared with those from different periods, it transitions into horizontal analysis. For example, if you were to convert the figures into percentages for ABC Industries for only the year 2003, it would constitute vertical analysis. However, what has been provided to you is the horizontal analysis of the common size financial statements.

Comparative Statements

- Initially, when examining a company's current financial data, it can seem daunting and often confusing. However, comparing this data to the business's historical performance renders it considerably more meaningful. Therefore, it is more practical to juxtapose the company's current financial figures with monthly, quarterly, or annual data from previous fiscal years. Through this process, you should observe discernible trends that will aid in forecasting the future trajectory of your business.

- This procedure resembles the common size financial statement but is approached slightly differently. To illustrate its significance, consider a hypothetical example involving the comparative financial statements of XYZ Company. Despite calculating percentages for each year, which constitutes vertical analysis, horizontal analysis has also been conducted by comparing data across multiple years. This enables not only a comparison of performance over the years but also a comparison with industry averages.

Trend Analysis

- Why is trend analysis useful? It's highly beneficial because it allows us to not only assess past performance but also to gauge whether the company will continue performing similarly or improve in the coming years. Similar analyses are conducted in stock investment, where technical analysts analyze trends in stock price movements to predict future stock prices. Similar analyses are applied in financial statement analysis as well.

- But how and where can we apply trend analysis of financial statements?

- Trend analysis is crucial for identifying potential issues with a borrower. This is essential during the initial review of a loan application, as well as during ongoing monitoring of disbursed loans. Both sound and weak companies may exhibit some similar trends, but it's a pattern of numerous negative trends that indicates a potential problem requiring further evaluation.

- Trend analysis entails spreading financial statements and comparing similar operating periods (e.g., year to year). This comparative analysis enables reviewers to identify both positive and negative trends. Once a pattern of negative trends is identified, further action is warranted. For potential loans, additional information or detailed explanations should be sought. The trends should be carefully considered when making decisions about loan approval or rejection. For existing loans, a pattern of negative trends necessitates swift action. Current financial information may indicate a problem, allowing reviewers time to respond accordingly.

Below is a general discussion of trends to look for when reviewing financial statements:

- Decreasing cash position: This may manifest as lower cash levels or cash as a percentage of total assets. Changes in deposit activity, draws on uncollected funds, or declining average monthly balances should be noted.

- Slowdown in receivables collection: This could indicate business distractions, neglect, changes in collection policies, etc.

- Significant increases in accounts receivable: This could be in terms of the dollar amount, percentage of assets, or accounts receivable to a single customer.

- Rising inventories: This could indicate a need to liquidate excessive or obsolete inventory, lack of attention to purchasing, or slowing sales.

- Slowdown in inventory turnover: This may indicate sales slowdown, overbuying, production problems, or issues with purchasing policies.

- Changes in sales terms/policies: Changes from cash sales to installment sales, leasing instead of selling, etc., should be noted.

- Decline in liquid assets: This could be a dollar decline or a decline in current assets to total assets, potentially affecting the ability to meet current liabilities.

- Changes in fixed asset concentration: Both declining and rising concentrations should be reviewed, considering whether funds are being used appropriately for replacements, renovations, or other operational needs.

- Revaluation of assets: Revaluation should be justified; otherwise, it impacts the company's financial picture.

- Changes in asset liens: New subordinated debt may indicate a deteriorating financial situation.

- High or increasing concentration of assets in intangibles: Intangible assets' value is challenging to establish and is typically eliminated from financial reviews.

- Increases in current debt: A rise, particularly tied to trade debt, or without a corresponding increase in assets, should raise concerns.

- Increases in long-term debt: Increases must be reviewed carefully, especially if repayment relies on higher-than-historical or projected sales.

- Increase or significant gap between gross and net sales: This may indicate lower quality, production problems, outdated product lines, or other related production and market factors.

- A rise in debt-to-capital ratio: This becomes worrisome, especially when the current ratio is low. Undercapitalized firms often face poor working capital conditions.

- Increase in cost of goods sold: A rise may suggest operational issues or increased expenses elsewhere.

- Decrease in profits relative to sales: This decline could stem from inadequate cost controls, management challenges, or failure to pass on cost increases.

- Growth in bad debt: An uptick as a percentage of sales typically signals deficient collection procedures, management issues, or declining customer quality.

- Assets growing faster than sales: This implies that increased assets are not translating into sales growth.

- Assets growing faster than profits: Assets are investments intended to generate profits. Concerns arise when increased assets fail to yield higher profits.

- Significant fluctuations in other areas of financial statements: Notable changes warrant thorough examination.

- An increase or significant gap between gross and net sales: This could result from lower quality, production issues, outdated product lines, or other market factors.

- A surge in debt-to-capital ratio: This is particularly concerning when the current ratio is low, indicating potential poor working capital conditions for undercapitalized firms.

- Rise in cost of goods sold: This uptick may indicate operational or expense-related challenges.

- Decline in profits compared to sales: This decrease might be due to deficient cost controls, management issues, or failure to manage cost increases.

- Increase in bad debt: A rise as a percentage of sales typically signals inadequate collection procedures, management challenges, or deteriorating customer quality.

- Assets growing faster than sales: This suggests that increased assets are not driving sales growth.

- Assets growing faster than profits: Assets are meant to generate profits; hence, concerns arise when increased assets do not lead to higher profits.

- Significant deviations in other areas of financial statements: Noticeable changes require thorough investigation.

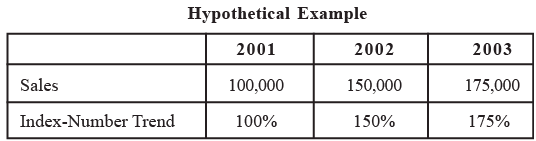

Apart from the aforementioned analysis, a simpler form of trend analysis can be adopted, known as Index Number Trend analysis.

Index-Number Trend Series

- Index-Number Trend Series offers a practical solution when analyzing financial data over an extended period becomes overwhelming. Rather than manually comparing financial statements, this method streamlines the process. Start by selecting a base year against which all other financial data will be compared.

- Typically, the base year is the earliest year in the dataset, although you may choose another year deemed suitable. Transform all amounts from the base year to 100 percent. Then express figures from subsequent years as a percentage of the base year amounts. It's important to note that index-numbers can only be computed for positive amounts.

- The index-number trend series method, a form of horizontal analysis, offers a comprehensive perspective on your company's financial status, earnings, and cash flow over an extended period. However, it's crucial to acknowledge that long-range trend series are highly sensitive to fluctuations in price levels. For example, there may be significant increases in price levels during certain years. Ignoring such changes in a horizontal analysis could erroneously indicate substantial growth in sales or net income when, in reality, there was little or no actual growth.

- Data presented relative to a base year can be immensely valuable when comparing your company's performance to that of government agencies and industry sources, as they often utilize index-number trend series. When conducting comparisons, ensure that the datasets share the same base period. If not, simply adjust one of the datasets to align with the other.

Ratio Analysis

- While many of us focus primarily on a company's bottom line, namely its profitability, solely examining the profit figure doesn't provide a comprehensive view of its performance. Relying solely on bottom-line figures can lead to misleading conclusions. For instance, consider two companies, A and B, in the same industry. Company A earned a profit of Rs. 100 Crs., while Company B earned Rs. 1000 Crs. for the financial year 2003. At first glance, it may seem that Company B is superior to Company A. However, a wise approach would involve comparing the profit earned with the level of investment made to earn that profit. For example, Company A spent about Rs. 500 Crs. to earn Rs. 100 Crs. profit, while Company B spent about Rs. 1000 Crs. to earn Rs. 1000 Crs. profit. Consequently, the profitability of Company A is higher than that of Company B, as evidenced by the higher profit-to-investment ratio for Company A (20%) compared to Company B (10%). Therefore, it's crucial to analyze profitability, not just profit figures. The key takeaway is that appropriate ratios, not just absolute figures, should be considered for comparison, making ratio analysis essential for a better understanding of financial results.

- Ratio analysis typically involves calculating a range of ratios, condensing complex information into standardized and easily understandable forms. These ratios allow for comparisons between different years within a single company, across companies of varying sizes, or across different industries. However, it's important to note that ratios serve as signals or clues rather than definitive answers to complex questions about a company. While some ratios may point to specific problems within the company, others may indicate the need for further investigation.

Ratios can be expressed in various forms, including percentages, fractions, "times" figures, number of days, rates, or simple numbers.

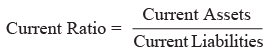

Liquidity Analysis Ratios

These ratios assess a firm's ability to convert its assets into cash to meet its day-to-day payments. Low liquidity ratios indicate that a company's funds are tied up in stocks and debtors, potentially causing cash flow problems. A value less than 1.5 is often seen as a warning sign that the company may run out of money due to its cash being tied up in unproductive assets. Liquidity ratios help evaluate a firm's ability to meet its current obligations. Key ratios in this category include the current ratio, quick ratio, and net working capital ratio.

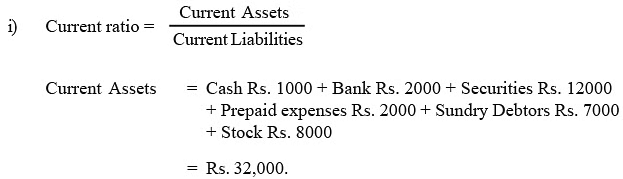

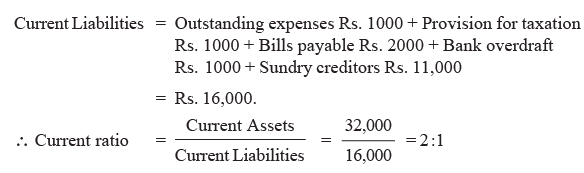

- Current Ratio: This ratio measures the relationship between current assets and current liabilities, indicating the firm's ability to meet short-term obligations. Current assets include cash, cash equivalents, accounts receivable, and inventory, while current liabilities encompass short-term debts and payables. The formula for computing the current ratio is:

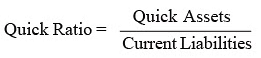

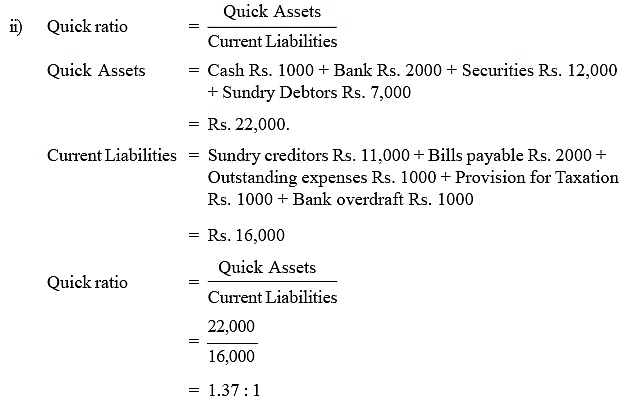

- Quick Ratio: The acid test ratio, akin to the current ratio, assesses the liquidity of the company. A ratio of 1:1 (or approximately 1) is considered acceptable. However, if the value is significantly below 1, it suggests that the company has a substantial portion of its cash tied up in unproductive assets, potentially hindering its ability to raise funds in the short term.

Quick Assets = Current Assets---Inventories

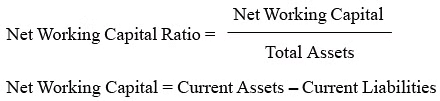

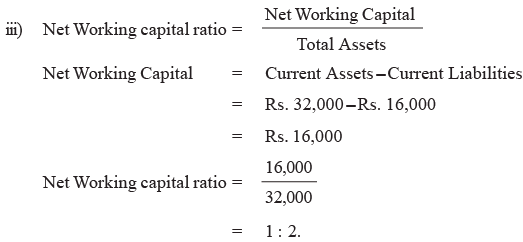

Quick Assets = Current Assets---Inventories - Net Working Capital Ratio: The working capital ratio can give an indication of the ability of your business to pay its bills.

Generally, a working capital ratio of 2:1 is regarded as desirable. However, the circumstances of every business vary and you should consider how your business operates and set an appropriate benchmark ratio. A stronger ratio indicates a better ability to meet ongoing and unexpected bills therefore taking the pressure off your cash flow. Being in a liquid position can also have advantages such as being able to negotiate cash discounts with your suppliers. A weaker ratio may indicate that your business is having greater difficulties meeting its short-term commitments and that additional working capital support is required. Having to pay bills before payments are received may be the issue in which case an overdraft could assist. Alternatively building up a reserve of cash investments may create a sound working capital buffer. Ratios should be considered over a period of time (say three years), in order to identify trends in the performance of the business.

The calculation used to obtain the ratio is:

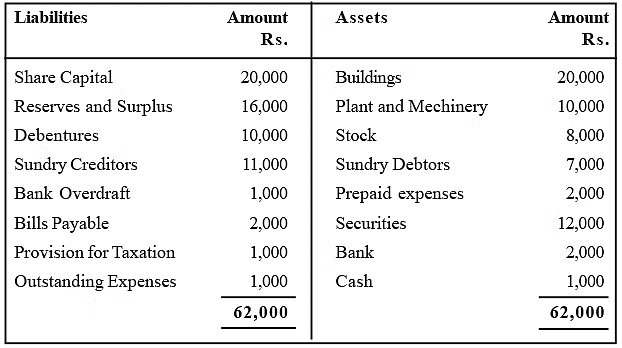

Illustration: The Balance Sheet of X Company Ltd. as on March 31, 2005 is given below. You are required to calculate the following ratios:

(i) Current ratio,

(ii) Quick ratio,

(iii) Net Working capital ratio.

Balance Sheet of X Company Ltd., as on 31.3.2005

Solution:

Profitability Analysis Ratios

Profitability ratios are the most significant - and telling - of financial ratios. Similar to income ratios, profitability ratios provide a definitive evaluation of the overall effectiveness of management based on the returns generated on sales and investment.

Profitability in relation to Sales

Profits earned in relation to sales give the indication that the firm is able to meet all operating expenses and also produce a surplus. In order to judge the efficiency of management with respect to production and sales, profitability ratios are calculated in relation to sales.

There are:

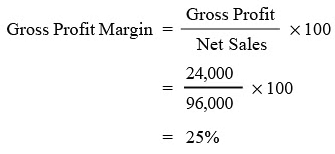

(i) Gross Profit Margin

- This is also known as gross profit ratio or gross profit to sales ratio. This ratio may indicate to what extent the selling prices of goods per unit may be reduced without incurring losses on operations. This ratio is useful particularly in the case of wholesale and ratail trading firms. It establishes the relationship between gross profit and net sales. Its purpose is to show the amount of gross profit generated for each rupees of sales. Gross profit margin is computed as follows:

- The amount of gross profit is the difference between net sales income and the cost of goods sold which includes direct expenses. A high margin enables all operating expenses to be covered and provides a reasonable return to the shareholders. If gross profit rate is continuously lower than the average margin, something is wrong.

- To keep the ratio high, management has to minimise cost of goods sold and improve sales performance. Higher the ratio, the greater would be the margin to cover operating expenses and vice versa.

Note: This percentage rate can --- and will --- vary greatly from business to business, even those within the same industry. Sales location, size of operations and intensity of competition etc., are the factors that can affect the gross profit rate.

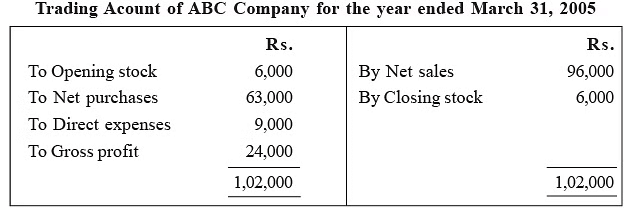

Illustration: From the following particulars, calculate gross profit margin.

Solution:

(ii) Net Profit Margin

This ratio is called net profit to sales ratio and explains the relationship between net profit after taxes and net sales. The purpose of this ratio is to reveal the amount of sales income left for shareholders after meeting all costs and expenses of the business. It measures the overall profitability of the firm. The higher the ratio, the greater would be the return to the shareholders and vice versa. A net profit margin of 10% is considered normal. This ratio is very useful to control costs and to increase the sales. It is calculated as follows:

(iii) Operating Profit Margin

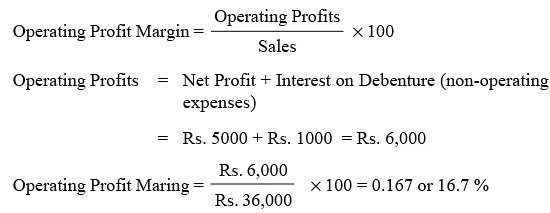

This ratio is a modified version of Net Profit Margin. It studies the relationship between operating profit (also known as PBIT — Before Interest and Taxes) and sales. The purpose of computing this ratio is to find out the amount of operating profit for each rupee of sale. While calculating operating profit, nonoperating expenses such as interest, (loss on sale of assets etc.) and non-operating income (such as profit on sale of assets, income on investment etc.) have to be ignored. The formula for this ratio is as follows:

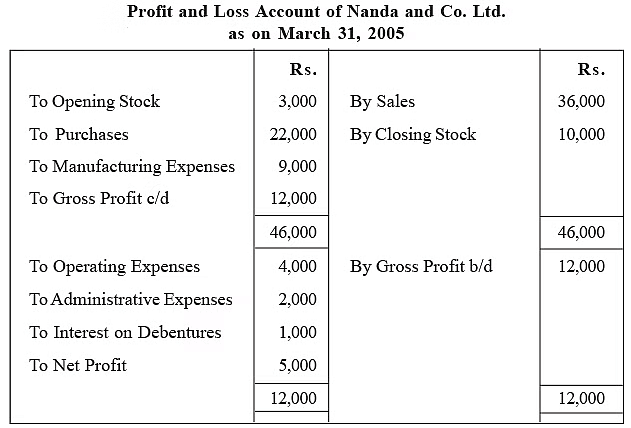

Illustration: From the following particulars of Nanda and Co., calculate Operating Profit Margin.

Solution:

A high ratio is an indicator of the operational efficiency and a low ratio stands for operational inefficiency of the firm.

(iv) Operating Ratio

This ratio established the relationship between total costs incurred and sales. It may be calculated as follows:

The operating ratio shows the overall operating efficiency of the business. In order to know how individual items of operating expenses are related to sales, individual expenses ratios can also be calculated. These are calculated by taking operational expenses like cost of goods sold, administrative expenses, selling and distribution, individually in relation to sales (net).

|

196 videos|219 docs

|

FAQs on Tools of Financial Analysis - 1 - Commerce & Accountancy Optional Notes for UPSC

| 1. What are the common techniques of financial analysis? |  |

| 2. What is the purpose of using common size statements in financial analysis? | |

| 3. How does trend analysis help in financial analysis? | |

| 4. What is the significance of ratio analysis in financial analysis? | |

| 5. How do financial analysts use comparative statements in their analysis? | |

ppt

,Exam

,shortcuts and tricks

,Viva Questions

,Sample Paper

,video lectures

,MCQs

,Tools of Financial Analysis - 1 | Commerce & Accountancy Optional Notes for UPSC

,Important questions

,past year papers

,Tools of Financial Analysis - 1 | Commerce & Accountancy Optional Notes for UPSC

,practice quizzes

,Extra Questions

,Previous Year Questions with Solutions

,Summary

,Semester Notes

,Tools of Financial Analysis - 1 | Commerce & Accountancy Optional Notes for UPSC

,Objective type Questions

,study material

,mock tests for examination

,Free

;

Tools of Financial Analysis - 1 Free PDF Download

Importance of Tools of Financial Analysis - 1

Tools of Financial Analysis - 1 Notes

Tools of Financial Analysis - 1 UPSC Questions

Study Tools of Financial Analysis - 1 on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!